Trump’s Policies Are Tanking the Economy

TL;DR

As the president’s tariff-induced trade war continues, signs of economic weakening are accelerating. Meanwhile, the administration’s messaging is in direct conflict with reality. Investors looking for answers will have to sit tight, as the real impact of Trump’s tariffs may not be realized until the end of Q2.

It’s May 1. Spring has sprung. We’ve turned over a new leaf. And when it comes to tariffs, there may actually be good news.

Last week, Trump shared some promising developments with Time magazine. Evidently, countries have been calling him nonstop. “I’ve made 200 deals,” The Art of the Deal author and man who bankrupted multiple casinos said.

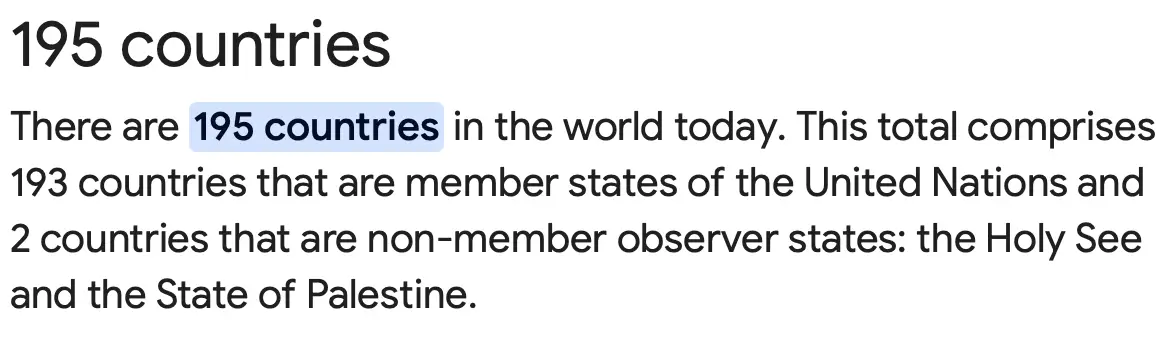

Unfortunately, and unbeknownst to the president, there aren’t 200 countries on Earth to make deals with:

