Sportsbook Apps Are Taking Over

TL;DR

Legalized sports betting is now worth more than some countries’ economies. The explosive growth it’s experiencing presents a buy-low opportunity for investors looking to capitalize on others’ vices.

Once upon a time, if you wanted to bet on sports, you had to visit a casino, a horse track or call your bookie. But in 2025, like many other modern conveniences, Americans can now place six-leg parlays from the comfort of their couches thanks to smartphones.

The result: 60% of American adults say they’ve gambled in the past year. And there are thousands of fewer broken knee caps, because with sportsbook apps, you pay upfront.

We wrote about America’s gambling addiction (and how to invest in it) in 2024. And while we stuck to traditional gaming establishments then, the explosive growth of online sports betting makes the topic worthy of revisiting.

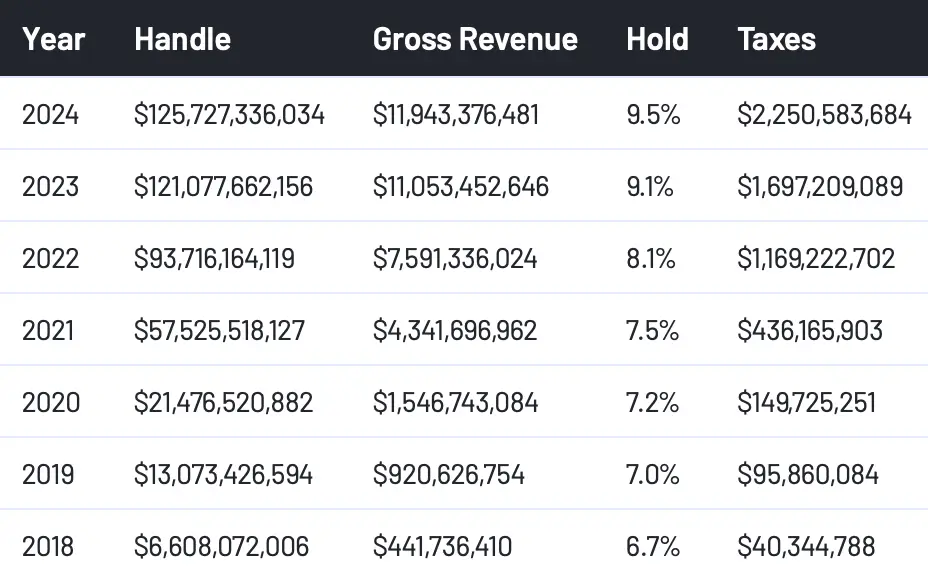

That’s because as more states permit legalized gambling, sports betting has become an enormous business. Americans placed over $120 billion in online sports bets each of the past two years, according to Sportsbook Review:

Last year’s $125.727 billion figure is just shy of the GDP of Ethiopia and $10 billion more than the GDPs of Slovakia and Ecuador … meaning Americans are now betting more on sports each year than the total value of some of the developing world’s economies.

More strikingly, that amount of online sports bets last year represents an astounding 1,804.95% increase since 2018.

Unfortunately, it’s coming at a cost to everyday Americans. A 2024 study found that in households that increase their bets by $1,100/year, there is a corresponding decrease of 14% in traditional investments.

With sports books now legal in 38 states and Washington, D.C., their growth isn’t only resulting in decreased investments but also:

- Lower credit scores

- Higher credit card debt

- And higher rates of account overdrafts

But American degeneracy aside, for every vice, there’s a corresponding investment opportunity. Marlboro-owner Altria Group (MO), for example, has appreciated 272% over the past 20 years while becoming a darling for dividend investors with its 7.89% quarterly yield.

Today’s pick isn’t income-oriented, though. Nonetheless, it should be alluring to growth investors looking for a buy-low opportunity to start the year.

Why DraftKings Is a Buy

Founded in 2012 as a daily fantasy sports site, Boston-based DraftKings (DKNG) has evolved to become the fourth-largest online sportsbook with a market cap of $33.40 billion.

