64% of Americans live paycheck to paycheck.

Raise your hand if you’ve ever been told by someone with gray hair, a pension and a home they purchased decades ago for less than what a car costs today that “young people are entitled and expect everything to be handed to them.”

Raise your hand again if you’ve heard someone say, “living with your parents means you’re not working hard enough.”

We’re guessing there are a lot of hands up.

Nobody’s surprised by how out of touch older generations can be with younger people’s financial struggles.

It’s become boomers’ mating call. But rather than being used for breeding, it’s aimed at attracting like-minded seniors who enjoy pickleball, all-inclusive cruises and ridiculing the youth.

They’re not to blame, though. They come from a time when single-income households could thrive on a factory worker’s salary. When you could have 2.5 children, own a vehicle, a three-bedroom home and take biannual vacations … and still have enough left over each week to save.

Sure, they endured their hardships. The 1973 oil embargo and subsequent recession, for example. The kind economists say is “once in a lifetime.”

Well, if you were born after 1980, you’ve already experienced three “once-in-a-lifetime” financial crises. Another’s likely on its way.

But what is surprising is how they can see the data and still expect entire younger generations to succeed merely by picking themselves up by the bootstraps and having a hard-working mentality.

How We Got Here

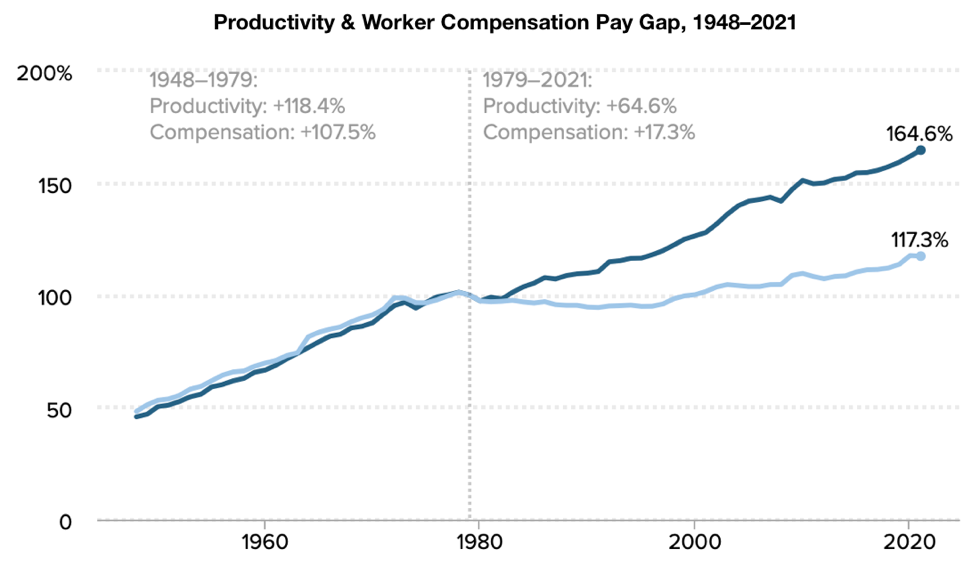

For most of modern American history, wages paralleled worker productivity.

Around 1973, that changed. Some politicians in suits got together with wealthy campaign donors in suits and decided — for all of us — that’s no longer the case.

- Pensions began disappearing and 401(k) plans shifted the onus of saving for retirement from employers to employees.

- Millionaires and billionaires were set on a path that now sees them paying a lower tax rate than the bottom 50% of Americans.

- And as productivity continued its ascent, inflation-adjusted wages virtually stagnated.

In 1978, minimum wage was $2.65. Adjusted for inflation, that equates to $11.89 today. However, in 2023, the federal minimum wage is just $7.25.

But median rent in the U.S. is ~$2,000/month. That means anyone making minimum wage (before taxes are deducted) must work at least 69 hours/week to cover rent. That’s before factoring in other cost-of-living expenses like food, medicine, transportation and healthcare.

It’s no coincidence this has paralleled the emergence of the gig economy. One job isn’t enough? Have you tried a side hustle? How about two? Maybe three.

Unforeseen emergency? Humans have two kidneys. You can always sell one.

Given how many hours it takes to simply cover life’s bare necessities, and how an astounding 64% of Americans are now living paycheck to paycheck, it’s no wonder why younger people are hesitant to invest their money.

This country has an incredible deficit of personal finance education. Many don’t know where to turn to safely grow what they’ve worked so hard to earn. Others, who may be settling into good careers with decent pay, have no risk tolerance because they fear potential losses.

But there are numerous ways to safely grow your money outside of the stock market. Before we get to that, you need a plan that helps you save even the smallest amounts, which over time can grow into sizable account balances.

Dollar-Cost Averaging

Dollar-cost averaging (DCA) is a disciplined habit. If you stick to it, it helps you steadily grow your wealth over time.

In short, it is the practice of dedicating a fixed amount at regular intervals (e.g., each pay day) to either save or invest.

Though it’s commonly associated with stocks and retirement accounts, DCA can be used to fund the recurring purchase of bonds or deposits into accounts that produce higher yields than you’d receive just by letting your money sit in traditional savings accounts.

By leaving your money in a savings account with an insultingly low interest rate, you’re actually losing money due to inflation.

Using DCA to commit a dedicated amount to a higher-yielding account or low-risk asset on a repeated basis allows you to not only combat inflation’s effect on your principle, but steadily — and safely — build your wealth over time.

So if you’re adverse to the idea of stock market volatility, what options do you have that can produce solid returns without the risk?

In the next issue of The Big Idea, we’ll share a few ideas for safely growing your hard-earned money outside of the stock market in low-to-no-risk bonds, money market accounts and high-yield savings accounts.

TL;DR

The gap between pay and productivity is widening. Inflation’s eroding the dollar’s value. Today, you have to do more with less.

There are low-to-no risk ways to grow your wealth steadily and conservatively outside of the stock market. Keep your eye on your inbox later this month for actionable ideas on how to do that.