$100 a Month Can Go a LONG Way

TL;DR

America is in the midst of an affordability crisis with no solution in sight. As parents, it’s incumbent upon us to provide a better future for our children. This strategy can help ensure that.

Last week, we discussed why index funds are likely the best investment for the majority of people. Individual stocks outperforming the market are at historic lows, and putting your money into a fund tracking a benchmark index is easier than attempting to determine the handful of winners outpacing said index.

This week, we’re going to talk about how you can use that knowledge to set your child on the right path in life with — excuse the infomercial language — a commitment as low as $100/month.

Given the staggering increases to costs of living in the U.S., we figured $250k is a good target number that — surprisingly — many Americans can actually afford to target.

But first, let’s briefly discuss …

How EVERYTHING Costs More Nowadays

Younger people in 2024 have it harder than older generations did at the same age. If you’re still denying that, congratulations! You’re a poster child for the fictitious “bootstrap” generation who’s incapable of seeing how, for the first time in U.S. history, subsequent generations are largely unable to achieve better financial footing than their parents.

For the rest of you who are open-minded and empathetic, here are some quick hits:

- The cost of housing in this country is absurd. Last week, Zillow reported that there are now 237 U.S. cities where a starter home costs at least $1 million.

- The home-price-to-median-household-income ratio is at an all-time high. Historically, the average single-family home in the U.S. costs 5x the average yearly household income. Today, that figure stands at 7.7x … more than at the peak of the housing bubble and nearly double what the ratio was in the early 1970s when a home cost around 3.62x the average salary:

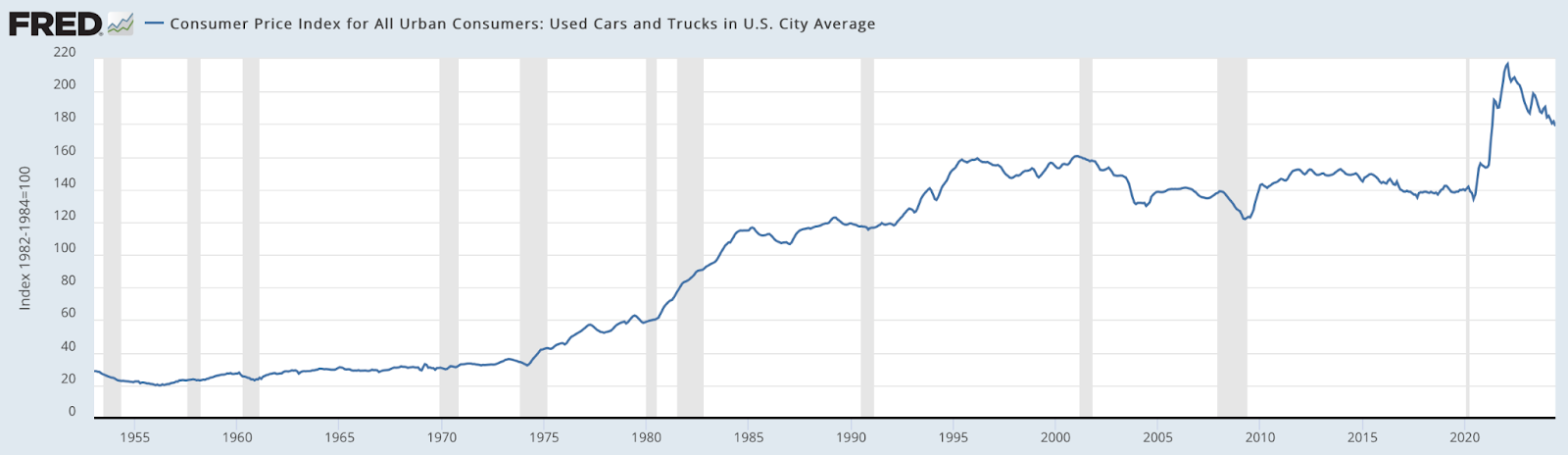

- Think opting for a used car rather than a new one will help you save money? Nope. Though it’s down from 2022 highs, the Consumer Price Index for used vehicles is at 178.83. Returning to the early ‘70s for context, the index reading was 30.1, meaning used cars today cost 178.83% more than they did then:

- How about healthcare? U.S. expenditures reached $4.465 trillion in 2022, up from $74.1 billion in 1970. That marks an increase of 5,925.64%.

Fun fact: Our healthcare system isn’t actually broken. It’s functioning precisely how it was designed to by those who profit from it. (Here’s an ETF we wrote about last year that can help you get a piece of that unscrupulous money pie.)

But, you know … “buy less avocado toast and Starbucks.” That’ll fix it!

We know opinions are like certain body parts: Everyone has them and they mostly stink. But in a country that’s running amok with disinformation and leaders who disseminate blatant lies that are blindly accepted by grown-ass adults who are too lazy to fact check anything, there’s always a boogeyman.

And now that boogeyman is often young Americans who are sick and tired of the cesspool that’s been left behind by preceding, prosperous generations.

Whether people acknowledge the facts or have fooled themselves into thinking that the success they’ve accomplished is solely attributable to their sweat equity doesn’t matter. Your children will have it harder in this world than you did. Period.

And that’s not. Their. Fault.

