An Under-the-Radar Oil Stock With Crazy Cash Flow

If you’ve been reading Rise & Hedge for a while, you know we like high-yield investments and strategies. Whether that entails writing about dividend snowballs, dividend ETFs, 5% CDs, REITs or Dividend Kings and Aristocrats …

We. Love. Yield.

Today’s recommendation — Chord Energy (CHRD) — fits the bill. The $7.53 billion energy company is our dividend stock of the month. But it’s not just the yield that caught our attention.

TL;DR

It’s earnings season again, which is a good time to rebalance your portfolios. We’re watching Chord Energy this month, a hydrocarbon exploration and extraction company with a strong dividend and eye-catching cash flow.

Some Background

If you recall from our issue, “Big Oil’s Big Comeback,” there are three phases of oil and gas production:

- Upstream: Exploration and retrieval of oil or natural gas, entailing geologic surveys, well drilling and the extraction of natural resources.

- Midstream: Transportation and storage of crude products, including pipelines, pumping stations, tanker trucks, rail transport and ocean shipping vessels.

- Downstream: Refining crude fossil fuels into finished products like gasoline, diesel, kerosene, jet fuel, heating oils, asphalt, rubbers, fertilizers, preservatives, plastics and pharmaceuticals (yes, 99% of medicines contain petrochemicals).

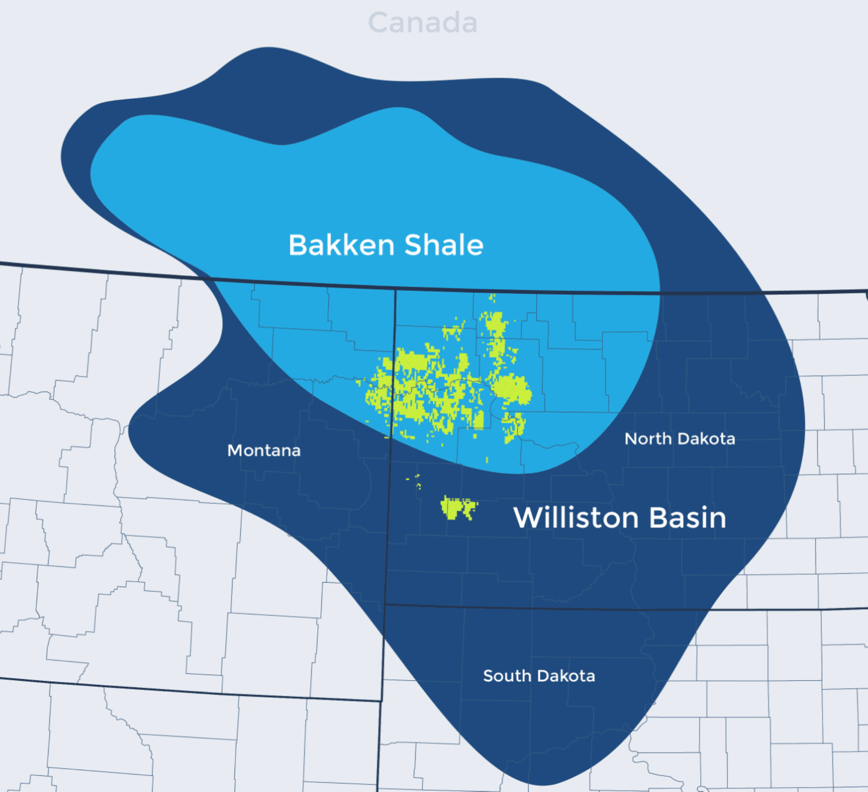

Chord Energy is an upstream, mid-cap company that specializes in hydrocarbon exploration and hydraulic fracturing (i.e., fracking). Founded in 2007, Chord went public in 2010, raised $400 million and is now one of the top producers in the Williston Basin, home to 4.3 billion barrels of oil and 4.9 trillion cubic feet of gas.

According to its website, the company “acquires, exploits, develops, and explores for crude oil, natural gas, and natural gas liquids” that are sold to a diverse network of refiners.

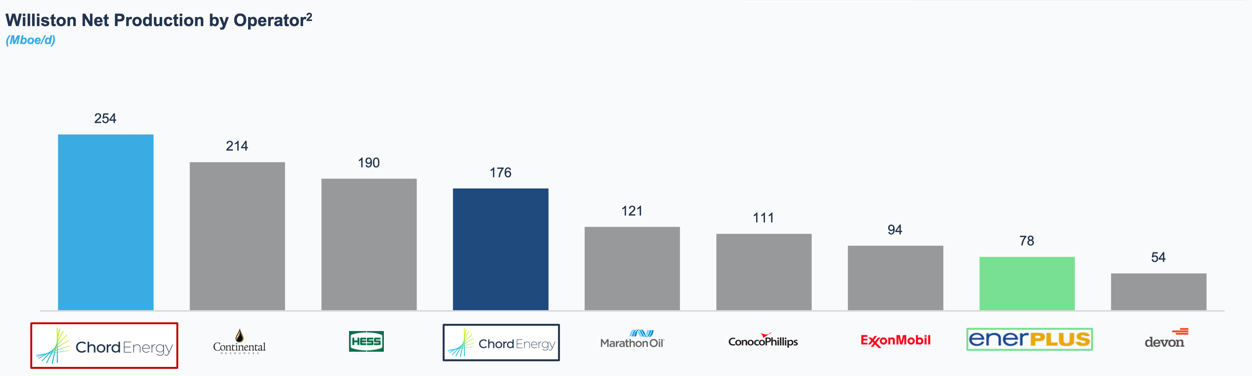

And while Chord may not be a household name, it’s the premier producer in the Williston Basin, extracting more crude in that area than operators like Hess, ConocoPhillips and ExxonMobil:

