Here’s Why & What to Do About It

TL;DR

The market is undergoing a pullback dating back to mid-February, and tariff-fueled trade wars are about to accelerate volatility. Uncertainty remains the theme for 2025. In the short-term, that means taking a wait-and-see approach and — importantly — not panic-selling.

There’s a saying that the stock market takes the stairs up but the elevator down. And since the second half of February began, that’s exactly what it’s felt like to investors who had been enjoying +24% annual returns three out of the past four years.

While we said in our last issue that we’d have a new recommendation today, present market volatility makes doing so imprudent on our parts. Instead, we’re going to continue to monitor the performance of that pick as well as broader market conditions.

As for today, we’re going to explain some components contributing to the uncertainty that’s been plaguing investors this year, and how you can approach it.

Recession Watch?

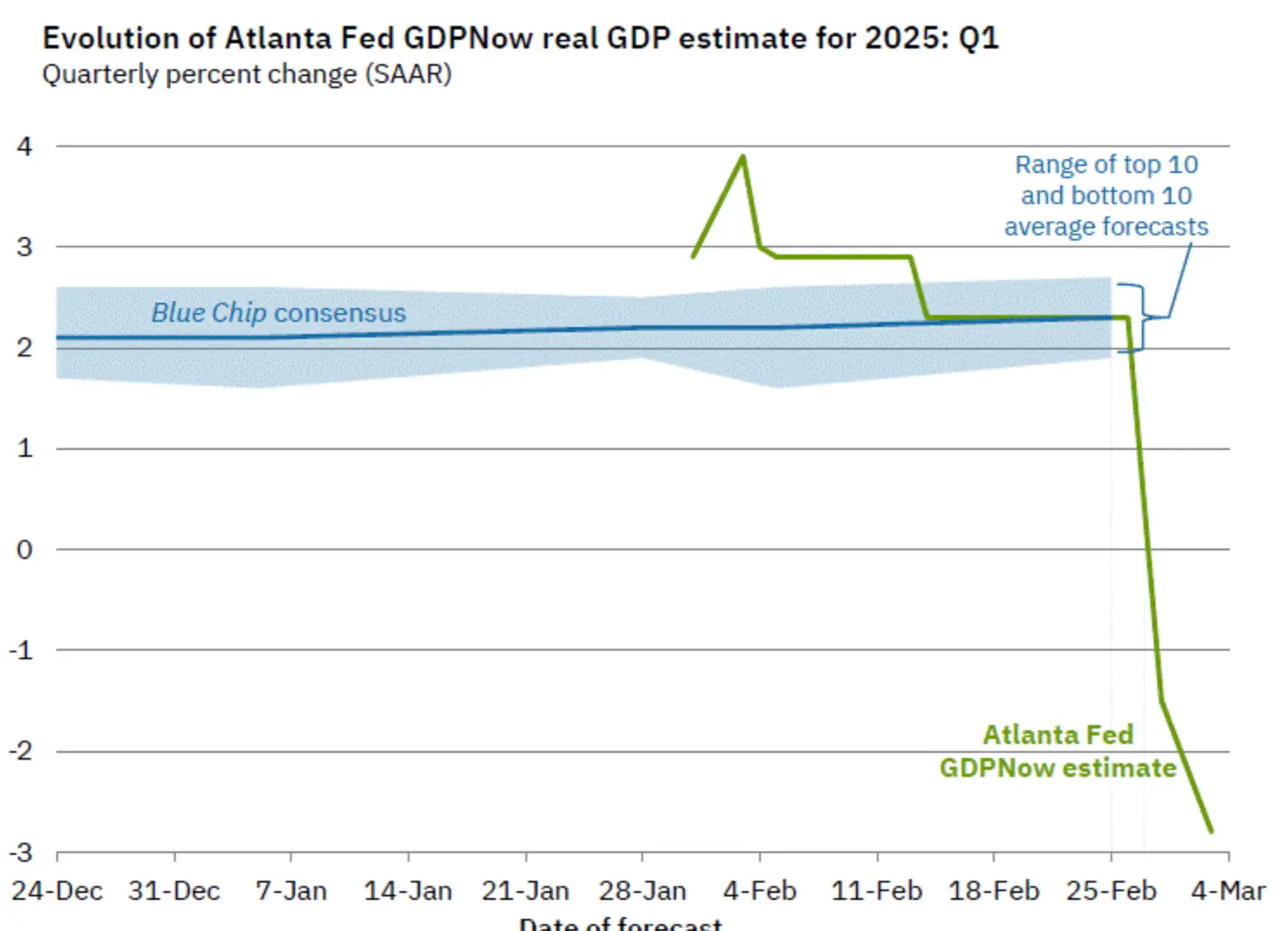

Last week, the Atlanta Fed revised its Q1 GDP forecast to the downside. Big time. Prior to last weeks’ consumer spending report and renewed tariff rhetoric from the White House, the GDPNow tool indicated quarterly economic growth of 2.3% for the quarter. Looking back to late January, that figure was as high as 3.9%. Now, the central Bank is projecting a contraction of -2.8%.