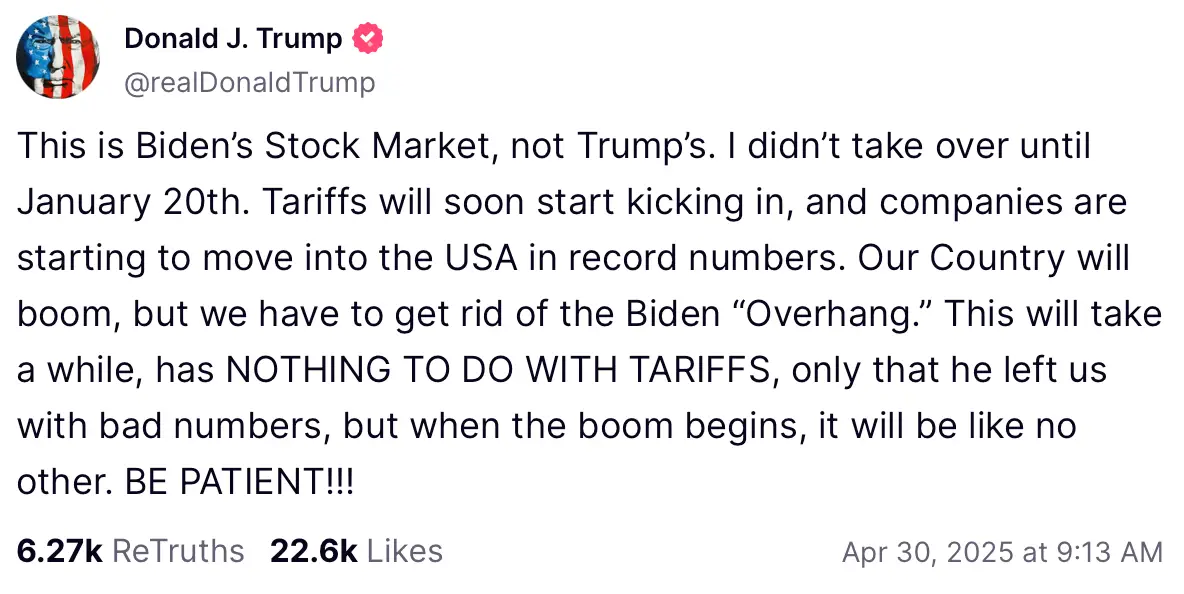

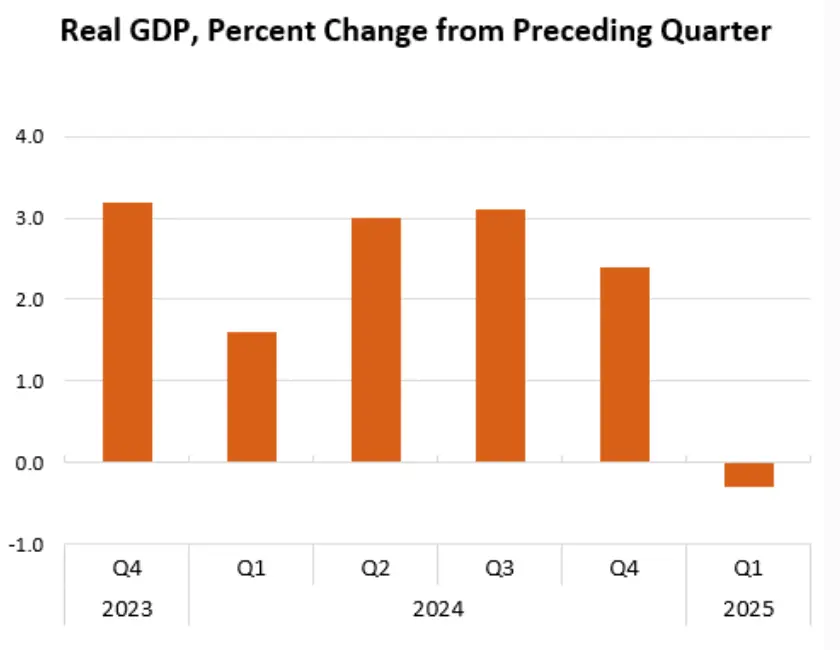

So, we call bullshit. But instead of focusing on how — in just 100 days in office — his tariff policy has tanked the markets, contracted our nation’s GDP in Q1 and caused the value of the U.S. dollar to plummet, Trump did what he does best. In a social media post this week, he shifted blame to the former administration, claiming this isn’t his stock market:

