Plus the Grifter-in-Chief’s Newest Side Hustle

TL;DR

A higher-for-longer rate environment sucks if you’re buying a house or shopping for a new car. But it’s good news for savers whose money is otherwise withering away in brick-and-mortar banks that offer insulting APYs.

With the Federal Reserve’s January meeting in the rearview mirror, one thing is now abundantly clear: Concerns about the impact of Trump’s tariffs on inflation weren’t hyperbolic.

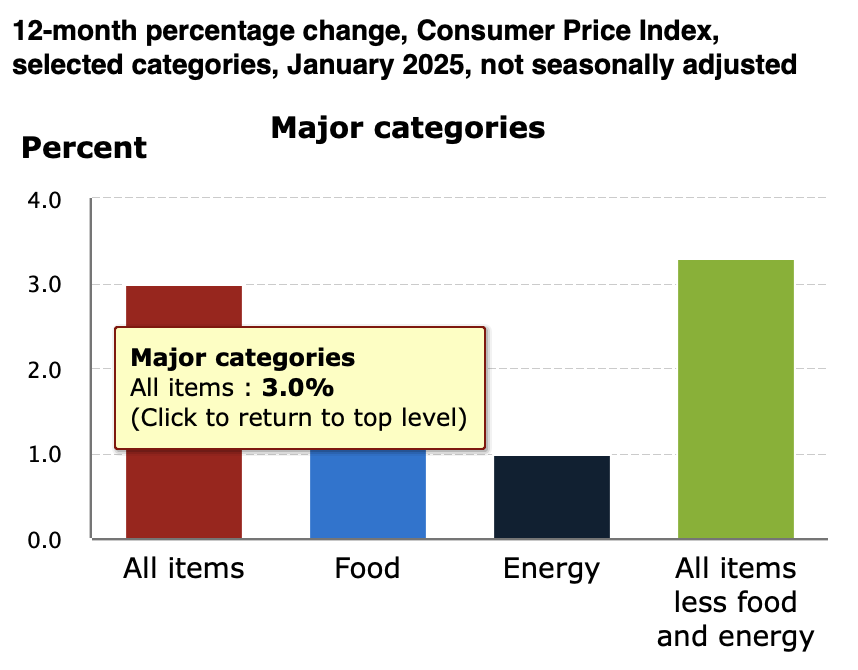

In January, inflation — as measured by the Consumer Price Index (CPI) — hit 3% year-over-year for the first time since June. When stripping out volatile energy and food prices, it crept up even higher to 3.3%.

We acknowledge that Trump only took office on Jan. 20. But he’s made a habit of taking credit for events that predated his inauguration, like the ceasefire between Israel and Hamas and the price of Bitcoin surpassing $100k for the first time ever.

Nonetheless, the often self-congratulatory president is back to pointing the finger of blame at Biden for inflation. The Fed, on the other hand, couldn’t be more clear about why (and who) they’re concerned with.

After last month’s meeting, the central bank announced that it’s pausing its interest rate cuts citing how Trump’s policies could reignite inflation and put pressure on the economy.

In its meeting minutes, the Fed reaffirmed that it wants to see the CPI at 2% — a full percentage point lower than it currently stands — and that “the Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.”

Translated: Not only are rate cuts on pause, but if inflation worsens (as many economists expect), rate increases are on the table. And while this may be devastating news for Americans hoping to purchase their first home or finance a new car, it’s welcome news for savers.

Your Bank (Still) Sucks

We’ve written a couple times in the past two years about why your bank sucks. So we’re not going to get into the weeds about why you should forgo brick-and-mortar institutions’ lollipops and ATMs in favor of exceptionally higher rates at online banks.

But we’re going to give you some quick perspective. While high-yield savings accounts are no longer offering +5% APYs, they’re still offering incredible value over traditional banks … and will continue to as long as the Fed keeps rates elevated.

Today, the national average APY for a savings account is 0.41%. For context:

- Jenius Bank and Lending Club are offering APYs of 4.50%.

- Brio Direct is offering an APY of 4.55%.

- Openbank is offering an APY of 4.75%.

- And Axos is offering an APY of 4.86%.

We don’t receive a penny from those aforementioned banks. Those aren’t affiliate links. We’re here to help you improve your financial standing. Period.

And with higher-for-longer interest rates likely to be an ongoing theme in 2025, getting your funds out of the corner bank and into a high-yield savings account is the easiest and safest way to let your money work for you.

The President’s Latest Grift

While perusing Trump Media & Technology Group’s filings last week to determine how much money his lackeys lost by investing in his company last quarter, we stumbled upon something very interesting.

From $500 sneakers and branded bibles (just like Jesus intended) to meme coins and cologne that we imagine smells like this, Trump’s latest grift was disclosed in a Form 8-K filing made with the SEC announcing the trademark registration for three ETFs:

- Truth.Fi Made in America ETF

- Truth.Fi Energy Independence ETF

- Truth.Fi Bitcoin Plus ETF

No word yet on which companies the Made in America ETF will hold, but we suspect none will feature his products since his ties, golf hats and eyeglasses are made in China; his suits are made in Indonesia; his mugs are made in Thailand; his fleeces are made in Pakistan; and his pullovers are made in Vietnam.

But we’re still holding out hope that he’ll create a line of adult diapers that not only can he use … but are manufactured right here in the good ole U.S.A.

Stock Update

The equities we recommended in 2024 did pretty well. Really well, actually. In some instances, they posted gains in the triple digits.

But we don’t make them without doing extensive research. So far this year, we’ve made two (both in January) and we’ll have another for your next week. But a quick update on the first stock we recommended in 2025.

When that issue hit your inboxes on Jan. 8, we explained why DraftKings was a “Buy” for investors looking for high upside growth potential. We broke down the industry’s explosive growth, the fundamentals (particularly how its revenue growth is trending in the right direction) and provided some technical analysis that we found encouraging.

Typically, we tend to favor value stocks, especially dividend-paying ones that are in reliable sectors. But DraftKings hasn’t disappointed. When the company reported Q4 2024 earnings last Thursday, Wall Street was enamored with:

- 30% year-over-year annual revenue growth

- 13% year-over-year quarterly revenue growth

- 42% growth in the customers, including 3.5 million new users

As a result, analysts have issued a “Strong Buy” rating. The stock is now up 32.34% since our recommendation early last month.

We’ll have another pick for you next week that we’re equally optimistic about.