That means in Trump’s first quarter as president, the forecasted GDP is now 221.74% lower than it was when he took office in January. The preferred measure of a recession is two consecutive quarters of economic contraction.

But as much as we’ve enjoyed assigning blame to where it’s due, the orange occupant of 1600 Pennsylvania Avenue isn’t entirely at fault. Signs of a slowdown have been around since late 2024. Inflation began ticking up again last fall, and when the calendar turned, it continued.

However, there is no denying that Trump has played a significant role in the sudden — and dramatic — downside revisions for the GDP. Unemployment claims are at a three-month high and consumer confidence registered its lowest monthly decline since August 2021. The president has compounded and accelerated the factors contributing to the macro environment.

Investor Sentiment Tanks

Earnings season is winding down, and by and large, it was a successful one:

- Companies reported 18% year-over-year (YoY) profit increases.

- Magnificent Seven companies saw YoY increases of 37%.

- Financial companies (like we suggested months ago that you should consider), saw 50% YoY increases.

But according to a report from LPL Financial, “With new tariffs in place and more likely on the way, on top of mounting evidence that the U.S. economy is slowing, achieving double-digit earnings growth in 2025, as many expect, will be a tall task.”

If you’re a Rise & Hedge subscriber, that shouldn’t come as a surprise. After the election, we told you in November that tempered growth is the expectation going forward.

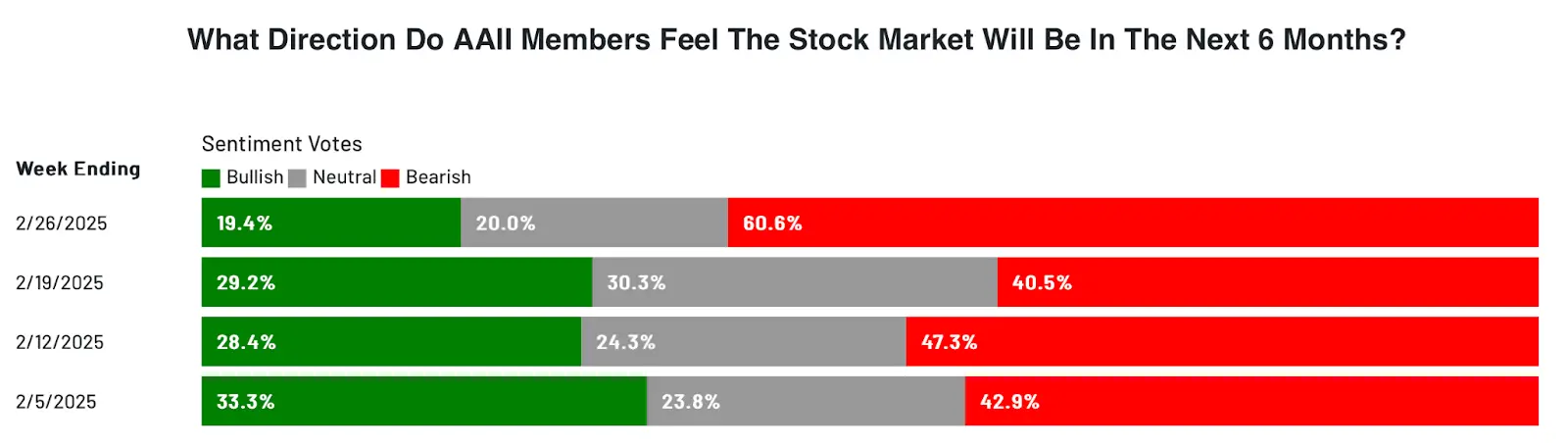

But evidently, some investors are just now piecing it together. According to the American Association of Individual Investors’ weekly sentiment survey, 60.6% of investors report a bearish outlook:

That’s the lowest since September 2022 (29 months ago) and the largest single-week increase since August 2019 — or 66 months ago — which just happened to be during Trump’s last presidency.