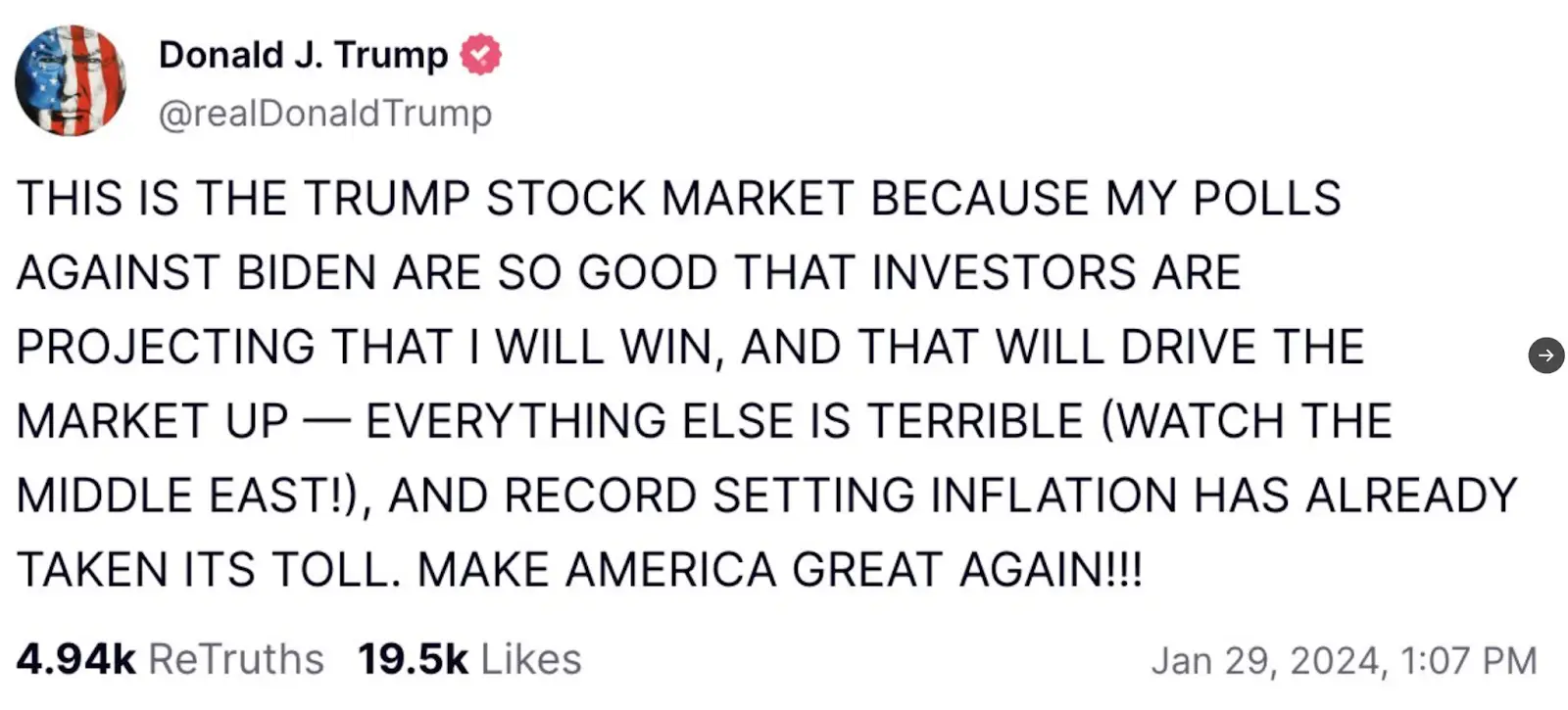

Feel free to laugh, because if you can’t laugh, the incessant gaslighting may cause you to go insane. Trump’s still pointing the finger at the former president. But while Biden was still in office and the markets were pumping out enormous gains, according to Trump in January 2024, that was his stock market:

So, to summarize, when things are good, he takes credit. But when everything goes to shit (which currently is the case), blame is assigned elsewhere. If this pattern sounds familiar, it should be if you’ve ever parented a toddler, a teenager or a senior citizen experiencing cognitive decline.

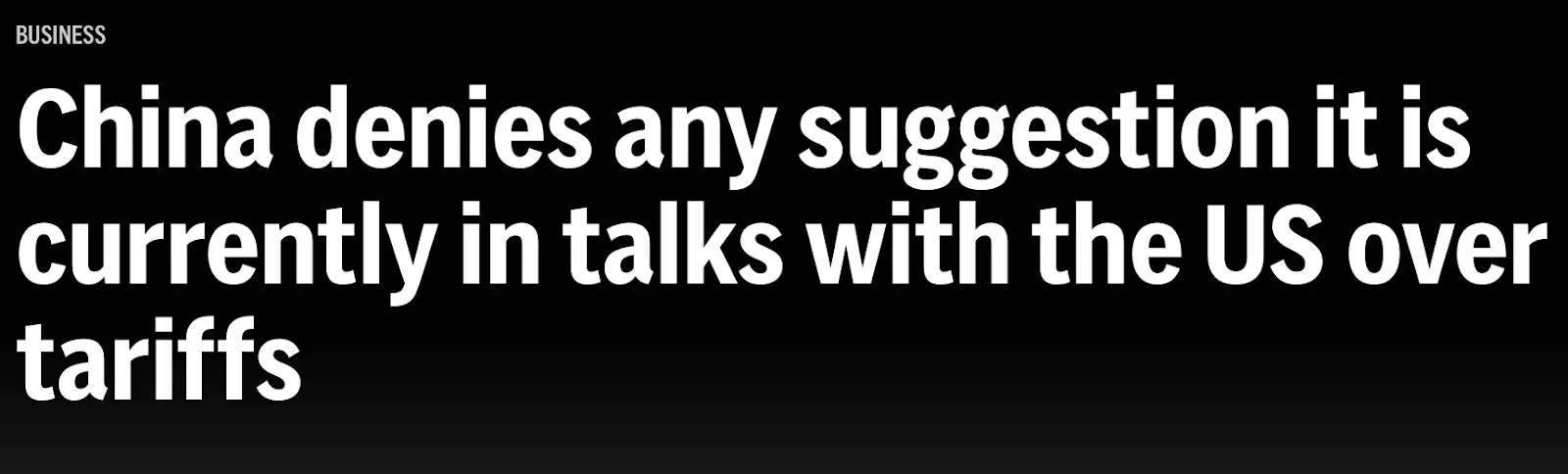

At the very least, the administration has said that the president of China has personally called Trump and they are negotiating 145% tariffs that — if not addressed — could cripple the global economy as the world’s two largest economies enter a standoff.

