Domestic Production Just Hit an All-Time High

These days, you can’t drive anywhere without passing a Tesla. You can’t read financial news without seeing a headline about improved electric vehicle (EV) ranges. And you can’t visit a museum without a Just Stop Oil activist ruining a masterwork with orange paint.

In the not-so-distant future, EVs will be the norm rather than the exception. That’s a good thing because climate change is settled science and anyone claiming otherwise is scientifically illiterate.

Hell, general literacy in this country is abysmal. 54% of American adults are incapable of reading at a sixth-grade level. So like how banning books and defunding libraries is the go-to solution to solving American illiteracy, it appears the go-to solution to climate change is pumping more oil.

But alas, here we are. When it comes to combustion engine vehicles, they — and the gas pumps they rely on — aren’t going anywhere any time soon.

In fact, last week, domestic oil production hit an all-time high of 13.2 billion barrels/day. By 2025, production’s expected to increase by an additional 1 million barrels/day … every day.

Do carbon-based fuels have acute ecological and climatic impacts? Of course. Is much of the world still reliant upon fossil fuels? Unfortunately. Should that demand be reflected in your portfolio? Absolutely.

ExxonMobil’s Big Signal

Two weeks ago, oil major ExxonMobil announced its $60 billion acquisition of Pioneer Natural Resources. The result? Exxon says its production in the Permian Basin — the highest producing oil field in the U.S. — would more than double to 1.3 million barrels/day.

Why’s this a big deal? It marks a new chapter for American energy. Before its bounceback began in 2021, the sector experienced a couple disastrous decades on the back of unprofitable fracking ventures and explosive capital expenditure growth.

By February 2021, daily production was down to 9.9 million barrels/day. The following month, the arrival of COVID-19 was the last straw.

What changed between then and now? U.S. oil companies drastically cut capex from $199.7 billion in 2014 to $106.6 billion in 2022. That, coupled with renewed demand and higher prices, has seen a revival in the space that’s well pronounced in the following four-year price chart:

The current price/barrel of West Texas Intermediate (WTI) crude — the American oil benchmark — is $88 and once again pushing towards $100. For perspective, when oil demand bottomed in April 2020, the price/barrel of WTI crude sunk to $15.

So yes, oil majors like ExxonMobil (XOM), Chevron (CVX) and ConocoPhillips (COP) look like strong buys. Shares of those three companies are up 4.62%, 3.77% and 4.21%, respectively, just in the past week.

However, beyond the Big Oil mainstays, dozens of lesser-known companies and exchange-traded funds (ETFs) in the energy sector offer more affordable shares with similar upside potential.

But before we get to them, you should understand the three phases of oil and natural gas production.

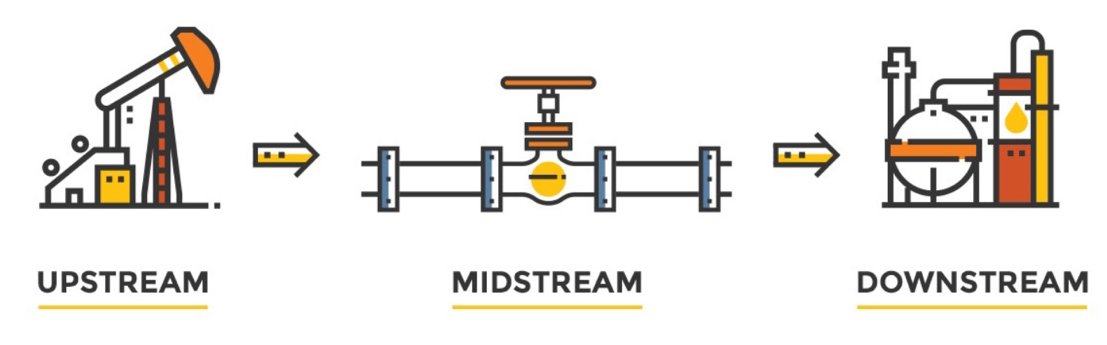

Upstream vs. Midstream vs. Downstream

Oil and natural gas production are divided into three subsets: upstream, midstream and downstream. If you’ve researched energy stocks or the energy sector broadly, you may be familiar with them. Even if you are, here’s a refresher.

Upstream: Refers to anything dealing with the exploration and retrieval of oil or natural gas. This entails geologic surveys, the actual oil well drilling process and the extraction of the natural resource.