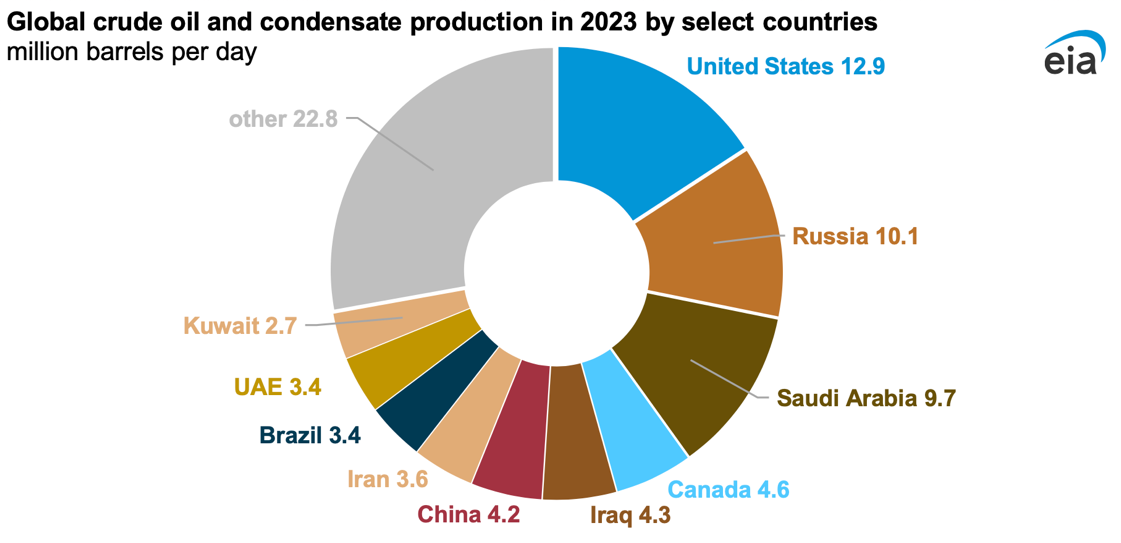

With the U.S. positioned to maintain its rank as the world’s largest oil producer — a title it’s held since 2018 — domestic producers like CHRD are poised to profit.

Strong Fundamentals

While we love yield, we really love strong fundamentals. Chord Energy saw its total assets grow from $2.1 billion in 2020 to $6.9 billion in 2023 … a 228% increase. Meanwhile, it lowered its total liabilities from $1.9 billion in 2022 to $1.8 billion in 2023.

Its revenue has also been steadily climbing:

- 2020: $1.08 billion

- 2021: $1.57 billion

- 2022: $3.64 billion

- 2023: $3.89 billion

The result? Since 2021, CHRD’s gross profit surged from $670.08 million to $1.43 billion in 2023, good for a 113% increase. The story’s the same for net profit, which rose from $188.96 million in 2021 to $1.02 billion in 2023 … a 439% gain.

Explosive Cash Flow Growth

Profit aside, cash flow is often more indicative of a company’s financial wellbeing. While income statements can be manipulated through financing, depreciation and amortization, cash flow statements are straightforward and report the company’s cash on hand.

And Chord Energy is a cash flow king. Its net operating cash flow since 2019:

- 2019: $892.85 million

- 2020: $290.93 million

- 2021: $914.14 million

- 2022: $1.92 billion

- 2023: $1.82 billion

Another reason cash flow is important? It’s where dividends come from.

Institutional Investors LOVE This Stock

On average, institutional investors (e.g., hedge funds, mutual funds, endowments, etc.) hold 60% of any given stock’s outstanding shares.

With Chord Energy, institutional investors own 98% of shares. The largest holder is Blackrock (5.17 million shares worth $932 million) followed by Vanguard (4.34 million shares valued at $799 million).

That combined with strong cash flow and revenue growth have likely contributed to Wall Street Journal analysts giving the stock a one-year median price target of $207.50 and a high-end one-year price target of $224. Shares are currently trading for $181, meaning there’s upside potential of 23.75% over the next 12 months.

Growth + Yield = 🤤

CHRD’s forward dividend yield is 2.72%, which equates to $1.23/share quarterly. And while 2.72% might not make headlines, the stock’s enjoyed strong growth that’s helped increase quarterly distributions.

So far this year, shares are up 7.64%. Over the past year, they’re up 25.76%. Going back five years, investors have seen a 484.26% return.

Its current price-to-earnings (P/E) ratio is 7.70. The average S&P 500 P/E ratio is 25 … meaning CHRD is considered cheap as investors are spending less money for each dollar of earnings the stock generates.