Here’s What Next Week’s Rate Cuts

TL;DR

The first of a potential series of long-awaited interest rate cuts by the Federal Reserve is just around the corner. The result could be an incredibly strong finish to the year for the major market indices.

March 2020 seems like forever ago. People were stockpiling toilet paper, disinfecting their groceries and acclimating to Zoom meetings.

It was also the last time the Federal Reserve, after an emergency meeting, slashed its effective federal funds rate (EFFR) — the benchmark interest rate that dictates everything from the APY you receive on a CD to the APR you pay on your credit card balance.

Then, from March 2022 to July 2023, the Fed enacted a series of rate hikes to the EFFR in a largely successful effort to combat decades-high inflation.

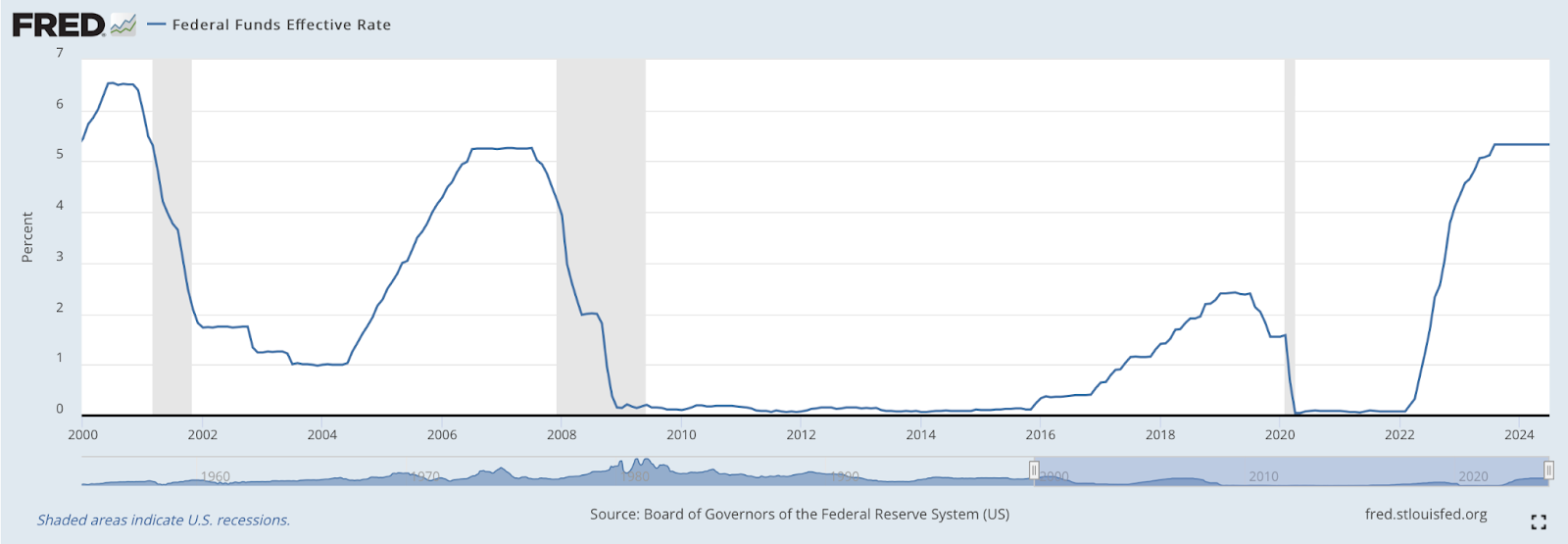

They haven’t touched the EFFR since, and according to the Federal Reserve Bank of St. Louis, rates are the highest they’ve been since 2001:

But next week, that’s all about to change.

What Rate Cuts Will Do for the Market

It’s largely expected that when the Fed announces the first rate cut at its FOMC meeting from Sept. 17-18, it will serve as an impetus for stocks.

But it’s not that analysts are simply bullish. Some are historically bullish. Take, for example, Wells Fargo’s head of global investment strategy Paul Christopher, who has stated that the looming rate cuts could bring about a watershed moment the likes of which the market hasn’t seen in nearly 30 years.

Christopher was referring to 1995, when Alan Greenspan’s Fed lowered the EFFR and the S&P 500 went on to gain an astounding 34.11% that year after setting a then-record 77 new all-time highs.

While the chances of repeating a gain like that this year aren’t great, the Fed’s decision could spark a rally that closes the year strong and sets the tone for 2025.

And this is regardless of who wins the election this November. In fact, despite common misconceptions, the stock market tends to perform rather well in election years and is already enjoying a roughly 18% gain through the first eight months of 2024.

According to T. Rowe Price, going back to 1927, the S&P 500 has seen a median annual return of 14% in election years compared to a marginally better 14.7% in non-election years.

Media fear-mongering aside, regardless of who next occupies the White House, the odds are that the market is going to continue its momentum … if not pick up steam.

