REITs Look to Recover After a Painful Year

Over the course of the pandemic, we learned some irrefutable truths. Among them:

- Teachers and nurses are criminally underpaid.

- Common knowledge is extremely uncommon.

- And workers are more productive in remote settings than in the office.

That last one’s germane to today’s issue. Despite countless studies demonstrating those productivity increases, some companies are ignoring the data and — in a last-ditch effort to prove that “corporate culture” benefits from in-person attendance — forcing workers back to the office.

The media even has an acronym for it. While 2020 gave us WFH (work from home), 2024 gives us BTO (back to the office).

BTO has little to do with augmenting interoffice camaraderie, no matter how management teams try to spin it. And it doesn’t matter how many pizza parties they throw or ping pong tables they purchase; it’s not about corporate culture.

It’s counterproductive, too. A recent survey of 1,400 full-time employees who were forced to return to the office found elevated rates of “burnout, stress and turnover intentions.” And according to employment website Indeed, replacing workers isn’t cheap. Per employee, companies can expect to pay:

- $7,500–$15,000 on professional recruitment services.

- At least $100 per background check.

- $1,000–$5,000 on employee referral bonuses.

- $1,000–$5,000 for onboarding.

- And $722–$1,438 for training.

So if the goal is to foment resentment, encourage workers to seek employment elsewhere and then spend over $20,000 replacing them … BTO mandates are working exceptionally well.

These companies can’t admit they overextended themselves with office leases, or that commercial real estate (CRE) is a drain on the average company’s bottom line.

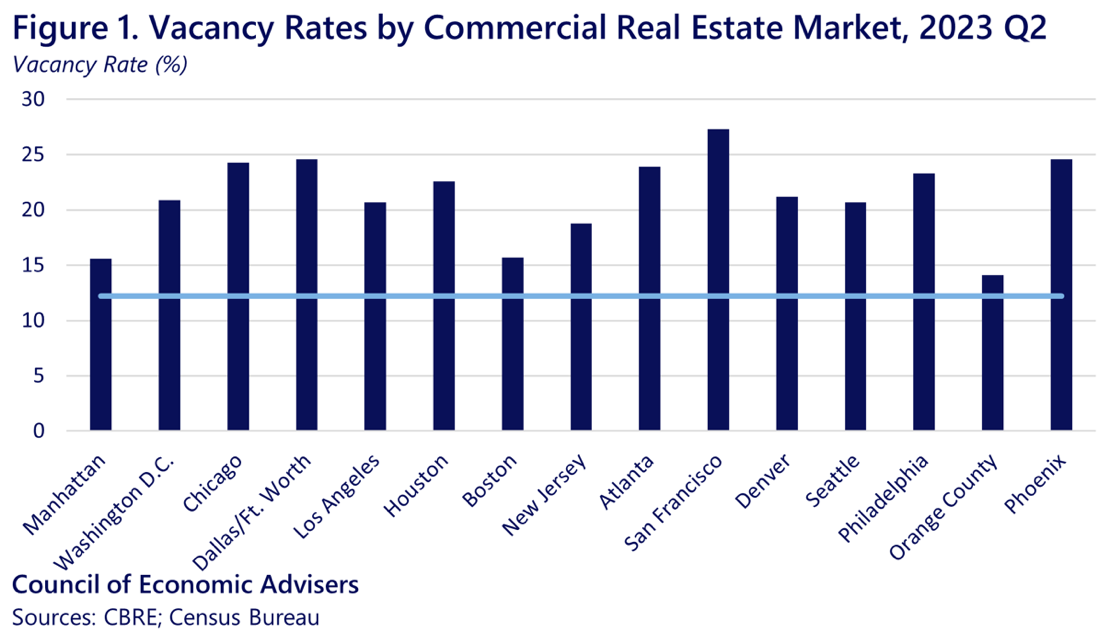

There are, however, plenty of forward-looking companies that have recognized this, which is why office buildings around the country are still experiencing incredibly high vacancy rates as more productive and happier workers remain in remote settings.

The horizontal blue line in the chart below represents CRE’s vacancy rate at the end of 2019, with some markets more than double that rate through Q2 2023:

No matter how they try to sell BTO, the primary reason some companies are attempting to revive cubicle farms is to save face. But as Aldous Huxley once mused, “Facts do not cease to exist because they are ignored.”

And oh boy does this country love to ignore facts. According to consulting and advisory firm Deloitte, in 2024, the CRE market is forecast for its lowest revenue on record. And the result is long overdue …

Office-to-Apartment Conversion

America’s in the midst of a housing crisis. While wages have mostly stagnated for … *checks calendar* … four decades, the average cost of an American home increased 721% since 1980. Meanwhile, there are 2.5 million homeless children in the U.S. and rent has more than doubled since 2000.

Meanwhile, the chances of your landlord being a billion-dollar corporation are increasingly likely. Blackstone (BX) owns 61,964 single-family homes, Progress Residential owns 82,502 and Invitation Homes (INVH) owns 81,716.

But today, we’re not discussing those companies. We’re not going to talk about commercial real estate investment trusts (REITs), either, given that earlier tidbit about how the industry’s on pace for its worst year on record.

Instead, we’re focusing on residential REITs. And while we recognize that converting downtown 50-story towers from offices to apartments isn’t going to solve the home affordability crisis, hopefully it can — to some extent — alleviate housing shortages in America’s cities.

That’s why we’re happy to see metropolises like New York, Washington, D.C. and Dallas leading the way in office-to-apartment conversion. Those cities are first, second and third, respectively, in those efforts.

