Dividend Snowballs Require Time, Patience & Perseverance

Dividend snowball /ˈdivəˌdend snōˌbôlˈ/ noun: the process of reinvesting dividends from equities to buy more shares, thereby earning more dividends to reinvest in the future.

TL;DR

For long-term investors, focusing on a dividend snowball can result in substantial passive income later in life. It can take a decade or more to see the results, but once it starts rolling, the momentum can have a life-changing impact on your portfolio.

Last week, an Arctic blast drove temperatures to near-zero in many parts of the U.S. Snow blanketed much of the country. It even got cold enough in South Florida to force locals into sweaters.

But it also afforded children and science deniers a chance to go sledding and demonstrate their complete lack of climate change comprehension, respectively. One thing those two demographics have in common, though: They both enjoy playing with snowballs.

It seems like just yesterday when former Senator Jim Inhofe brought one onto the floor of Congress to “prove” climate change is a hoax (just like eating a sandwich disproves world hunger, or releasing a helium-inflated balloon debunks gravity).

Big brain moves from Jim.

It was a demonstration of flawless logic and stellar theatrics from a senator who, throughout his political career, received campaign donations from companies — like oil major Valero Energy, gas utility OGE Energy and fossil fuel giant Alliance Coal — that operate in sectors that significantly contribute to anthropogenic climate change.

That was nearly nine years ago, and painfully, the scientific literacy of our elected officials hasn’t improved since. Meanwhile, Inhofe, a vocal opponent to the military mandate for COVID-19 vaccines, was forced to retire in 2023 at the spry age of 88 due to — you guessed it — long COVID.

But we digress … snowballs.

That memory inspired this week’s topic. However, rather than using snowballs for political stunts or to assault our least favorite neighborhood kids, we’re talking about how they can set you up for lifelong income.

Dividend Snowballs

Growing a dividend snowball entails reinvesting your dividends from equities — be they stocks, ETFs, REITs, BDCs or MLPs — to purchase additional shares at no out-of-pocket cost. In turn, these shares beget more dividends payments, which can be used to purchase more shares.

Lather. Rinse. Repeat.

This strategy can be accentuated by routinely purchasing additional shares out of pocket. Ultimately, the more dividends that are reinvested, the more your monthly/quarterly/annual payouts will grow. Over time, your snowball accumulates to the point where it can sustain a FIRE lifestyle or carry you through retirement without having to worry about Social Security be stolen from us by our aforementioned elected officials.

Seems easy enough, right? That’s the tricky party. Building that snowball requires time and patience. A lot of both.

This isn’t a strategy suited for day traders, swing traders or crypto bros. It’s aimed at investors with fortitude; those who want to build a portfolio that eventually provides enough dividend income to sustain or supplement their lifestyles, particularly in retirement.

How It Works

Here’s a hypothetical. You own 100 shares of a $25 stock paying an annual dividend of $1/share. After one year, your dividend distributions amount to $100, which when reinvested can purchase an additional four shares at $25.

The following year, you now own 104 shares yielding $104/year, which can be reinvested to purchase an additional 4.16 shares at $25. After year three, the dividends from those 108.16 shares enable you to purchase an additional 4.32 shares, bringing your total to 112.48 shares at just the initial cost of $100.

Thus the snowball continues to grow as it rolls downhill.

However, that hypothetical assumes the company doesn’t raise its dividend and the share price doesn’t appreciate. By investing in companies with a history of raising their dividends — like Dividend Aristocrats and Dividend Kings, which have done so for 25 and 50 years consecutively — you’re helping ensure that the overall yield on your portfolio isn’t just maintained but steadily grown.

Here’s another example:

- You purchase 100 shares of Dividend King Altria Group (MO) at its current share price of $40.34. The stock’s gained 6.95% over the past 10 years and has a dividend yielding 9.72%, which it’s raised for 55 consecutive years.

- In addition to those 100 shares, you invest another $100/month every year into Altria, doing so in a Roth IRA for tax advantages.

- Altria increases its dividend by 4.3% annually (which it did last fall to align with its progressive dividend goal of increasing the yield by “mid-single digits per share growth annually”).

- The company’s able to replicate its 10-year growth rate of 6.95% over the following two decades.