Wait … this just in:

So more lies and more bullshit. So much bullshit that if bullshit was a commodity, it’d be doing as well as gold and other safe-haven assets that investors are fleeing to in order to avoid the turmoil Trump has injected into the equity markets.

This isn’t opinion, either. To some extent, we wish it was. But the facts support the notion that we are undergoing a rapid and historic economic and market collapse. Last week, the Wall Street Journal reported that the S&P 500’s performance since Inauguration Day was the worst for any president up to that point going back to 1928. The Journal also reported that the Dow was on track for its worst April — a historically strong month for the markets — since 1932.

Thankfully, there are still some adults in the room whose messaging is objective and factually based. Analysis by prominent economists indicates that we are heading into a voluntary trade reset recession (VTRR). To understand a VTRR, imagine you’re leading a race after inheriting a stock market that’s seen the S&P 500 post +23% gains in three of the past four years. Then, you pull out a gun and shoot yourself in the foot.

Torsten Sløk, chief economist at Apollo Global Management, has stated the probability of a self-induced VTRR now stands at 90%. Citing the adverse impact of Trump’s tariffs and the ensuing trade war, Sløk says that small businesses — which account for more than 80% of U.S. employment — will bear the brunt of the president’s shortsightedness.

In a post on the Apollo Global Management’s website, Sløk wrote that although “the administration inherited an economy with strong growth, 4% unemployment, positive hiring and a substantial tailwind from investments … expect ships to sit offshore, orders to be canceled and well-run generational retailers to file for bankruptcy.”

U.S. consumers should start to see those impacts by the end of June. We explained this back in November after the election — at this point, nobody should be surprised by lurking inflation and looming supply shortages.

So what should investors do? Unfortunately, a wait-and-see approach may be the only means of gaining clarity.

Q2 Should Provide Insights

We’re in the midst of Q1 earnings season, and while preliminary reports have demonstrated tenacity at the corporate level, messaging from a number of CEOs is cause for concern. Through two weeks, mentions of “tariffs” and “uncertainty” in earnings calls have spiked 132% and 20%, respectively.

And while April 2 was Trump’s self-proclaimed “Liberation Day,” the impacts of those tariffs will not be realized until the end of Q2 — at the earliest. In the interim, cargo bookings from China have fallen 60%, suggesting that supply shortages are just around the corner.