REIT-diculous Yields

In 1960, Congress created REITs to provide individual investors with opportunities to invest in large-scale, income-producing real estate projects. This entails REITs specializing in mortgages, apartments, offices, homebuilders, trailer parks, industrial properties, healthcare facilities or the ownership and operation of any of the aforementioned.

What makes REITs so appealing — particularly for investors looking to diversify how they generate cash flow — is that by law, they must distribute at least 90% of their taxable income to shareholders in the form of dividends.

And while office CRE is beginning to look like a relic, it’s a different story for resident REITs, which have tailwinds at their backs:

- This year, the Federal Reserve’s expected to begin reducing interest rates, making the cost of borrowing — for REITs and prospective homeowners — more affordable.

- The Fed’s stabilization of rates already reversed what was a year of losses for REITs, totaling -24.95% in 2023.

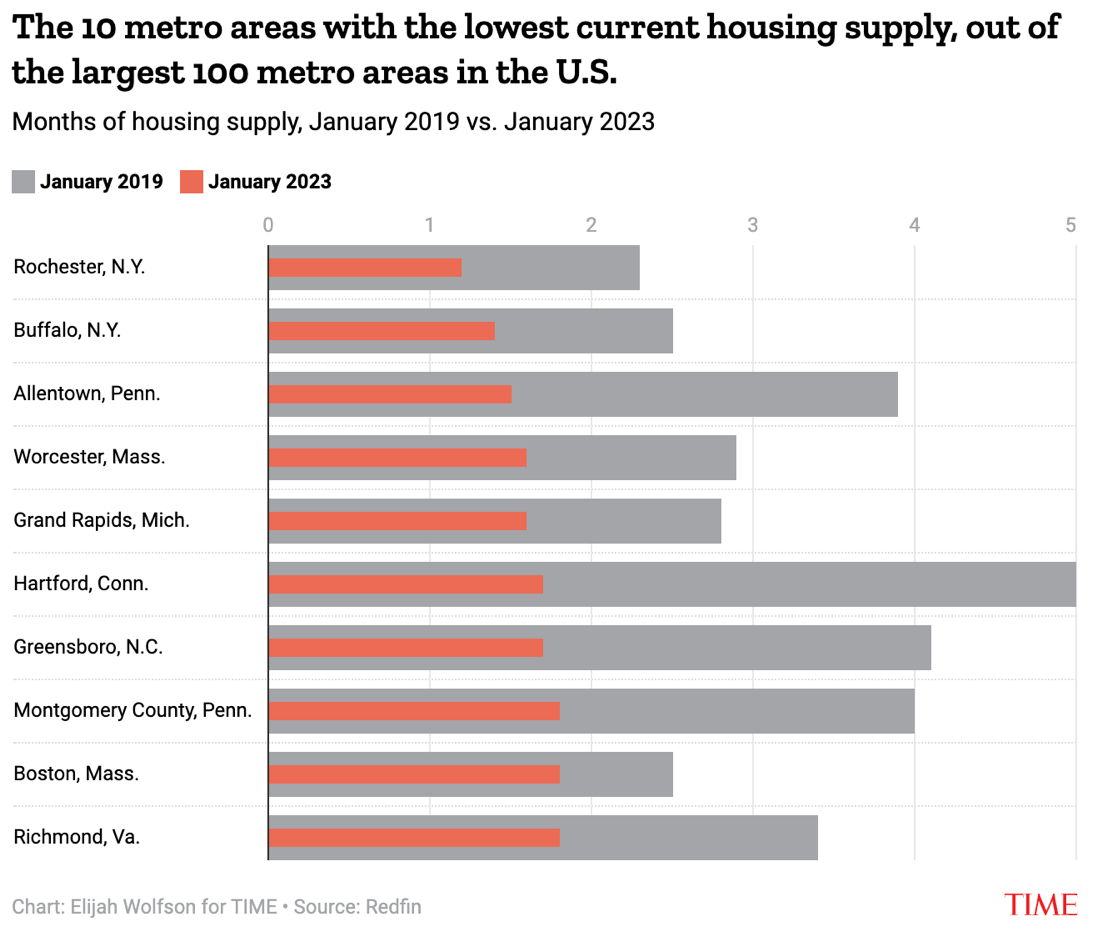

- Home inventories remains painfully low, down 41.8% from pre-pandemic levels, with the 10 metro areas in the U.S. with the lowest inventory all under a two-month supply.

- As of Dec. 29, publicly-traded REITs were trading at a median 10.7% discount to their actually net asset values.

Translation: Many of these companies are still on sale, and because of these tailwinds, REIT fund managers expect the sector to deliver double-digit returns in 2024.

Our Pick

While there’s no shortage of REITs offering strong yields and tremendous growth potential, Camden Property Trust (CPT) caught our attention as one of the largest publicly-traded multifamily companies in the U.S.

The $10.31 billion company’s portfolio of multifamily apartment buildings boasts an occupancy rate of 97.5% across 172 properties with 58,000 units in major markets from Florida north to Atlanta and Washington, D.C., and west to Texas, Denver and California.

CPT is down -21% over the past year, but since it’s one-year low on Oct. 30, the REIT is up 15%. It yields 4.14%, or $1/share quarterly. After a down year in 2023, the company’s consensus EPS for Q1 2024 is 39 cents — a metric it hasn’t missed since Q3 2022.

Based on 17 Wall Street analysts, CPT receives an average one-year price target of $104.63 and a high-end estimate of $138. Currently trading at $96.57, the average price target represents upside potential of 8.3% while paying investors a considerable yield.

Until next time,

Team Rise & Hedge