Despite Trump’s Rhetoric, Energy Stocks Could Struggle

TL;DR

Campaign promises have been broken for as long as politicians have been making them in stump speeches. Trump’s no exception, and investors should be mindful about their allocations to energy stocks.

Big promises make for big headlines. But oftentimes, what’s said on the campaign trail fails to be delivered in Washington. However, one expectation that’ll likely play out is that the president-elect will axe the EV tax credit, which will not only hurt car companies’ sales, but by extension, American consumers as well.

That’s in part why automakers are urging Trump not to end what he refers to as the “EV mandate.” By now, we all know that the former/next president isn’t exactly a wordsmith. But he’s smart enough to know that mislabeling a tax credit as a mandate will rile his base, which associates words like “mandate” with socialism and acronyms like “EV” with the diabolical progressive agenda of making the world’s climate more stable for future generations.

So when Trump makes unfounded and outlandish claims, like saying the noise from wind power causes cancer, to those who are well-informed or who received an education beyond middle school, it just comes off as hyperbolic bullsh*t that those who didn’t get past eighth grade seemingly believe.

Of course, back in reality, we should all know that energy isn’t partisan. Oil is a commodity, and commodities don’t lean left or right. The world continues to depend on it, and energy companies continue to produce it. However, that dependence is waning.

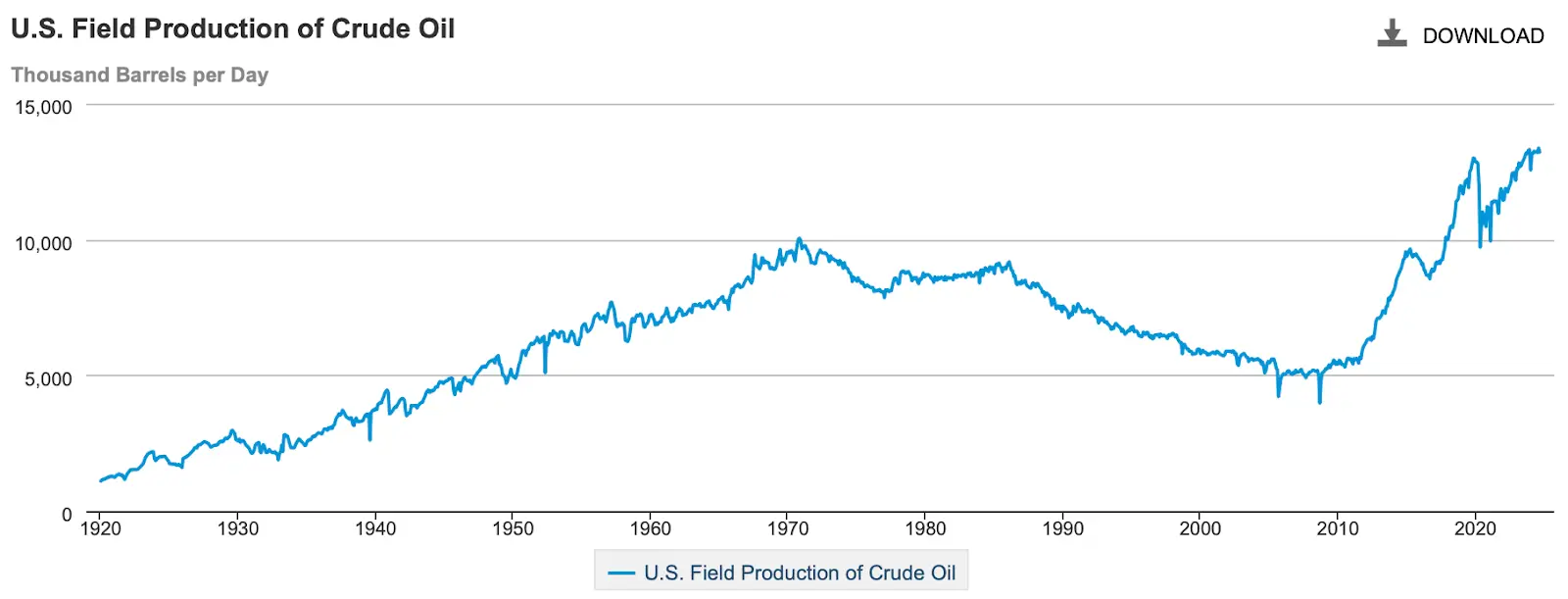

The Biden administration, recognizing that and also not subscribing to the school of climate denial, enacted the EV tax credit. But Biden’s term also coincided with domestic energy production reaching an all-time high, with the U.S. currently producing more oil and natural gas than any other country has in the history of the world:

Regardless of Trump’s messaging, the fact remains that U.S. energy companies are already pumping more oil than ever before … and they’re not sure how they’re going to be able to pump much more without it resulting in massive surpluses.

And it doesn’t take a Nobel Prize-winning economist to understand that when supply outpaces demand, it’s bad for business.

Energy Policy With a Side of Reality

A major facet of Trump’s platform has been the claim that he will establish American energy dominance. But with the U.S. already producing more gas and oil than Saudi Arabia and Russia, that’s like Steph Curry saying he’s going to become the greatest three-point shooter in NBA history.

Instead, investors should probably listen to the big boys in the room. Like ExxonMobil (XOM) CEO Darren Woods, who said in November that he doesn’t believe Trump can make good on his promise to “unleash” oil production.

He added, “I don’t think U.S. production is constrained, so I don’t know that there’s an opportunity to unleash a lot of production in the near term, because most operations in the U.S. are already optimizing their production today.”

Additionally, this month, the Financial Times reported that “producers are unlikely to follow the president’s marching orders, as muted global demand and Wall Street calls for higher returns depress outlooks for crude in the U.S. and abroad, warn analysts.”