Don’t Get Left Behind

If you find yourself sitting on a large cash position because you:

- Mistakenly thought election years were bad for the market

- Were frightened by the mid-summer sell-off that was mislabeled a “market crash”

- Or were simply playing it safe and shifted to more conservative allocations

… Then it’s time to act. By now, you’ve hopefully locked in a +5% rate on debt instruments like CDs or U.S. Treasurys. But we’re talking about focusing on the stock market.

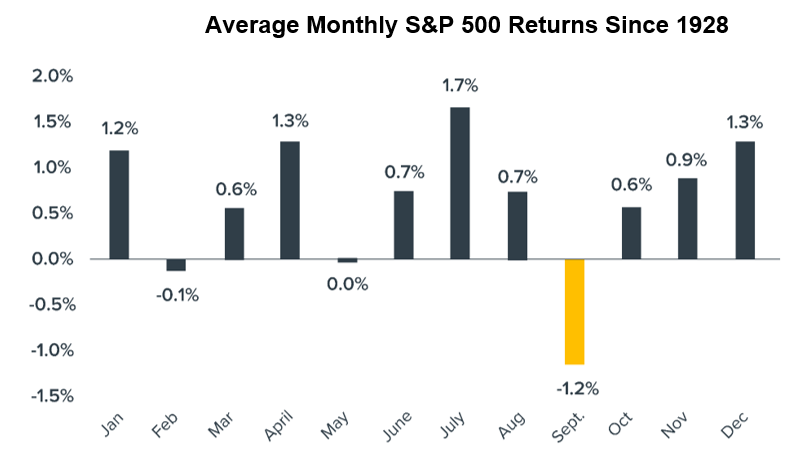

While elevated volatility in September has been well-documented, October and November are two of the Nasdaq’s four best-performing months of the year, and November, December and January are three of the S&P 500’s five best-performing months of the year:

In short, stocks might not be as cheap as they are in September for the remainder of the year and into next. Investors who hesitate to deploy their cash could wind up leaving potential gains on the table.

If you’re able to, don’t let this opportunity pass you by. They say the best time to invest was 30 years ago, but the second-best time to invest is right now.

Remember: If you received this email from a friend or family member, sign up here so you don’t miss any future issues.

Additional Reading …

When the Federal Reserve last cut interest rates significantly, markets responded with notable rallies. Returning to the 1995 example, following a series of rate cuts by the Fed that year, the S&P 500 surged by over 34% by the end of the year, setting a record for all-time highs.

Similarly, in 2008, rate cuts were used to combat the financial crisis, leading to a prolonged recovery in the stock market, though it was more gradual and tied to a fragile economy.

These moments highlight the power of rate cuts to rejuvenate markets, especially when they follow periods of tightening. While past performance isn’t a guarantee of future results, it’s worth considering how these cuts have consistently triggered market rebounds and created opportunities for investors willing to act early.

Rate Cut Cheat Sheet

Interest rate cuts create ripple effects across various investment types. Here’s a quick breakdown of what this means for you:

Stocks: Lower interest rates often encourage businesses to borrow more cheaply, invest in growth, and boost profits. This typically leads to stock market rallies, as seen in past cycles.

Bonds: While bond yields may drop with rate cuts, bonds issued before the cut often increase in value because their higher rates become more attractive compared to newer bonds.

Real Estate: Lower rates mean cheaper mortgages, which can drive demand in the housing market. Real estate investment trusts (REITs) often benefit as property values rise.

Cash: If you’ve been sitting on a large cash position, this might be the moment to reconsider. Holding too much cash while the market recovers could mean missing out on significant gains.

The takeaway? Rate cuts often favor equities and real estate, while fixed-income investments like bonds may require strategic timing. Balancing your portfolio with these trends in mind could be key to maximizing your returns.

With the Federal Reserve’s decision just days away, there are a few steps you can take to ensure you’re ready for what’s coming:

How to Prepare

Review Your Portfolio

Look at your current asset allocation and decide whether it’s time to shift toward more aggressive growth opportunities like stocks, especially if you’ve been holding defensive positions like bonds, Treasurys or other cash alternatives.

Lock in Fixed Income Rates

If you’ve been eyeing fixed-income investments like U.S. Treasurys or CDs, consider locking in rates now before they drop further post-rate cut.

Consider Dollar-Cost Averaging

If you’re worried about volatility, dollar-cost averaging into the market could be a safer way to ease into riskier investments over time rather than making a large lump-sum investment right away.

Dollar-cost averaging is the commitment to investing a fixed dollar amount on a recurring basis (daily, weekly, monthly, etc.). Doing so mutes short-term noise and the need to ever try to time the market.

The Fed’s rate cut offers a window of opportunity, but it’s key to act strategically. Preparing your investments before the announcement could mean better positioning for the upcoming market cycle.