Older Americans Are Returning to the Workforce in Record Numbers

The new year always fills people with hope and optimism. It’s why we make resolutions. But the reason those typically fail is because they’re designed to.

Eating healthier? Admirable. But after three weeks of dieting, visions of dancing pizza and never-ending pasta bowls will haunt your dreams as the salad in your refrigerator wilts.

Exercising daily is another popular choice. Promotional memberships offered by fitness centers surge in January. By Groundhog Day, only the gym rats remain.

Financial resolutions are more realistic and can be achieved with far less effort than is required by strict workout regimens or fashionable diets … and for comparable amounts of money.

So this week, we’re revisiting retirement and recommending you focus on it as your new year’s resolution. Because nobody should have to work forever. But as 2023’s data shows, it’s increasingly likely that Americans will remain in (or return to) the workforce after hitting retirement age.

The Un-Retirement Trend

According to Yahoo! Finance, last year, the average American retiree had $170,726 in retirement savings, a 10% decrease from 2022’s $191,659 and woefully short of the recommended $555,000 that only 12% of retirees achieve or surpass.

What’s worse, 37% of retirees have no retirement savings.

These are crisis-level figures, especially considering how (1) retirement is heavily dependent on fixed income and (2) the costs of certain consumer staples hardly ever subside.

For example, the cost of food at home. Going back to 1968, the price of groceries has only fallen 10 out of 660 months. That’s just 1.5% of all months dating back to President Lydon Baines Johnson, meaning food prices are an exception to the old adage, “what goes up must come down.”

The results of these failures in retirement savings coupled with runaway prices are horrifying:

- 45% of American retirees report a decline in living standards.

- Americans aged 75 and older represent the fastest-growing age group in the workforce.

- And the 11 million older Americans working today are quadruple the number that worked in the mid-1980s.

We’ve previously discussed how, in the early ‘80s, companies began moving away from pension plans in favor of bottom-line beneficial defined contribution plans like the 401(k). That’s a major factor in all of this, but what’s done is done.

Now we need to be accountable for our own retirement plans. Because the average age of an American grandparent is 67, while the average life expectancy of an American is 76. And instead of bagging groceries or stocking shelves in our later years, retirees should be clogging the left lane during rush hour en route to pickleball tournaments and early bird dinners.

They’ve earned that right.

Tip #1: Max Out Your Retirement Accounts

Doing so for a 401(k) might be more challenging than for an IRA, but if you can, you should.

The IRS increased contribution limits for both types of accounts for 2024. Annual limits for IRAs rose from $6,500 to $7,000, and from $22,500 to $23,000 for a 401(k).

