Insurance in Florida Is a Disaster of Its Own.

Last Wednesday, Hurricane Idalia crept up Florida’s Gulf Coast and made landfall as a Category 4 storm in the state’s Big Bend region.

The strongest storm to strike the area in 125 years, it battered homes and businesses for hundreds of miles of coastline.

But it wasn’t the 125 m.p.h. winds that caused the most damage. Just like Hurricane Ian the year prior, the bulk of the damage was the result of catastrophic storm surge. Up to 15’ in some areas.

It’s why FEMA’s been so busy reconfiguring flood zones across the state since Ian.

It’s why handfuls of property insurers have either gone insolvent or abandoned the state entirely.

And it’s why the state of insurance is akin to the Florida Man spotted paddling an inflatable duck through the floodwaters of Tampa in Idalia’s aftermath: a hot f*****g mess.

The Dumpster Fire State

Sure, Florida has its fair share of issues. Off the top of our heads:

- A rise in emboldened neo-Nazis who have yet to be condemned by state leadership.

- Orwellian-esque school book bans.

- And a recent law allowing permitless carry, which is fitting for a state known for the intelligence of its citizenry.

Disclaimer: Author James Baldwin once stated, “I love America more than any other country in the world and, exactly for this reason, I insist on the right to criticize her perpetually.” By extension, as Floridians, we reserve the right to sh*t on this state to illustrate our points herein.

Yes, you’d be hard-pressed to find a state without some kind of issue making it look like a dumpster fire.

However, it feels like Florida has no shortage of them. Like the state’s invasive species, or along similar lines, relocatees from New York.

But to many homeowners residing here, the aforementioned issues pale in comparison to …

The Atrocious State of Property & Flood Insurance

According to a significant number of headlines this year, the Florida home insurance market is collapsing.

Whether that’s due to unscrupulous business practices, moral vacancy among executive leadership or simply because they’re packing up and cutting their losses … it’s happening.

Don’t take our word for it, though. The evidence is overwhelming:

- Since 2021, Florida homeowners holding policies with six property insurers were left abandoned after those companies became insolvent.

- Since 2017, 11 property and casualty (P&C) insurers in Florida have been liquidated.

- In July, Farmers Insurance pulled out of the state, leaving +100,000 homeowners scrambling for a policy.

- The average annual home insurance premium in Florida is now $2,385/year, up more than $900 since 2022 and four times the national average.

- Florida now accounts for 79% of all homeowners insurance lawsuits.

- And only ~15% of Floridians have flood insurance, either due to ineligibility or prohibitively expensive policies resulting from the state’s low-lying topography and rapidly rising sea levels.

With more people moving to the Sunshine State every day, but fewer insurers willing to issue policies to Florida’s denizens, the situation is progressively dire.

We don’t want to point the finger of blame … but climate change has a lot to do with it.

Florida’s Not Alone

Climate change isn’t Santa Claus, the Tooth Fairy or a Cleveland Browns Super Bowl title. It actually exists.

And like we discussed two weeks ago — similar to the market — climate change doesn’t care about your opinion.

It’s pervasive, global and increasingly severe. After decades of ignoring the scientific community, we’re now seeing the results in real time:

- In a three-day stretch during July, Italian firefighters simultaneously battled 1,400 wildfires.

- From July 3–6, the global temperature record was broken four days consecutively.

- And due to 100° water temperatures in July, there’ve been numerous coral reef mass mortality events around the world.

According to the National Oceanic and Atmospheric Administration, last year, the cost of climate and weather disasters in the U.S. totaled more than $165 billion … the third most costly year on record.

So it’s evident that fewer insurers are going to be covering a growing global population in a rapidly warming world.

Insuring Your Portfolio

Investing in a slimy industry seems … well, slimy. But with how the industry’s consolidated, there are fewer options.

Whether it’s flood or P&C insurance, the biggest corporate insurers are raking it in.

This week, we’re not going to delve into year-to-date gains, financial fundamentals or price targets. Because — like oil majors — it’s hard to go wrong with any of the large-cap insurance companies.