Shocking, right?!

It’s almost as if a president who relies on contrarianism, divisiveness and vitriol as much as he does tariffs and the McDonald’s app somehow isn’t good for the economy let alone the market.

As we write this, the S&P 500 is in the midst of another day in the red — its fifth in the last six trading sessions. Since Jan. 21 when the market reopened after Trump’s inauguration, the market has handed investors a -3.88% loss. And since hitting its year-to-date high on Feb. 19, the S&P has fallen -5.36%.

Trump’s Tax Plan Wake-up Call

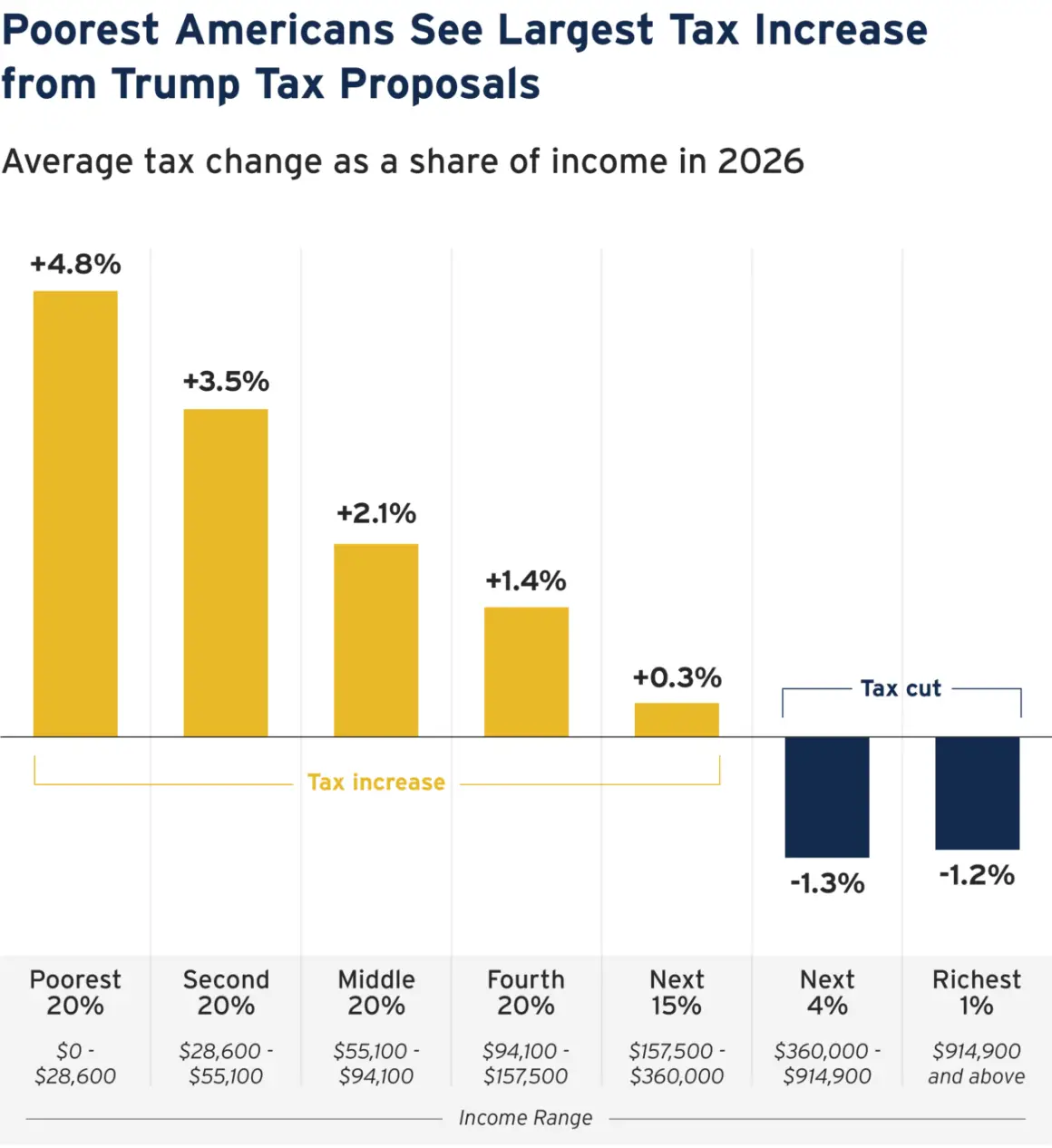

Another thing that may have investors — and even Trump supporters — down is his tax plan, which is a gut shot to anyone making less than $360,000/year. And if you’re reading this, we suspect that includes you.

