Inflation is eroding your savings. Here’s how to get more bang for your buck.

That bank around the corner is really convenient, isn’t it? They’re always smiling and handing out lollipops.

But smiles and lollipops don’t fight inflation. Neither does the abysmal 0.24% interest rate the average bank pays you to keep your money in savings there.

The convenient location isn’t of much value anymore, either. Banking apps now let you scan checks and deposit them from the comfort of your couch. And the utility of cash is decreasing by the day, so ATMs are queued up to join the Blockbuster club.

Anecdotal: The minor league ballpark nearest our office no longer accepts cash for tickets or some concessions.

Empirical: 59% of Americans with household incomes over $100k never use cash for purchases, up from 36% in 2015.

So it’s time to reconsider why you’re still keeping your money in a traditional, low-yield bank account.

But first, don’t forget to take our poll. Click or tap here and tell us what you want to read about in the next issues of The 101 and The Big Idea.

People Don’t Like Change, Even If It Benefits Them

When people don’t understand change, they resist it. It’s human nature. According to Harvard Professor Rosabeth Moss Kanter, who also serves as director and chair of the university’s Advanced Leadership Initiative:

“We are creatures of habit. Routines become automatic, but change jolts us into consciousness, sometimes in uncomfortable ways.”

So if you are a creature of habit who loves your routines, congratulations! Unlimited smiles and lollipops for you.

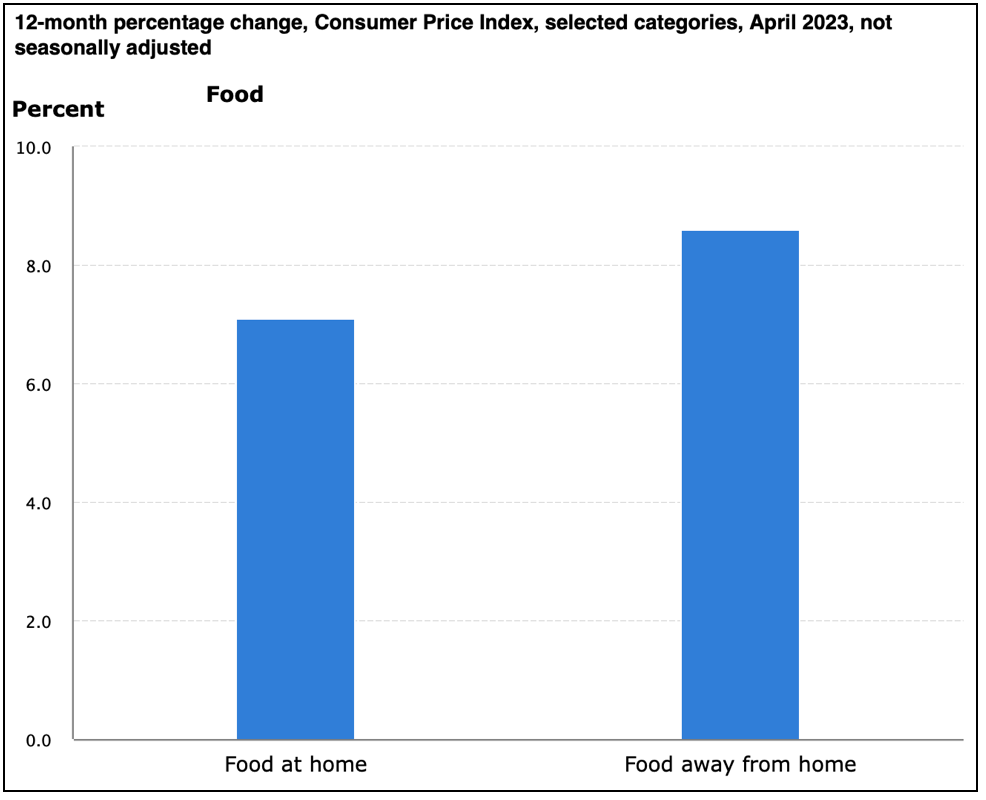

But if you’re not OK with your savings gaining a measly 0.24% while food inflation increases your monthly grocery bill by 7.1%, perhaps it’s time to be proactive and embrace some change.

The cost of food at home has risen 7.1% over the past year,

while food away from home has risen 8.6%.

Earn Higher Yields Without the Risks of Investing

High-yield savings accounts are just that: deposit accounts offered by financial institutions that earn above-average yields.

These banks are often online-only, and for good reason. They provide greater returns to customers because they don’t have to pay for operating branch locations and are able to pass those savings along to account holders in the form of higher interest rates.

And yes, in case you’re concerned about the safety of your money — which is understandable given the ongoing bank failures we’re witnessing — these institutions are FDIC-insured, meaning your deposits are protected up to $250k for individuals or $500k for joint accounts for spouses.

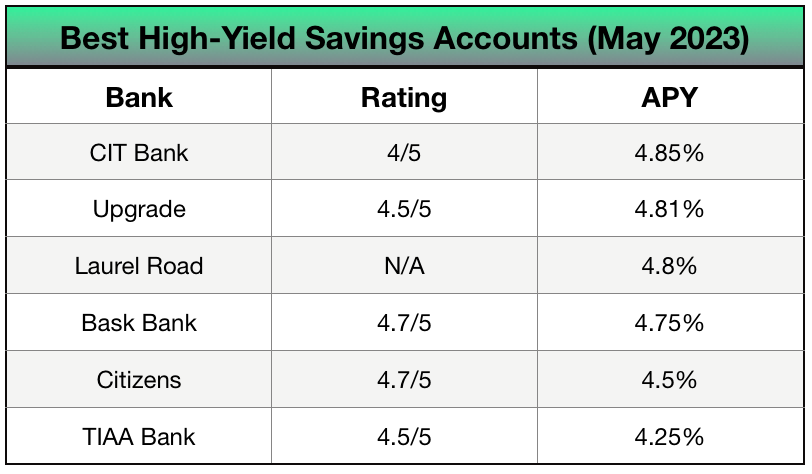

Right now, some of these banks are providing an APY of nearly 5%. Or, put another way, around 4.76% more than your local brick-and-mortar lollipop dispenser.

Nerdwallet keeps an updated list of them, as does Bankrate. But for a quick overview, here are some with the best ratings and highest APY:

Best high-yield savings accounts for May 2023.

Keep an eye on your inbox for next week’s issue of The 101. In the meantime, don’t forget to visit our archive and catch up on more personal finance and investing tips.

Until next time,

Team Rise & Hedge

One Response