Avoiding Bad Investments Is as Important as Finding Good Ones

TL;DR

With the bull market likely to pump the brakes this year, it’s increasingly important to understand what makes an investment flawed. We’ve identified three telltale signs that you may want to avoid in a stock, ETF or broad sector this year.

According to Goldman Sachs’ investment strategy team, the current bull market has left the S&P 500 “more expensive than at least 90% of the time since World War II.” That means, going back 86 years, the stocks of the 500 largest companies listed on American exchanges are presently more costly than they were in 77 of those years.

Inasmuch, the investment bank has tempered its 2025 outlook for the market, forecasting a 5% to 7% gain by year’s end. For comparison, three of the past four years have seen the index gain at least 24%, with 2022’s bear market loss of -19% being the only down year for the S&P 500 over the past four.

Making matters worse, bond rates are on the rise. The 20-year yield is now over 5% with the 10-year not far behind. That, coupled with the expectation of fewer (if any) interest rate cuts from the Fed this year, puts us firmly back into a higher-for-longer rate environment.

So, as we’re apt to do here at Rise & Hedge, lemons and lemonade. We often recommend fundamentally strong companies worthy of your investments, explain how you can pace the market using some ETFs that charge lower expense ratios than the largest funds and show you how to use strategies that can set you up for steady income later in life.

Today, we’re going to lean into what you shouldn’t invest your hard-earned money in this year. Because according to Goldman Sachs, about 60% of the S&P 500’s return last year came from price-to-earning (P/E) expansion, NOT from earnings growth.

Here’s the critically important difference: P/E expansion indicates when investors are willing to pay more for a company’s earnings, while earnings growth indicates when companies are actually making more money. So what we’re left with is an overvalued market. The average P/E ratio for the S&P 500 is generally between 20 and 25. Today, it’s 27.87. Looking at individual companies’ P/E ratios, it’s even more concerning.

1. Concerning P/E Ratios

Take Walmart (WMT), for example, which might be the best-case-scenario of the companies we highlight today. The consumer staples mainstay had an exceptional year in 2024, gaining over 74% as it continued building out its Walmart+ business segment.

In fact, Walmart had the most revenue of any company in 2024, generating $648.125 billion — even more than overlord Jeff Bezos’ Amazon.com (AMZN) did (though, for the record, the yacht collector’s company did rank second with $574.785 billion).

But from an earnings perspective, Walmart had a mixed year, seeing growth in Q1 followed by declines in Q2 and Q3 before ticking back up in Q4. It currently boasts a P/E ratio of 38.16.

Does that mean Walmart doesn’t warrant a place in your portfolio? Of course not. It’s the largest grocery store in America, and it’s a Dividend King, having raised its payout for 51 consecutive years since first issuing a dividend in 1974. Shareholders just shouldn’t expect the same kind of returns the retail and emerging e-commerce giant posted in 2024, and as things stand, it’s not currently at an attractive valuation.

Tech is more of a pressing concern. The sector could post strong gains in 2025, but tech has been cited by analysts as a prime candidate for a correction. And given the weighting of the Magnificent Seven, that could result in a major drag on the broad market. Look no further than Tesla (TSLA) and its current (and ridiculous) P/E ratio of 110.56.

It’s easy not being a fan of Elon Musk. His own social network’s AI has pinned him as one of the foremost propagators of online misinformation, his children despise him and he takes credit for groundbreaking companies that were founded long before he latched his name onto them.

But in this case, it has nothing to do with the pasty, bloated alien or his Freudian rocket-envy. Tesla’s a fundamentally flawed company that produces computers on wheels — not vehicles. It had negative free cash flow in Q1 last year and middling free cash flow, proportionately, thereafter. On a trailing 12-month basis, it’s posted -$19.56 billion in net income (a.k.a. profit).