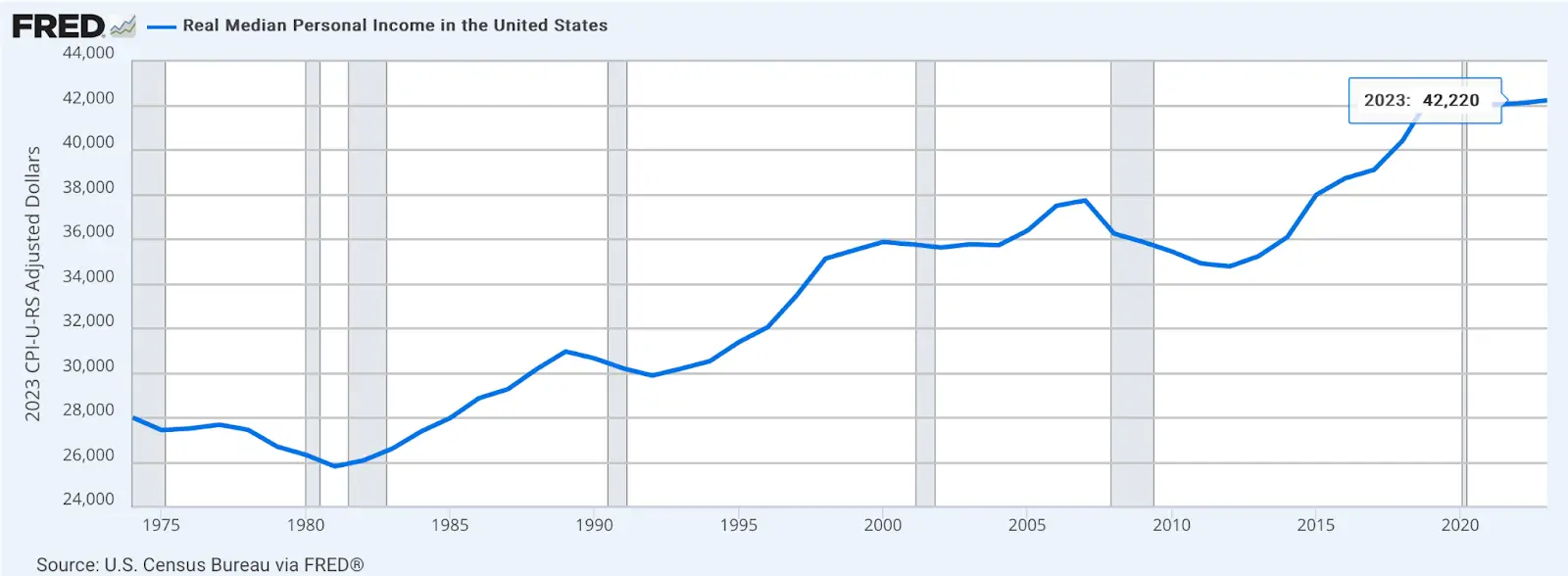

That’s because in 2023, real median personal income (i.e., adjusted for inflation) in the U.S. was $42,220:

While 2024 data hasn’t been released yet, we suspect that the everyday American didn’t receive a $307,800 raise last year.