When the company holds its Q4 2024 earnings call on Feb. 12, 2025, it’s expected to build on the momentum established in Q3 when it posted a 39% year-over-year increase in revenue while simultaneously lowering its customer acquisition costs by nearly 20%.

And while DraftKings is still operating at a loss, it’s increased its net assets by 10.62% since 2023 while holding its liabilities steady. Additionally, the company’s free cash flow has climbed from -$73.42 million in March 2024 to $130.88 million in September 2024. Those aren’t the types of numbers companies like Walmart (WMT) are putting up, but there’s reason to be optimistic about the near term.

First, revenue growth is trending in the right direction:

- 2019: $323.41 million

- 2020: $614.53 million

- 2021: $1.30 billion

- 2022: $2.24 billion

- 2023: $3.67 billion

- 2024: $4.61 billion

And despite earnings per share (EPS) being in the red, that too is trending in the right direction. In 2021, annualized EPS was -$3.78. In 2022, -$3.16. In 2023, EPS was -$1.73 and last year, -$0.85. As a result, the company posted positive free cash flow for the first time in 2024.

And while shares of DKNG gained 13% over the past year — respectable, but not as much as the S&P 500’s 24% gain in 2024 — a little technical analysis indicates underlying strength.

What the Chart Says

The stock is both undervalued and oversold while remaining down 47% from its all-time high set in March 2021. Looking at DraftKings’ one-year technical chart offers more clues:

The first important part is the blue arrow at the top. That’s pointing at the intersection of the 50-day moving average and the 200-day moving average.

Moving averages calculate the average closing price of an equity over a given period. When the shorter term average crosses over the longer-term average, it’s referred to as a golden cross pattern — an extremely bullish indicator.

For DraftKings, the golden cross pattern emerged in late December amid a pullback. And that pullback brings us to the second blue arrow at the bottom of the chart, which is pointing at DKNG’s Relative Strength Index (RSI). The RSI is a momentum indicator that generally plots points between 70 and 30. At the upper-end of the scale, equities are considered overbought and likely to face a bearish price reversal.

That’s exactly what happened when DraftKings breached an RSI of 70 in December. But to start the new year, the RSI bounced off of 30, where it was considered oversold, indicating a likely bullish price reversal in the near future, and is already trending upwards.

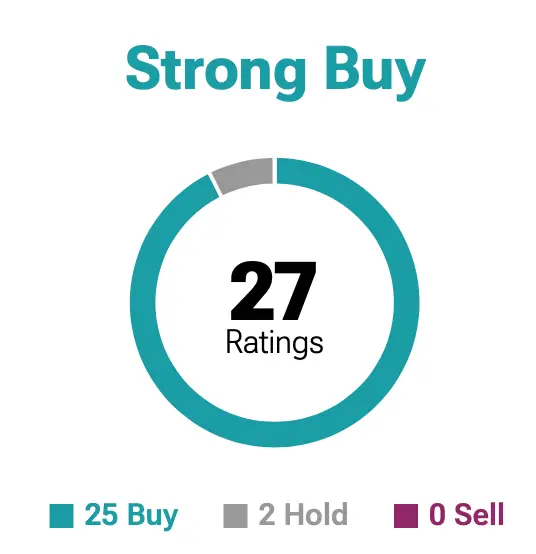

What Analysts Are Saying

Based on 27 analysts’ ratings, DraftKings is currently considered a “Strong Buy,” according to TipRanks, with zero analysts recommending it as a “Sell.”

The Wall Street Journal’s analysts have given DKNG a median one-year price target of $53. With shares currently trading for $37.77, that median price target represents upside potential of over 40% by the end of 2025.

If you’re looking to add an undervalued growth stock to your portfolio to start the year, you could do worse than DKNG. But don’t listen to us … listen to DraftKings’ 3.5 million reprobates (sorry, active users) who are handing over their hard-earned money to the online sportsbook on a recurring basis while neglecting their investment portfolios.