Investors should still be able to find gains in both the consumer staples and tech sectors, as well as the other nine sectors of the S&P 500. But when you look more closely at the macro environment, there are warning signs that shouldn’t be ignored. Here are some other examples of popular companies with concerning P/E ratios heading into the new year:

- Sprouts Farmers Market (SFM): 40.08

- Coinbase (COIN): 42.95

- Chipotle (CMG): 52.59

- Nvidia (NVDA): 53.45

- Costco (COST): 55.02

- Eli Lilly (LLY): 86.49

- Fair Isaac (FICO): 93.78

- SoFi Technologies (SOFI): 121.19

- Shopify (SHOP): 124.12

- Toyota (TM): 124.73

- Estée Lauder (EL): 135.09

- Shopify (SHOP): 137.53

- Taiwan Semiconductor Manufacturing (TSM): 161.17

- Live Nation (LYV): 165.71

- Broadcom (AVGO): 185.00

- GameStop (GME): 185.08

- Arm Holdings (ARM): 229.33

- Cameco (CCJ): 262.22

2. Supply-Demand Imbalances

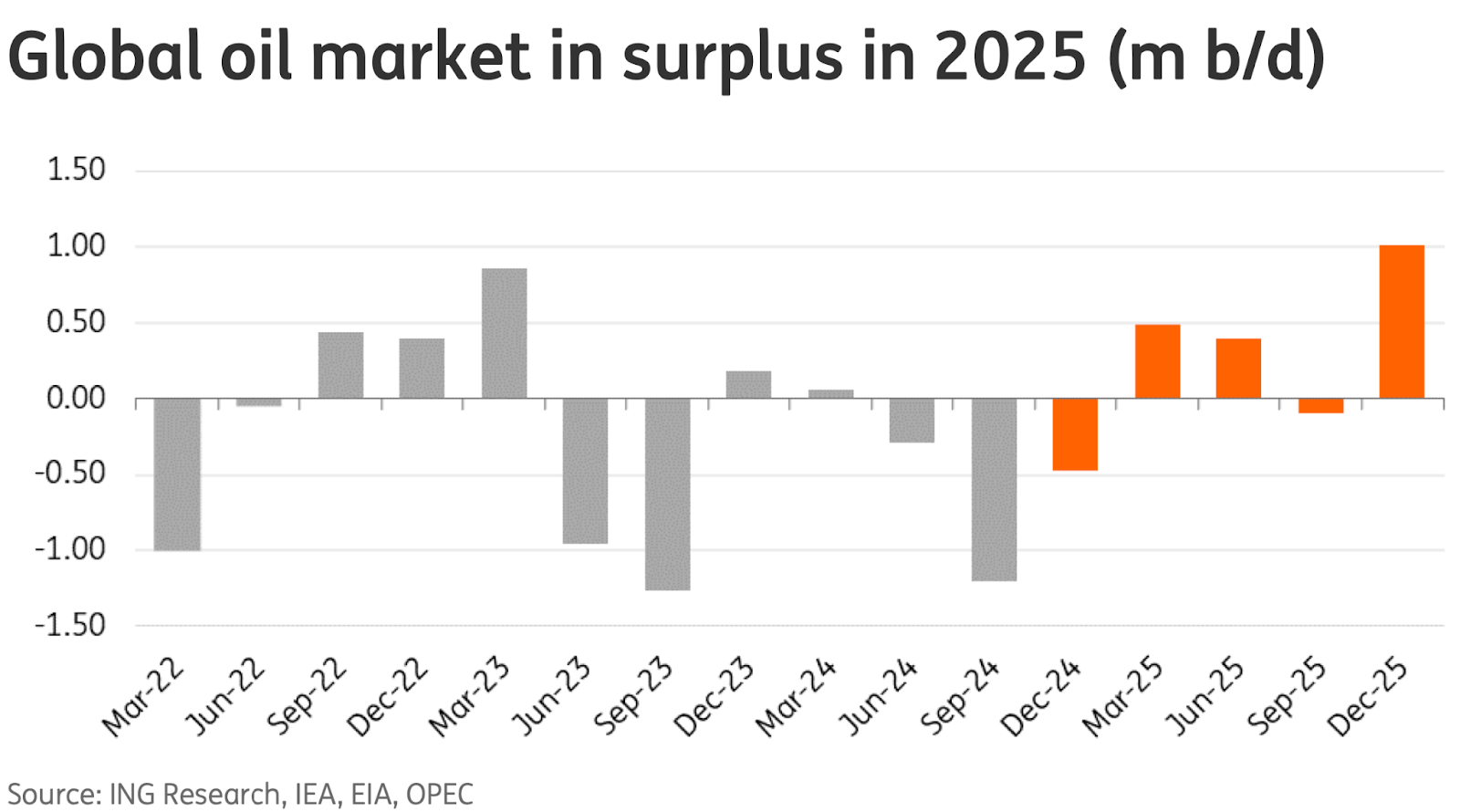

At the time of writing, oil just hit a four-month high. Big f*****g deal. It still remains down -32.07% from its five-year high of $116.02/barrel in May 2022. And while disparaging fossil fuels’ outlook may seem counterintuitive given the incoming administration’s mantra of “drill, baby, drill,” energy companies can’t really drill anymore than they are.