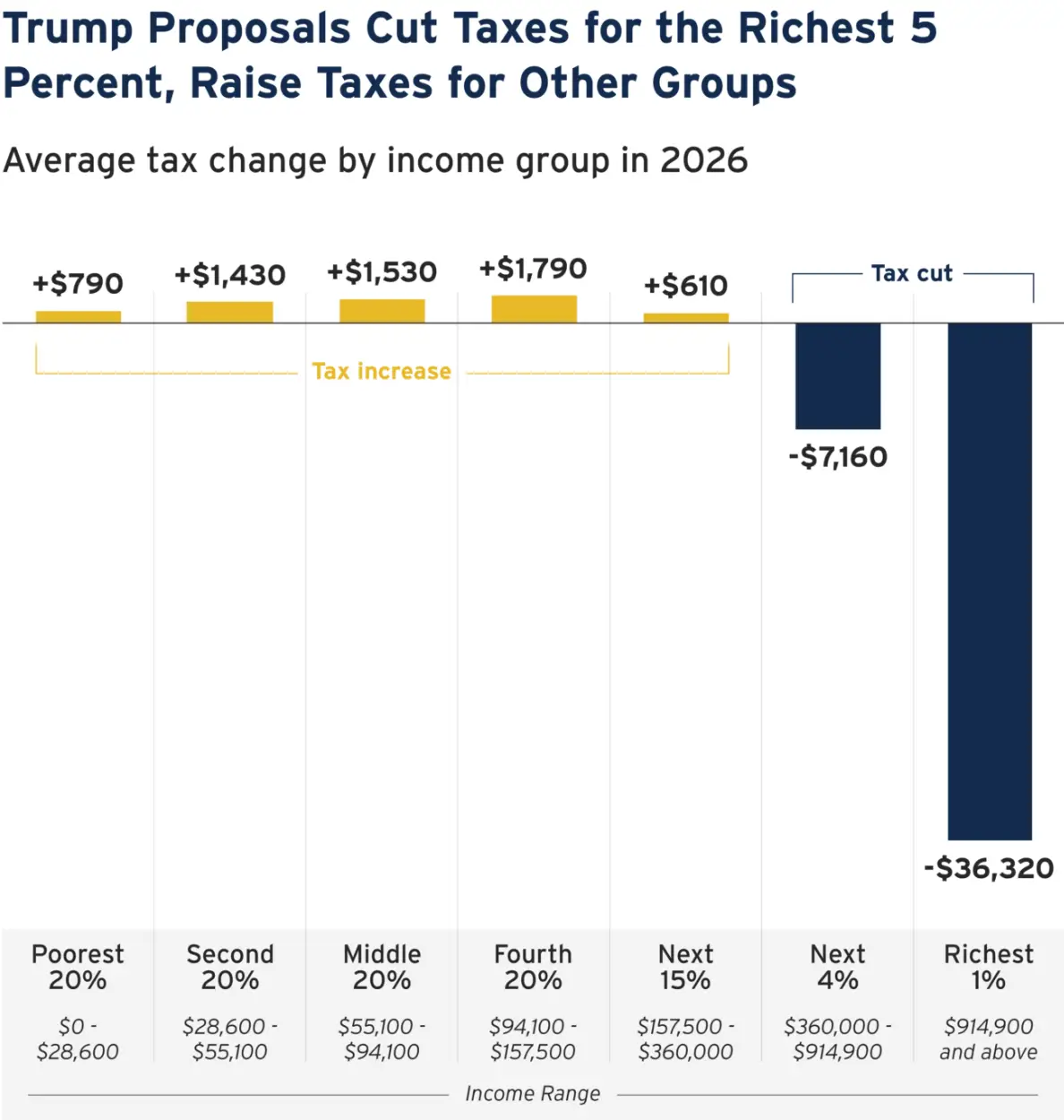

Why is it a gut shot? Because on top of prices rising in perpetuity, you’re also going to be doling out more of your hard-earned money in federal income taxes beginning next year:

The results are predictable: Less money to allocate toward increasingly expensive goods and services, which in turn decreases consumer confidence and has an outsized impact on corners of the market that are either cyclical, reliant upon consumer discretionary spending or both.

So how much less? This much less:

Don’t take our word for it, though. Take the word of the aptly named Institute on Taxation and Economic Policy.

What the plan doesn’t include: No taxes on tips, no taxes on Social Security income — two major campaign promises Trump made to everyday Americans. Instead, the wealthiest Americans are set to receive another sizable tax break while the rest of us get the short end of the stick.

We’re not going to dive into how the administration plans to make up for the shortfall in tax revenue, but if you or someone you care about is one of the 72 million Americans enrolled in Medicaid or the 42.1 million enrolled in SNAP, you might want to click those links.

Takeaways

So what’s this all mean? Negative sentiment is contagious, but in this instance, it’s also justified. While equities are currently overpriced from a price-to-earnings standpoint, that doesn’t mean they can’t continue to inflate before things come back down to Earth.

We’re due for a correction, and given the average lifespan of a bull market, we very well may be approaching a bear market. That’s not our opinion, either. Many of the CIOs and CFPs we’ve spoken with have said that they believe we’re firmly in the late stages of the current bull run.

We don’t foresee the market settling down in the short-term, but we’re trying (as best as humanly possible) to remain optimistic. For now, take these steps:

1. Sit tight. We’re not making a recommendation this week, but we’ve been doing our homework and have our eyes on one that will share with you as soon as the market (hopefully) calms down. If you’re thinking about buying low on some stocks that’ve been beaten up lately, consider how much lower they could go. This very well could just be the start of a full-blown correction.