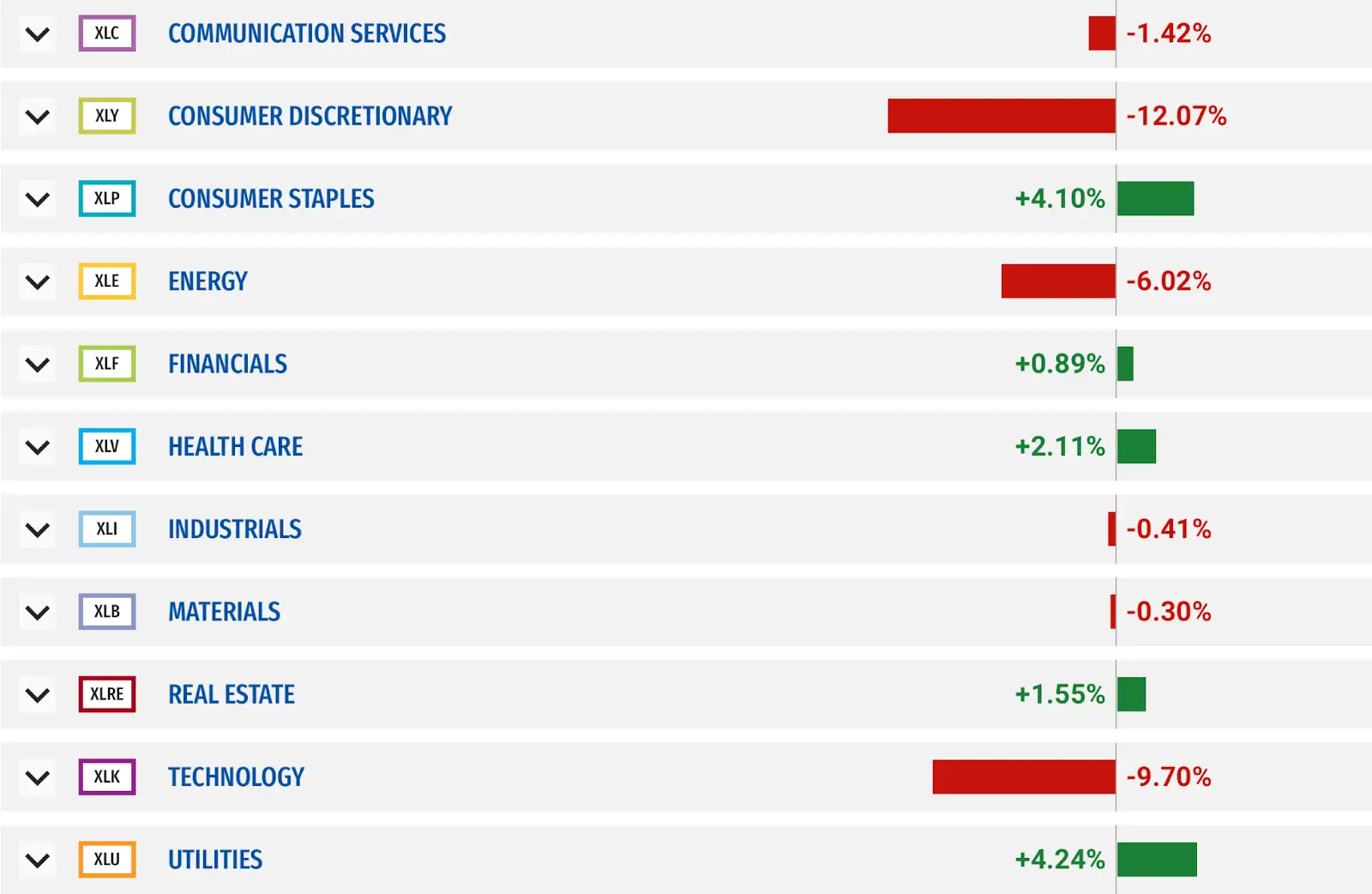

From a market perspective, indications of how this will impact portfolios have already emerged. Of the S&P 500’s 11 sectors, consumer discretionary has seen the worst year-to-date performance. People are eating out less, for example, with hints that a restaurant recession is already here.

Meanwhile, the two top-performing sectors — consumer staples and utilities — are showing resilience. This is something we have repeatedly pounded the table about at Rise & Hedge in the lead-up to Trump’s second term. Long-term opportunities in beaten down sectors like tech are ripe. But in the medium and short term, investors can hedge against ongoing losses in defensive sectors (i.e., consumer staples, utilities and health care) that provide products and services that are inelastic in demand.

The implications of defensive sectors leading the market are equally obvious and concerning. Consumer sentiment is falling faster than at any point since 1990, GDP has reversed from growth to contraction … and the bull market has officially died.

But until we see Q2 earnings, the true gravity of the president’s economic policy will not be felt. We’re not there yet, but if we listen to the “smart money,” the writing is on the wall. Just ask J.P. Morgan’s research team, who “expects the business sector to be poised for a large sentiment shock, which could be one of the factors spurring the economy on toward a recession.”

According to Bruce Kasman, chief global economist at J.P. Morgan, “We anticipate this slide in sentiment to accelerate sharply into midyear.” Translation: If you think things are bad now, just wait until the end of Q2.

Until then, don’t be impulsive. If you’re long, stay put. Heightened volatility is impermanent. And if you’re approaching retirement, consider extending your time horizon.

If you’re looking to grab a quick gain (like we did last week by successfully shorting gold after it hit its all-time high), please weigh the risk-reward ratio. Around 97% of day traders fail. Success can be found in patience, so make time your best friend.