The U.S. already produces the most oil and natural gas in the world, ever. Not Russia. Not Saudi Arabia. And it’s gotten to the point that the industry is facing a massive surplus in both 2025 and 2026. That excess production has already decreased energy companies’ profit margins, and if they do concede to Trump and miraculously find a way to increase production, it’s going to further erode earnings and hurt shareholders.

Investors shouldn’t be giving these companies much leeway as it stands. Last year, owning oil majors’ stocks punished investors’ portfolios, with only two posting gains:

- ExxonMobil (XOM): +7.88%

- Shell (SHEL): +1.95%

- Chevron (CVS): -0.88%

- Valero (VLO): -8.02%

- Marathon Petroleum (MPC): -8.55%

- BP (BP): -15.43%

- ConocoPhillips (COP): -16.50%

- Phillips 66 (PSX): -16.75%

Returning to our first point about overvalued stocks, BP’s current P/E ratio is a mind-boggling 196.97. Buyer beware.

Financial services firm ING has stated that oil prices are “likely to remain under pressure,” and regardless of Trump’s tough talk on Iran, with “almost all Iranian [oil] exports heading to China, it may be challenging to significantly reduce these flows.”

In short: A global oil glut doesn’t bode well for energy stocks or their investors this year.

3. Over-Reliance on Imports

We’re not going to dive into the likely fallout from Trump’s tariffs. But briefly, he’s entertaining the idea of levying a tax upwards of 60% against all Chinese imports. Some companies will be able to pass through those costs to consumers — namely, those operating in the consumer staples sector. On the other hand, consumer discretionary companies are more affected by shifts in consumer behavior.