So how’s a net worth of $250k achievable for them by the time they turn 30? The not-so-secret secret, according to Einstein, is the eighth wonder of the world …

Compound Interest

You’re probably never going to win the lottery. And despite America’s increasing addiction to gambling, that’s not a sound plan for financial wellbeing, either.

Compound interest takes time and it takes patience. But it works.

The idea is that, over years and literal decades, compound interest builds upon principal balances and accrued interest. That allows your money to grow exponentially faster.

And when bolstered by recurring contributions — whether weekly, monthly or annually — account balances really begin to balloon after the first 15 years.

The S&P 500’s Historical Performance

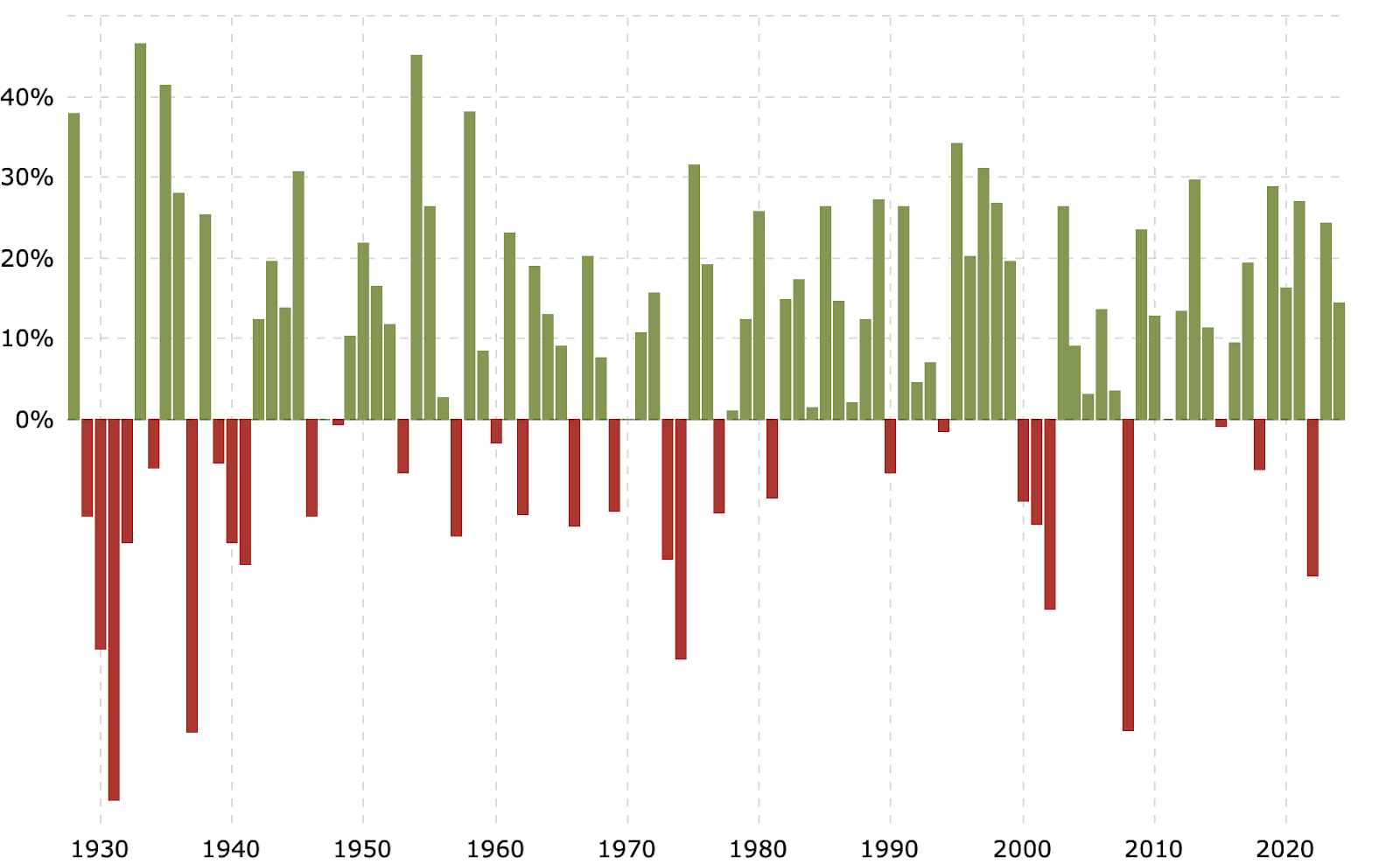

So what does this have to do with index funds? The S&P 500 offers many of them, but more importantly, the index itself is the source of an average annual return of 10% over the past 30 years.

Better yet, bull markets notably outnumber bear markets since 1930, and in the past five years, three have seen gains (28.88%, 26.89% and 24.23%) larger than 2022’s bear market loss of -19.44%.

Another fun fact: Despite March 2020’s pandemic-induced selloff, that year still ended in the green with a 16.26% gain.

So while the S&P 500 has returned an average of 11% over the past 20 years and 15.6% over the past 10, we’re sticking with the conservative 10% figure over the past 30 years.

Compound Interest Calculator

If you’re uncertain this can work, the government provides a compound interest calculator that you can use (and adjust per your preferences) to better visualize the strategy.

Here are the calculations we used:

- Initial investment of $1,500

- Monthly contribution of $100

- 30-year timeline

- Estimated 10% return

- Compounded quarterly (which S&P index funds do)

One Response