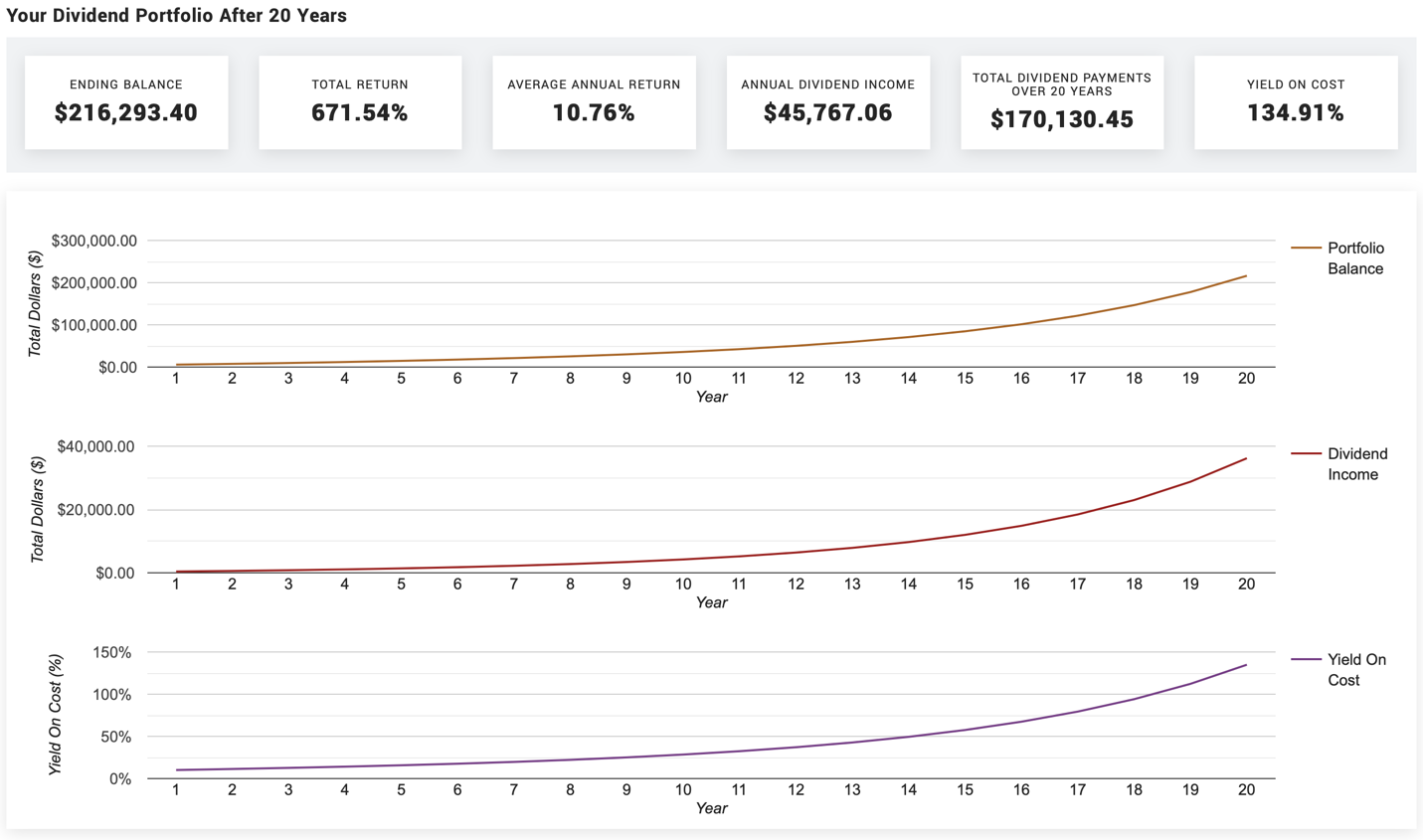

The Result

After 20 years, the Altria component of your dividend snowball alone is worth $216,293.40, providing you with $45,767.06 in dividend income/year, or $3,813.92/month.

That equates to a yield on cost of 134.91%, underscoring the power of reinvesting dividends.

But it’s important to remember that this isn’t an overnight strategy. As you can see in the charts above, the portfolio balance and dividend income don’t change significantly until year 10 and then really take off around year 15.

Again, the key to this strategy is patience, of which Jean-Jacques Rousseau remarked “is bitter, but its fruit is sweet.”