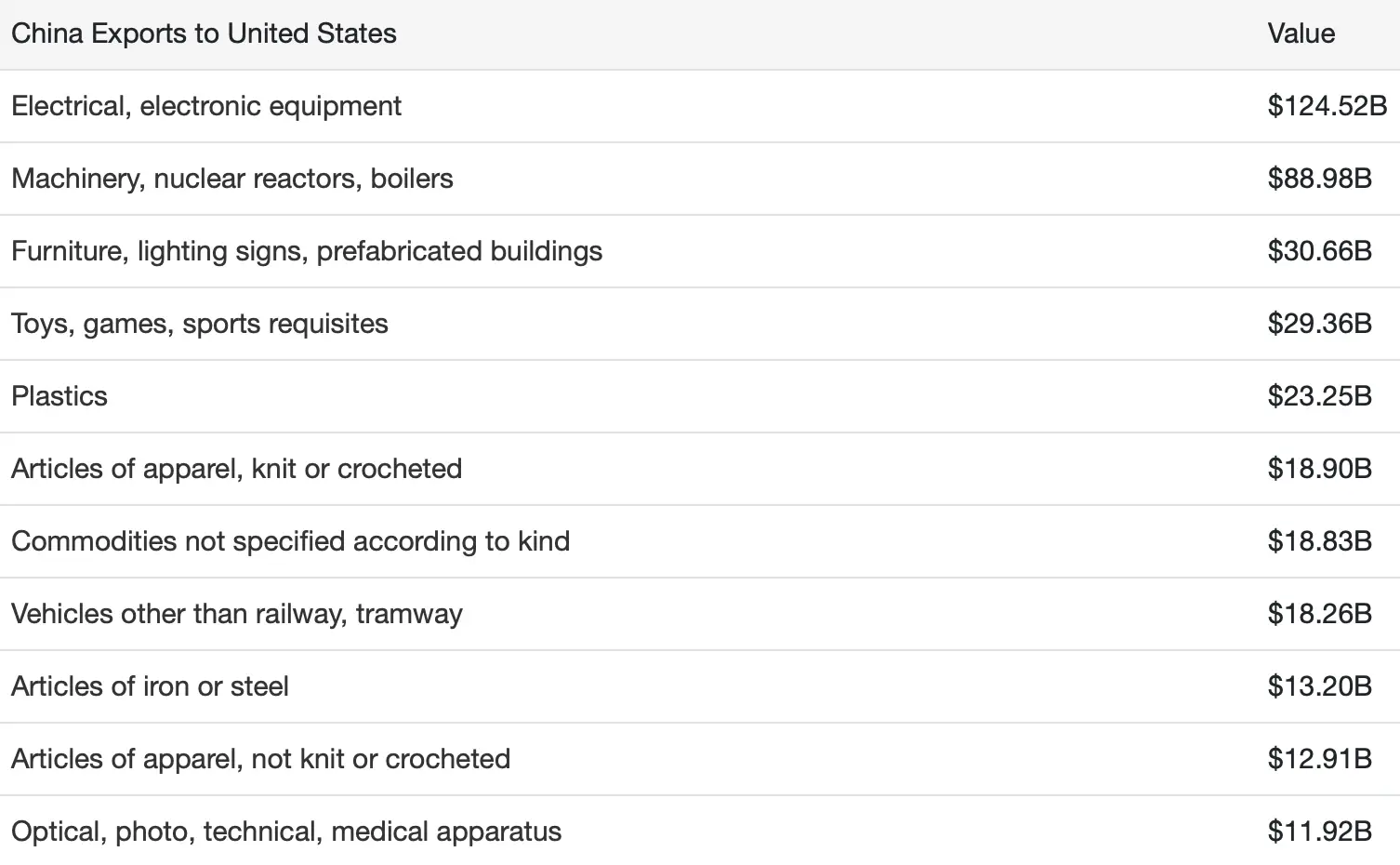

Lithium-ion batteries serve as the perfect example, of which China produces 80% of the global supply. The U.S. imports $13.1 billion worth of them each year from China, or 70% of all the lithium-ion batteries used in this country. Companies like Stanley Black & Decker (SWK) rely heavily on Chinese production of those batteries for use in their products.

The company, which is also a Dividend King and currently yields 4.05%, may seem like a buy-low candidate after falling -14.22% over the past year. In response to looming tariffs, SWK is planning on shifting its supply chain for those batteries from China to — wait for it — Mexico, another country in Trump’s crosshairs.

That’s not going to help an already-struggling company. SWK saw total revenue decrease from $3.95 billion in September 2023 to $3.75 billion in September 2024. Over the same period, it saw its free cash flow decrease by 45.24%. Falling free cash flow translates to less money to cover operational expenses and less money for shareholders.

While Stanley Black & Decker isn’t a bellwether for the broad consumer discretionary sector, it does serve as an example of the scrutiny that companies that are overly reliant on Chinese imports should receive from prospective investors. To better understand what’s at stake, here are the top 10 most-imported goods from China:

Nobody has a crystal ball. Despite what the data and trends suggest, any of the aforementioned companies could be exceptions to the rule in 2025. However, in a year that the investment banks are projecting lower returns, investors should be acutely aware of the fundamental flaws that certain companies and sectors present.