Not Every Pick’s a Winner, But Most Are

It’s almost 2024, so what better time for a year-in-review than now?

With the calendar about to turn, we want to recap how our recommendations have performed since making them.

And while most performed well, not all have. Nonetheless, we stand by our contention that all of this is to help you make better personal finance decisions.

In that vein, it’d be neglectful of us to not revisit our issues over the past year. After all, the reason we founded Rise & Hedge was to demonstrate how you can educate yourself and find opportunities in a world increasingly lacking them.

We don’t want you to rely on us (or anyone else) for suggestions about where to look in the market, though. Our primary objective is to help you improve your money management.

That’s why:

- Last week, we explained how you can use roboadvisors to get better portfolio performance than you would with stockbrokers.

- Last month, we showed you how easy it is to use a stock screener to find your own picks.

- And earlier this year, we talked about debt management, retirement savings and conservative investments like CDs, Treasurys and high-yield savings accounts.

So you’ll notice we don’t have stock (or ETF) picks for you every week. It’s equally important to discuss savings, alternative investments and profitable side hustles.

But in case the jury’s still out about our picks, we want to reaffirm that, with a little bit of your own research built on the backs of our how-to issues, success is there for the taking.

The idea isn’t to hop on the bandwagon of flashy, headline-grabbing companies with the world’s most disagreeable CEOs.

Rather, we want you to understand in which sectors to look for companies that’ll provide you with consistent returns (and dividends) year after year.

Our 2024 Track Record

November

In mid-November, we discussed how American farmers produce a surplus that feeds the world. The Andersons (ANDE), our No. 1 pick that week, is up 6.67% since. It’s a small window, but the company’s been around since 1947 and we like that the dividend’s increased for 28 years. Its fundamentals underscore its success.

Our other two picks that issue — Archer-Daniels-Midland (ADM) and CHS Inc. (CHSCP) — are up 2.78% and 5.53%, respectively.

October

The Monday before Halloween, we talked trash. Literally. Per capita, America produces the third most waste in the world. Our picks, Waste Management (WM), Republic Services (RSG) and Clean Harbors (CLH), are up 6.76%, 10.51% and 13.11%, respectively, since that issue.

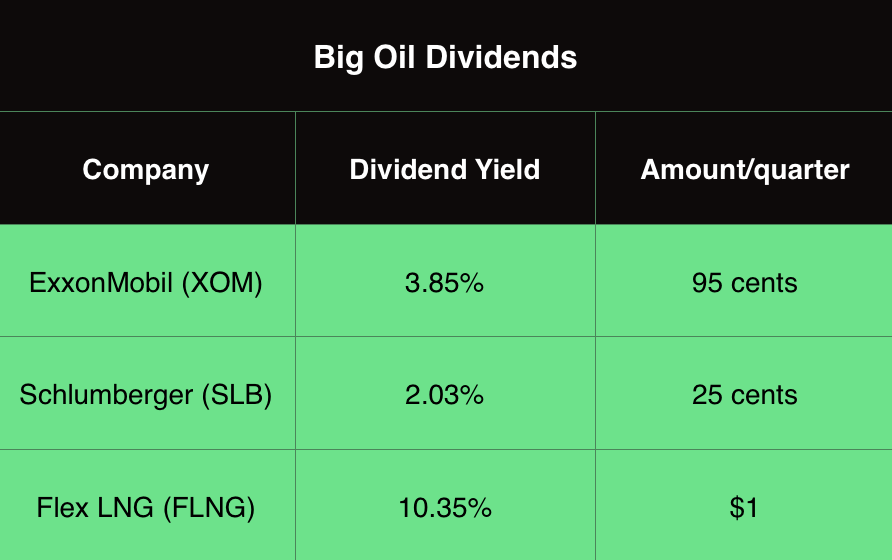

Big Oil’s seen some share depreciation since we wrote about it in October, but that’s a consequence of America hitting an all-time-high in domestic production. ExxonMobil (XOM) is down 9.16% since, Schlumberger (SLB) has shed 16% and Flex LNG (FLNG) dropped 6%.