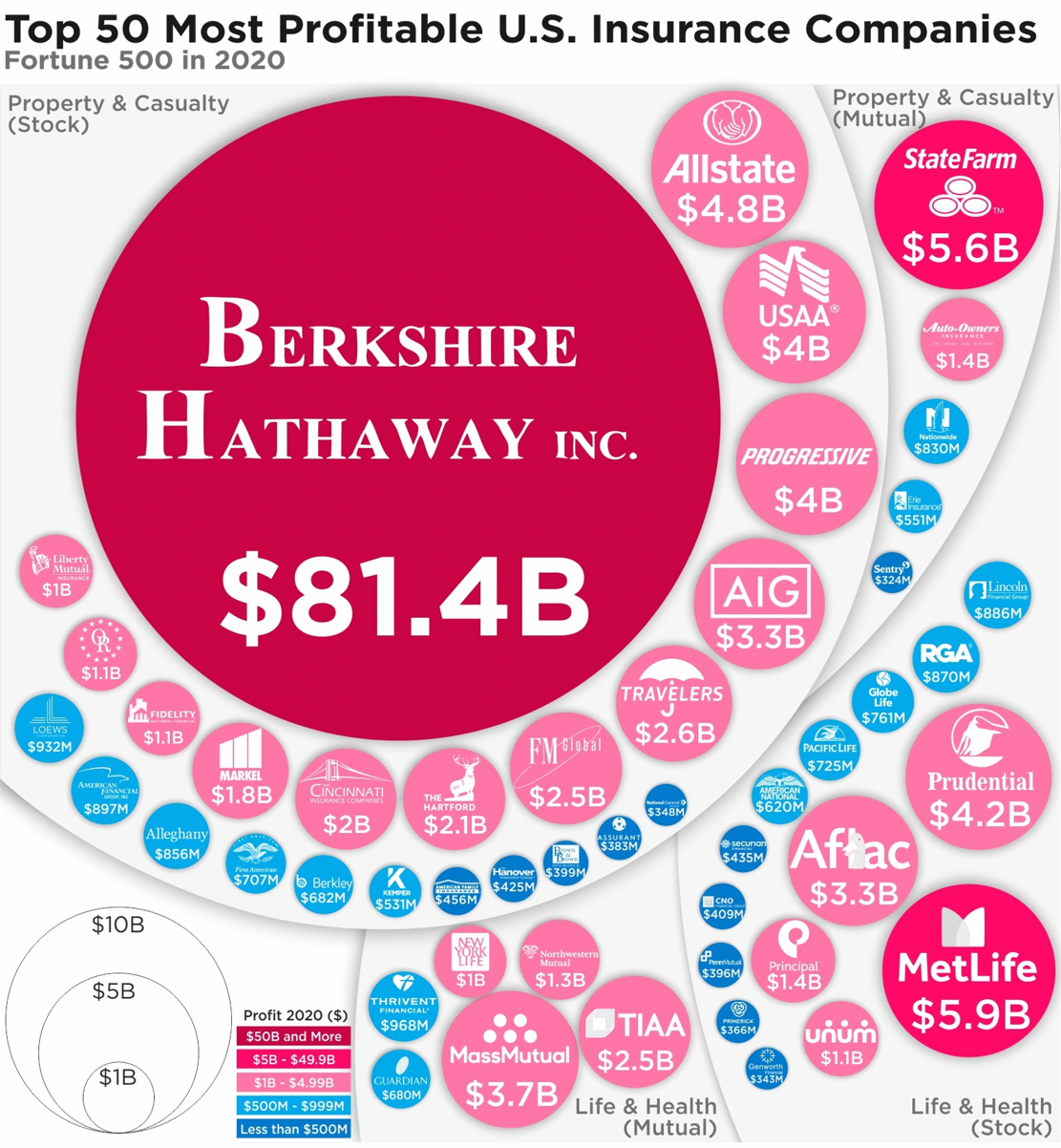

Instead, here’s a fun infographic:

The scary part — besides Earth literally scorching itself — is that the above image is based on 2020 data.

Since then, and not including 2023, there’ve been three hurricanes that’ve made U.S. landfall, two of which were “major” hurricanes.

And 127,973 wildfires. Just in America.

TL;DR

Insurers are vacating Florida as quickly as new residents are arriving, while climate change is increasing the frequency and severity of natural disasters. There are 24 Fortune 500 companies operating in the insurance space that have made profits in excess of $1 billion. For buy-and-hold investors, purchasing shares of the publicly traded ones is a way to capitalize on the calamity.