Cash ISN’T King

TL;DR

The Fed is expected to make its first rate cut at the end of summer. Meanwhile, as the markets surge, investors’ cash positions have swelled.

Last Monday, in our first of three independence-themed July issues, we discussed why your bank sucks, how it makes 155.55x more on loaning out your money than it does in interest payments to you … and subsequently why you should be using online alternatives.

This week, we’re going to briefly talk about the Fed’s interest rate policy and Americans’ growing cash positions.

According to Betterment’s 2023 Retail Investor Survey, 43% of the 1,200 respondents reported that their cash positions have “Increased Somewhat” or “Increased Significantly” over the past year.

Here’s the thing: Cash doesn’t pay interest. It never has and it never will. When it sits idly, its value is eroded by inflation and its purchasing power is reduced.

So unless you’re a stripper, a fan of nose candy or a senior citizen hunting for an early bird dinner discount, there’s really no need to carry it anymore.

But for those skeptical about the current state of the stock market who are reluctant to deploy that cash … cash alternatives provide a way to conservatively grow your funds while still maintaining liquidity.

What’s Up With Interest Rates?

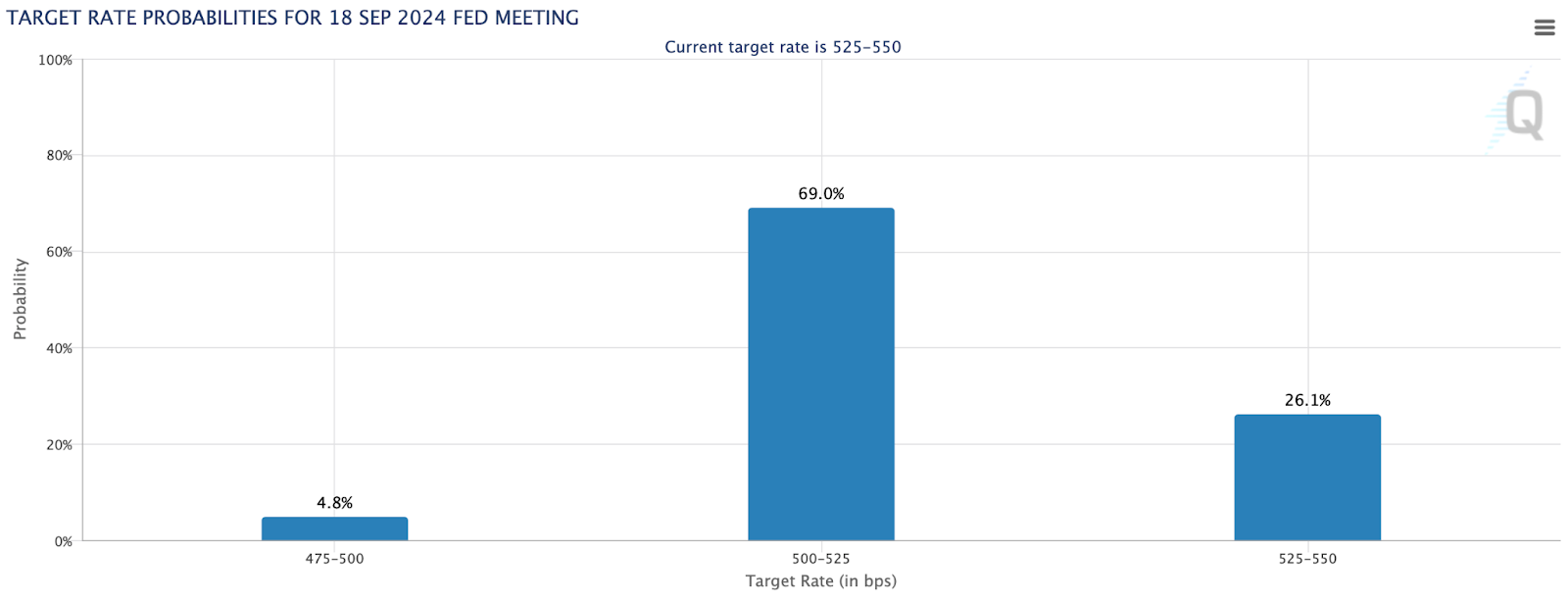

What goes up must (eventually) come down. That’s the prevailing opinion according to the Chicago Mercantile Exchange’s FedWatch Tool, which measures the likelihood of potential rate changes for each of the Fed’s Federal Open Market Committee (FOMC) meetings.

And according to the FedWatch Tool, there’s a 73.8% chance that the Fed will cut its benchmark interest rate during the September FOMC meeting.

But with all of the major stock market indices at or near their all-time highs (again) this year, some people are understandably hesitant to inject any money into what some regard as an overvalued market.

Enter cash alternatives.

What Are Cash Alternatives?

Basically, they’re financial instruments that — compared to other forms of securities (e.g., stocks and ETFs) — offer extremely low risks and conservative returns.

Traditionally, these include high-yield savings accounts (like we highlighted last week), money market accounts, Treasurys and CDs.

And since the former offer variable terms, we’re going to survey the latter, which offer investors fixed terms that should be taken advantage of now before the Fed decides to start cutting rates.

Great Rates Are Still Available

Yes, the idea of holding a cash position is that it is readily available if and when you decide to use it for a purchase or invest it. So while Treasurys and CDs are available with longer horizons, we want to focus on short-term debt instruments so you don’t have to worry about accessing your money when it’s time to.

First, short-term Treasury bills, or T-bills. These are securities issued by and fully backed by the U.S. federal government, which has never defaulted on its debts.

And right now, the coupon rate for an eight-week T-bill is 5.39%.

For comparison, as we mentioned last week, the national average APY for savings accounts is currently 0.45%.

You do the math.

Second, CDs. If you grew up in the ‘90s, you’ll be happy to hear they’re cool again.

Dallas-based NexBank, which is FDIC-insured, is currently offering a six-month CD with an APY of 5.20% and a one-year CD with an APY of 5.40%.

Here’s a reminder that we don’t make any money from our subscribers. We don’t sell. We’re here to democratize access to information that helps you improve your personal financial wellbeing.

But at the risk of sounding like used car salesmen, these deals won’t last.

The Fed is going to cut interest rates, either later this summer or fall or in 2025. If you find yourself sitting on a sizable cash position, now is as good of a time as ever to safely secure +5% returns on those funds.