Fossil fuel companies have pulled back across the board, and like we explained then, this is a natural correction after the energy sector outperformed all others last year. Our opinion remains unchanged … we like the prospects for 2024, and the dividends for those companies ice the cake:

In mid-October, we introduced you to some high-income ETFs. iShares iBoxx $ High Yield Corporate Bond ETF (HYG) is up 3.97% since while paying a 5.43% monthly dividend. JPMorgan Equity Premium Income ETF (JEPI) is up 1.45% since while paying an 8.61% monthly dividend. And Pacer U.S. Cash Cows 100 ETF (COWZ) is up 1.69% while paying 2.03% quarterly dividend.

Crypto scares the sh*t out of people. But we’ve routinely stressed the importance of portfolio diversification as a strategy to offset risk exposure … even if that means allocating a tiny bit to alternative assets. Since our Oct. 2 issue on National Cryptocurrency Month, Bitcoin (BTC) is up 52% and Ethereum (ETH) is up 33%.

September

In late September, we reported on companies that capitalize on holidays. Starbucks (SBUX) is up 6.62% since, Hershey (HSY) is down 9.55% and pumpkin spice-manufacturer McCormick (MKC) is down 10.18%.

In mid-September, we wrote about how 32 of 33 developed countries in the world have successfully implemented universal healthcare. The one that hasn’t won’t shock you … but how much some companies profit from our broken healthcare system might. Our pick that week, HCA Healthcare (HCA), is up 1.41% since, but up 16.91% since Oct. 26.

August

In late August, we reported on the writers’ strike and AI’s role. It was a you-call-it issue recommending Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), NVIDIA (NVDA) or C3.ai (AI) for exposure to AI.

Since that Aug. 28 issue:

- AI: -4.62%

- NVDA: -2.11%

- GOOGL: +0.91%

- APPL: +6.44%

- AMZN: +8.71%

Food prices remain out of control. And while corporations continue to blame inflation, rearview data proves its “greedflation,” and those companies have been shockingly lying to us all along.

Those corporations continue their profiteering campaigns, albeit with mixed results for their shares. Since Aug. 3, our food-leveraged picks PepsiCo (PEP), Kroger (KR), Ingles (IMKTA) and Invesco DB Agriculture Fund (DBA) are down 10.35%, down 9.43%, up 1.71% and up 0.28%, respectively.

However, those companies operate in the consumer staples sector, which has performed third-worst of the S&P 500’s 11 sectors this year. And since consumer staples are wants, not needs, these companies are likely to perform well over the long term as they’ve done for years. In the meantime, they all offer solid dividends that pay you to wait.

June & July

We’re firm believers in the saying, “Time in the market beats timing the market.” Without patience and a long-term plan, the odds are stacked against you.

Even though you’ve only been receiving our picks since Q3 of this year, the farther back we look, the more time those companies have had to demonstrate their value.

Since then, only one recommendation has a double-digit loss. Raytheon (RTX) has fallen -16.22% since June 12.

However, there are a trio of double-digit wins, including +12.61% on AbbVie (ABBV) since July 12, +15.10% on Boeing (BA) since June 12 and +19.09% on General Dynamics (GD) since June 12.

All of these are, of course, small sample sizes. But given the general direction of the market (up and right), time will continue to reward patient investors who’ve taken positions in these companies.

Transparency

We could’ve only highlighted the wins. There’s no shortage of financial publishers out there touting their successes in sales copy while hoping you forgot about the 73% loss you took on Tesla (TSLA) after they recommended it at its five-year top in November 2021.

But we don’t write sales copy. Frankly, it disgusts us.

We’re here to provide you with free insight — built on experience and tireless research — to help you find opportunities to grow your wealth. And even if some of those positions we’ve touched upon over the past six months are down, we remain confident that in the long term, they’ll produce.

So in this last issue of our inaugural year, we want to stress three points:

- We want you to LEARN.

- We want you to SUCCEED.

- And we want you to do so at NO COST.

Plenty more of that’s to come in the new year. We’ll be back in your inboxes on Monday, Jan. 8. Until then, happy Hanukkah, merry Christmas and happy New Year!