But Celebrity Wealth Isn’t Your Goal

Pop culture isn’t really our thing. Perhaps if TMZ had a financial vertical, it would be. But TMZ and its in kindred media are satisfied with chasing after photographs of celebrities sans makeup taking out their garbage and they seem to be doing fine with that business model.

But there was some TMZ-worthy news last week that caught our attention. Both Taylor Swift and Magic Johnson joined the billionaire club.

Magic became just the fourth professional athlete to accomplish the feat, joining Michael Jordan, Tiger Woods and LeBron James. Perhaps more impressively, Swift becomes the first musician to achieve the rank based solely on her songs and performances.

For the rest of us, it’s a club we’ll never join. George Carlin knew it and now you do, too. And that’s OK. Because celebrity wealth isn’t your goal.

Instead, the remaining 99% of us should be focusing on …

Realistic Financial Goals

One problem with celebrity worship syndrome is that it presents some of the most unrealistic personal finance goals average Americans could set for themselves.

That’s largely because:

- Only 22 states requiring financial literacy education.

- The average American has $7,951 in credit card debt.

- 30-year mortgages now cost 41% of monthly household budgets.

- New car payments now average $729/month.

- Half of Americans have no retirement savings.

- And 62% of us are living paycheck to paycheck.

You know who doesn’t have to worry about that? Taylor Swift and Magic Johnson. You know who does? The rest of us.

Americans suck at saving, let alone investing, and if you look at the bulleted list above, it’s painfully obvious why: It’s difficult getting ahead when you’re disadvantaged from the get-go.

By and large, we’re not taught personal finance basics in the American education system. Even when we are, a significant portion of the population is burdened by student loan debt compliments of a 1,120% increase in college tuition since 1978.

That makes saving for something as common to the American dream as home ownership nearly impossible. And when, by some magnificent effort, people are able to, they’re faced with inordinately high mortgage rates and salaries that’ve failed to keep pace with their workplace productivity let alone cost of living increases.

So where’s that leave us?

Understand Your Debt

You can’t save (or invest) until you establish a debt management plan. That doesn’t mean paying it all off at once. It means understanding good debt vs. bad debt, and from there, making efforts to drastically reduce the latter while properly managing the former.

For simplicity’s sake, ask yourself if the purchase you’re making — or have made — will hold its value and potentially increase your future net worth. Home? Good debt. Credit card purchase of a vintage arcade game for the man cave? Bad debt.

Good debt: Money borrowed to purchase essential items, invest in yourself or leverage existing wealth to manage your finances more effectively. Examples include mortgages, home equity lines of credit (used for home repairs or renovations), student loans and small business loans.

Bad debt: Money borrowed to purchase rapidly depreciating assets or assets for consumption. Typically accompanied by high APR with the potential to damage your credit score. Examples include credit cards, payday loans and car loans.

If you’re burdened by student loan debt and hold multiple loans, consider consolidation. The interest rate environment’s a dumpster fire right now, but when — not if — they come down, you can have a plan in place.

The same goes for credit card debt. If you’re in collection, most agencies will be happy just to have you sign up for a minimum installment payment plan.

Think small, start small. You shouldn’t be saving or investing until you have a debt management plan. Then you can turn to saving and investing.

Don’t Work Until You’re 90

It’s never too early or too late to start saving for retirement. That’s because between 1970 and 2014, the percentage of private sector workers provided with employer-sponsored pension plans fell from 45% to just 2%.

That means the onus of saving for retirement is now on you. So it’s time to get to know your new best friend: compound interest. And over the long term, with commitment, you and your new BFF can go a long way.