Midstream: This segment involves the transportation and storage of crude oil and natural gas from production sites. This can include vast infrastructure, like pipelines, pumping stations, tanker trucks, rail transport and ocean shipping vessels.

Downstream: The final phase of the process involves turning crude fossil fuels into finished products like gasoline, diesel, kerosene, jet fuel, heating oils, asphalt, rubbers, fertilizers, preservatives, plastics and more.

Recapping, upstream is about extraction. Midstream is transportation and storage. And downstream is refining and finishing.

As we aim to do in most issues, we want you to be able to take this knowledge and apply it to investment opportunities. So, here are three companies aligned with each of those energy production segments that are worthy of your consideration.

Upstream: Schlumberger (SLB)

Schlumberger is the world’s largest offshore drilling company and the world’s largest offshore drilling contractor by revenue. It was founded in 1926 and is the 349th largest company in the world.

The $86-billion market cap company is growing, too. In February, it acquired Gyrodata, a gyroscopic wellbore positioning and survey technology company.

The acquisition only strengthens demand for SLB’s products and services, which has steadily grown in the recent past, resulting in its stock seeing year-to-date and one-year gains of 18% and 40%, respectively.

SLB pays a 1.65% annual dividend yield, or 25 cents/quarter. It’s currently trading at a solid 22.17 price-to-earnings ratio, and in Q2, the company beat year-over-year earnings by 14.33% with $8.1 billion.

SLB reports Q3 earnings on Oct. 20, and according to Zacks Investment Research, the expectation is for a 22% YoY beat on earnings per share. The Wall Street Journal gives SLB a one-year price target of $69.34. With shares currently trading at $60.38, the average analyst projection represents 14.8% upside potential.

Midstream: Flex LNG (FLNG)

Flex LNG is a seaborne liquified natural gas (LNG) shipping company. It recently expanded its Oslo, Norway-based fleet, bringing its total LNG carriers to 13 with an average age of 3.5 years.

Here’s why we love the company: The entire Flex LNG fleet is fully booked until 2030. Its main clients include BP, Cheniere Energy, Chevron, Trafigura and Guvnor.

Shares pulled back slightly this year but are still up 1.79% YTD after seeing an astounding 668% gain since its pandemic-induced bottom in March 2020. FLNG is currently trading at a ridiculously cheap 11.38 P/E ratio.

Then there’s the dividend, which yields an enormous 9.59%, or $3/share annually. Additionally, FLNG’s expected to post earnings of 75 cents/share for the current quarter, good for a YoY increase of 23%.

European natural gas futures recently surged over 5% to €51/megawatt-hour, after being as low as €21 in June. Given that … and how FLNG’s fleet is entirely booked for the next six years … and its massive dividend, shareholders will continue to be rewarded every quarter for the foreseeable future.

Downstream: VanEck Oil Refiners ETF (CRAK)

This ETF holds a basket of oil refiners, including Marathon Petroleum, Phillips 66 and Valero Energy. Its expense ratio is a bit elevated at 0.76%, but it’s offset by a dividend yielding 2.9%, or 96 cents/share annually.

CRAK has an absurdly low P/E ratio of 4.56. So far this year, it’s gained ~12% and is up 127% since the pandemic-induced bottom in March 2020.

The ETF, which has $30.5 million in net assets, seeks to mirror the MVIS Global Oil Refiners Index, which tracks the overall performance of companies involved in crude oil refining.

In late September, Russia announced it’ll be restricting exports of gasoline and diesel in an effort to stabilize domestic prices. That news sent the price of diesel up by 5%. The country, which is a major exporter of the fuel, shipped 30 million barrels of diesel in August. In September, that figure fell to 90k gallons, a 99.7% reduction.

Russia’s export restrictions are putting upward pressure on prices for refined oil products and diesel in particular, tightening a market that was already dealing with undersupply and likely aiding companies and ETFs with downstream operations.

As a result, the three aforementioned companies in CRAK’s holdings — Marathon, Phillips 6 and Valero — all saw their shares recently hit all-time highs. The ETF itself is currently $1.10 off its all-time high of $35.05/share and is likely to challenge that price in the near future.

TL;DR

No matter how you feel about fossil fuels, the demand for them isn’t subsiding in the immediate future. As part of a well-diversified portfolio, it’d behoove you to include some exposure to the energy sector, whether that’s with an oil major, a lesser-known company operating in one of the three production phases or with an ETF leveraged to the industry. As always, conduct your own due diligence before deciding which investment is right for you.