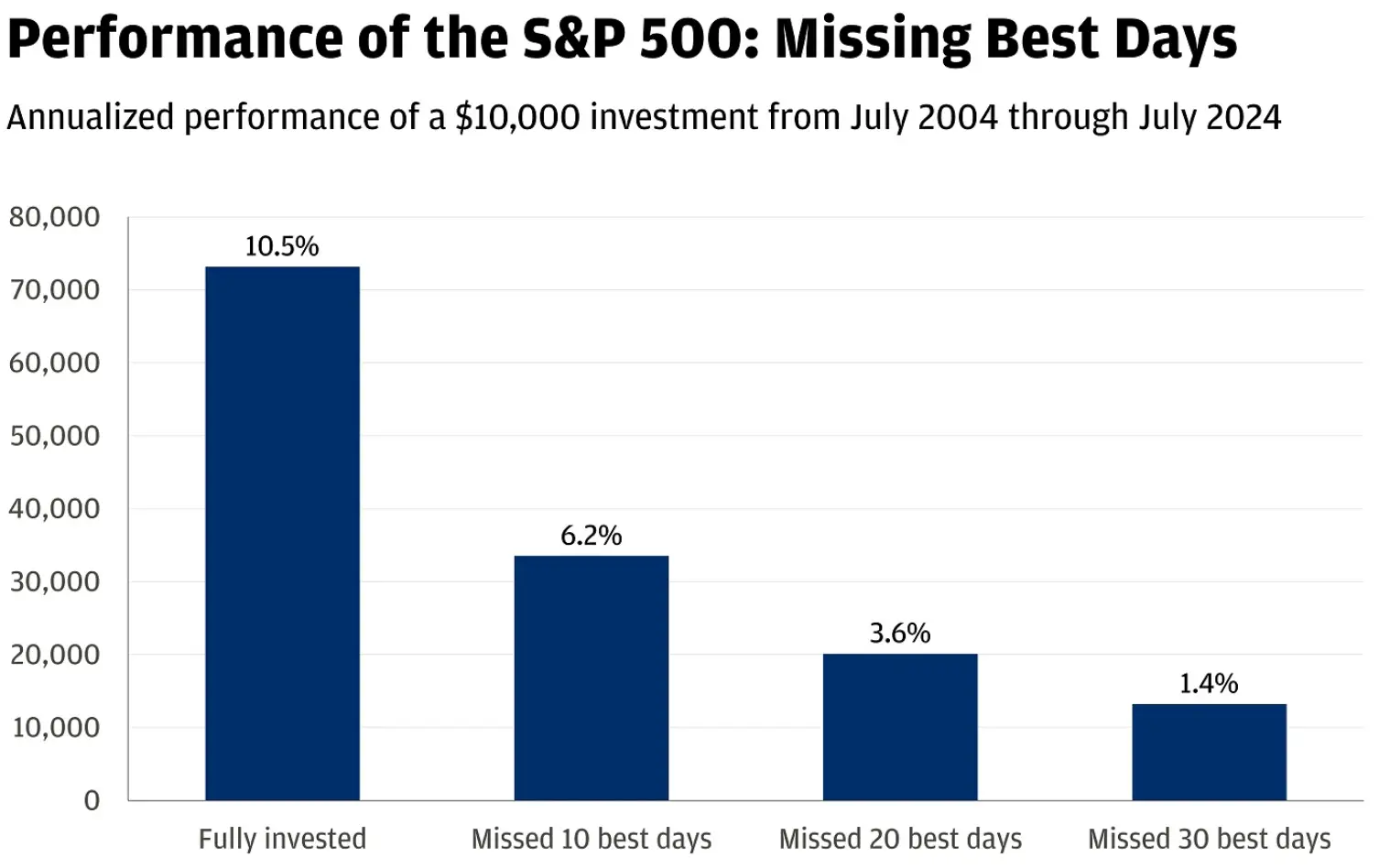

2. Don’t panic sell. Studies show that attempting to time the market is a fool’s errand. In fact, those who do and wind up missing the best days of market performance see significantly reduced long-term growth potential:

3. Subscribe and share Rise & Hedge: We’re here to help democratize financial literacy and provide you with investment insights that don’t cost you the subscription fee some “guru” is charging for his hot takes or the commission a financial advisor is going to charge your to just tell you to dump your money into an index fund and not pay attention to the market.