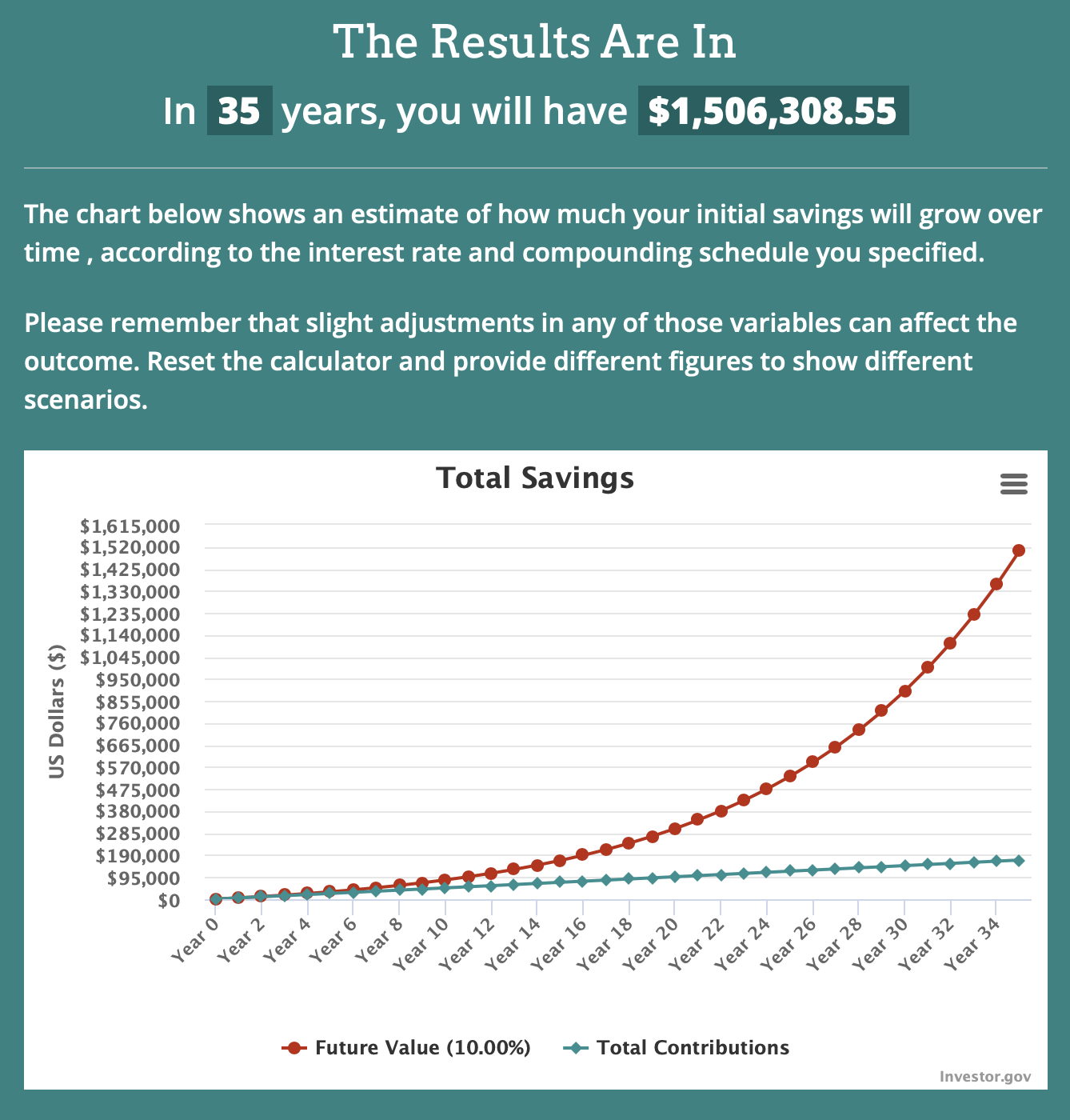

For example, if you open a tax-advantaged Roth IRA with $1,000, contribute $100/week for the next 35 years and invest in the most basic index fund — like the SPDR S&P 500 ETF Trust (SPY), which mirrors the S&P 500 (and its average annual return of 10%) — this is what you’d be looking at upon retirement:

If you increase that contribution to $125/week, you can max out your annual IRA contribution ($6,500/year), and in 35 years, you’d have $1,874,955.54 … or more than $368k more than if you only contributed $100/week.

And while the more than half of Americans with no retirement savings are posting pictures from their most recent vacation or new cars to social media, keep this in mind: Money spent is more easily seen than money saved.

Saving for a Home

Your local bank might seem convenient, but there’s no reason you should be loyal to it. Banks are corporations, not people (regardless of what some Supreme Court Justices have claimed). They’re not your spouse nor your favorite sports team. They don’t deserve your loyalty.

Their sole purpose is to make a profit from your deposits. And if they aren’t paying you a competitive APY, it’s time to pack your sh*t and walk.

Because right now, the best high-yield savings accounts are offering 5.27% with no minimum opening balance requirement … while your nearby branch is offering an industry average 0.46% APY.

Many of these accounts compound interest monthly, meaning your money is making more money in less time, so when mortgage rates come down (and eventually, they will), you’ll have a larger nest egg ready to be deployed.

account.

TL;DR

No matter which celebrity joins the billionaire club next, you shouldn’t emulate them. Being realistic about your personal finance goals is integral to setting yourself up for a comfortable life. That begins with debt management. From there, you can begin saving and investing so, in time, you’ll have that home you always wanted and can retire when the time comes.