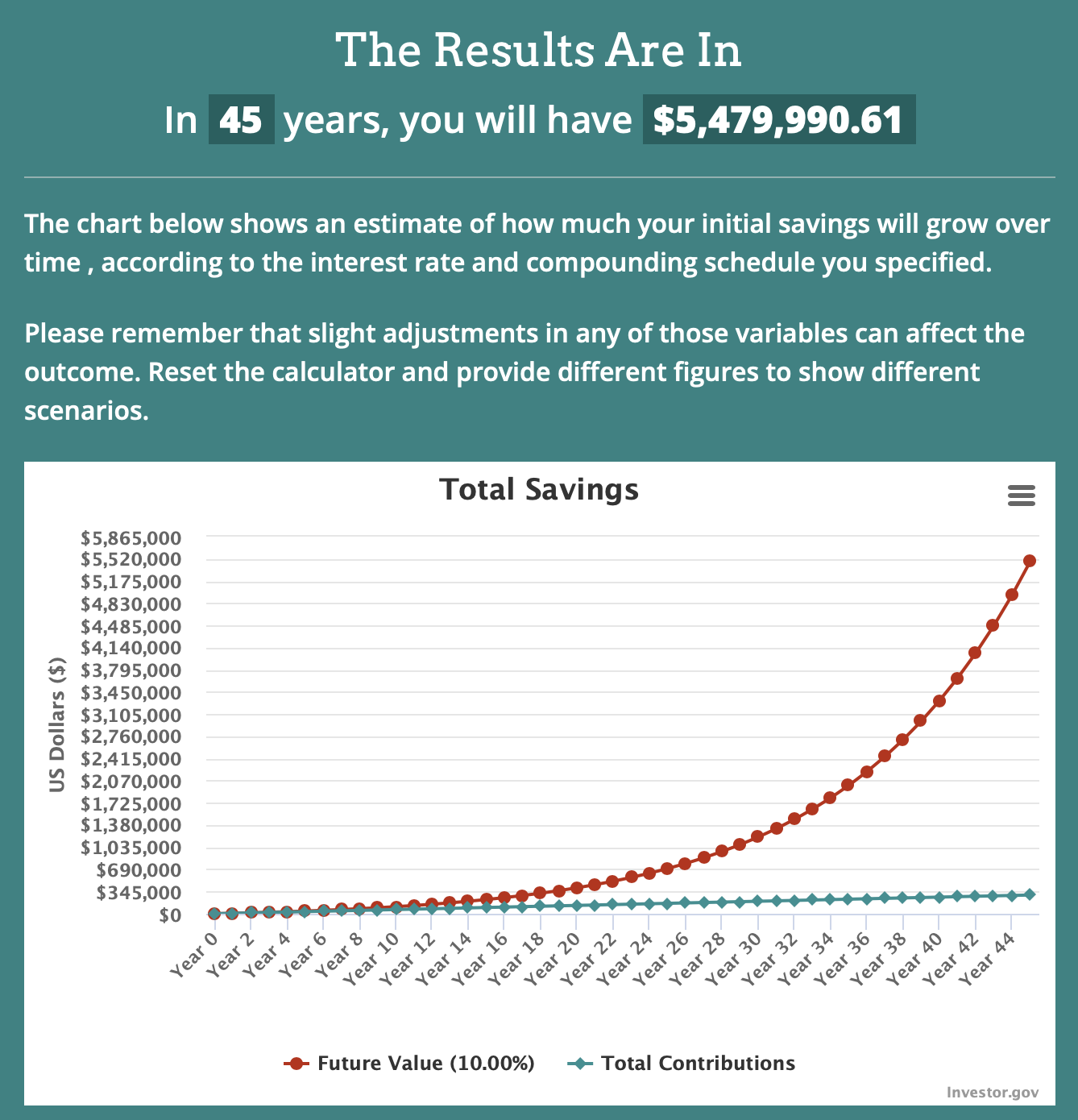

That means, if possible, you need to commit a line in your household budget that ensures you maximize your retirement savings. For IRAs, that $7,000 breaks down to $134.61/week.

The average hourly wage for an American is $28.16, meaning you can earmark less than $135/week in fewer than 4.7 hours of work. That leaves 35.3 hours (for full-time workers and those who don’t require a second job) dedicated to your other fixed expenses.

But in order to avoid becoming part of the aforementioned un-retirement statistics, it’s critical to begin treating retirement savings as mandatory.

If you begin investing that amount at age 25 in a passively managed S&P 500 index fund with a historical average annual return of 10%, that $134.61/week will be $5.479 million at retirement. And that’s just a baseline assuming the IRS doesn’t increase contribution limits between now and 2069, which is highly unlikely.

Some of you might be lamenting the $538.44/month this requires, which brings us to our next tip.

Tip #2: Follow Buffett’s Advice

Warren Buffett once remarked, “Do not save what is left after spending, but spend what is left after saving.”

That budget line for retirement savings should be treated no differently than the ones for housing, utilities and food. It’s essential.

It doesn’t have to be $538.44/month if you can’t manage it. View retirement savings as a blended income strategy. If you’re behind in your plan, remember that you can generate blended retirement income from a combination of your 401(k), IRA(s), annuities, dividend portfolio and Social Security.

This strategy is particularly important because you may not be able to rely on one of those components — Social Security — if a certain political party succeeds in gutting and/or destroying it.

As the Center for Retirement Research at Boston College points out, members of that party are already making concerted efforts to:

- Increase the full retirement age from 67 to 69.

- Dramatically reduce benefits for upper-income earners (despite them having paid into the system their entire working lives).

- And eliminate the cost-of-living adjustment for certain earners.

This isn’t partisan bickering. There are a$$holes on both sides, and most of them are millionaires who don’t represent our best interests nor require Social Security to keep them afloat in retirement (which, given their advanced ages, is overdue).

Pointing this out shouldn’t be considered a contentious statement no matter which party you affiliate with: Americans who’ve labored for decades deserve a comfortable and financially stable retirement.

If you have a 401(k) with a match, make sure you’re meeting it. Don’t use your 401(k) as an excuse to not fund an IRA. If you max out either (or both), focus on dividend-paying equities in an investment account to help bolster your income later in life.

Because now more than ever, the onus of saving for retirement is on you.

TL;DR

Older Americans are the fastest growing segment in the workforce. To avoid the un-retirement trend, be steadfast in your savings plan, take advantage of the IRS’s increased contribution limits for 2024 and focus on a blended income strategy.

One Response