Translation: Trump’s statements are in direct contradiction to the executives who intimately understand the macroeconomics of the energy industry.

The Financial Times, long considered a center-right publication, stated that “JPMorgan similarly forecasts an ‘outright bearish’ market for oil in 2025, with 1.3 million barrels a day of excess global supply,” going on to say that JPMorgan analysts’ outlook is for U.S. shale growth to “slow to a crawl in 2026.”

The Financial Times cited underwhelming demand from China and strong non-OPEC supply growth as the causes that are dragging down crude prices, resulting in a surplus and creating the lack of incentive to drill.

“You can’t have low crude prices, as President Trump has campaigned on, at the same time as robust production growth. It’s just not reality,” said Hunter Kornfeind, an oil analyst at Rapidan Energy Group.

Simply put, just saying things doesn’t make them true. If that was the case, the repeated rumors of Trump continuously soiling himself would’ve been front page news.

Americans may very well get lower gas prices in the next two years, which will be the result of weakened demand coupled with excess supply (importantly, not due to Trump’s policies). However, investors won’t be seeing their shares of oil stocks appreciate alongside lower prices at the pump.

So rather than taking everything he says at face value, let’s scrutinize some more facts to see how it could impact you as an investor.

Oil Prices & Oil Stocks Are Struggling

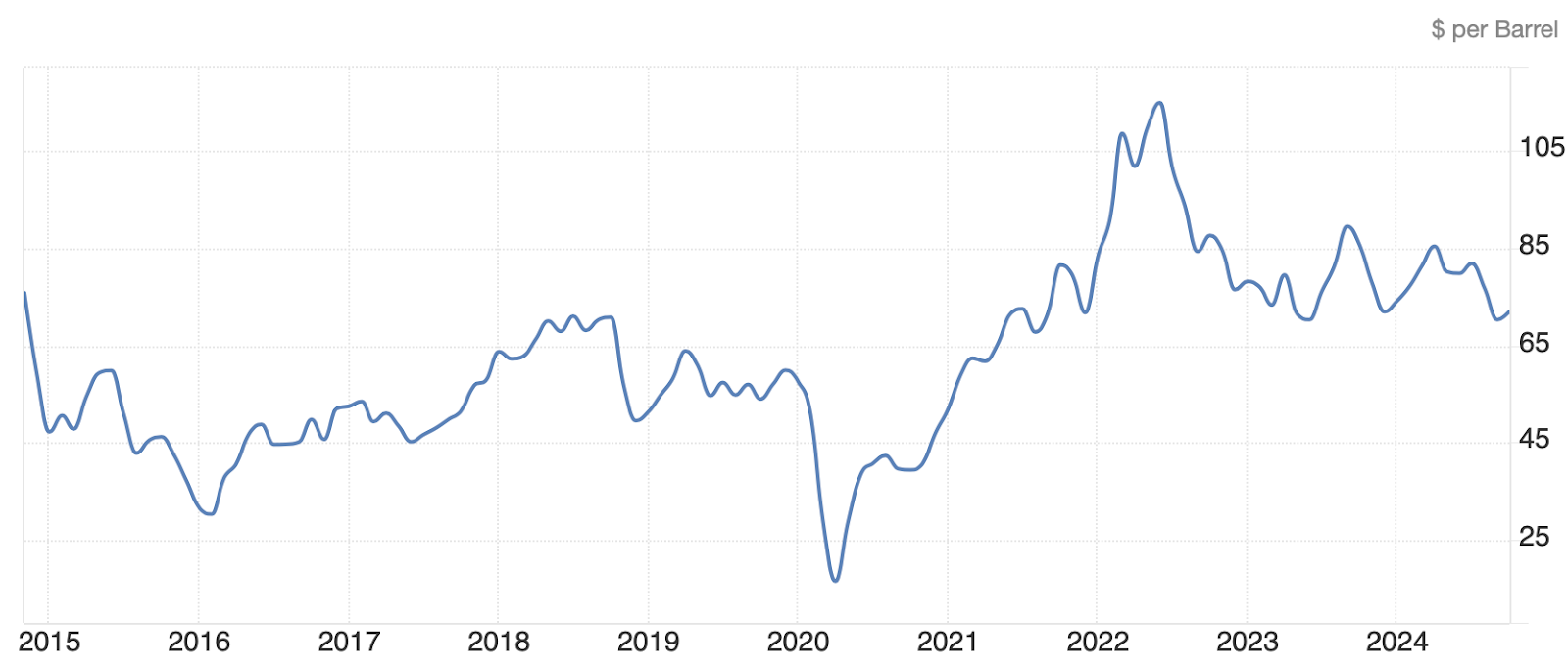

Year-to-date, West Texas Intermediate (WTI) — the American crude oil benchmark used to price production and exports — has fallen -4.94% in 2024.

WTI is currently priced at $71.99 per barrel, significantly down from its 10-year high of $114.84 per barrel in June 2022.

Meanwhile, ExxonMobil has seen its shares gain 10.30% this year. And while positive returns are nice, the Big Oil mainstay has vastly underperformed the S&P 500’s 28% gain in 2024.

Looking at the other five oil majors shows similarly subpar performances, with the following year-to-date gains/losses:

- Chevron: +5.08%

- Shell: -1.84%

- ConocoPhillips: -12.27%

- TotalEnergies: -14.74%

- BP: -15.24%

ExxonMobil has led the pack … by underperforming the broad market by 17.70% this year. And with a tempered — at best — outlook for 2025 and 2026, investors should consider rebalancing their portfolios.

Because no matter what Trump says, (1) wind turbine noise does not cause cancer and (2) energy is unlikely to be a top-performing sector in the first half of his next administration.