Tax-Free College Savings That Benefit From Compound Interest

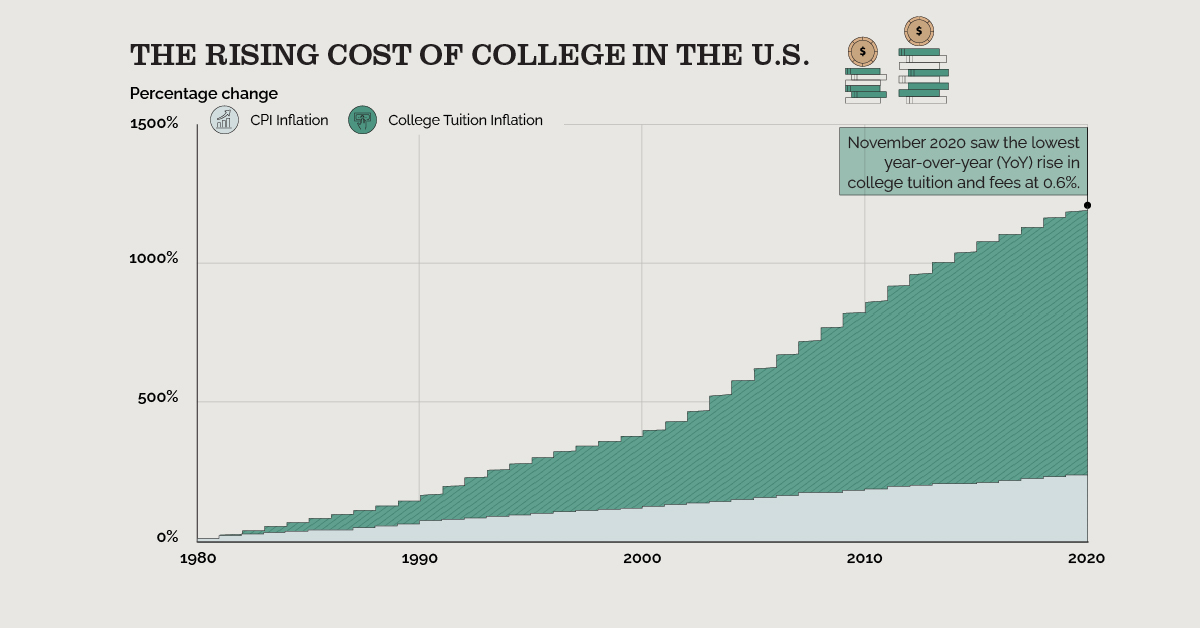

Since 1980, the cost of college has increased 1,200%.

| Compound Interest /ˈkämˌpound in·truhstˈ/ noun the interest on savings calculated on both the initial principal and the accumulated interest from previous periods |

Albert Einstein was pretty smart. Perhaps not compared to today’s greatest scientific minds, though.

After all, prodigy Rick Perry, the former governor of Texas, was appointed the 14th Secretary of Energy. And in college, Perry received a grade of “D” in a science course titled “Meats.” He also failed organic chemistry.

Perfectly qualified for the job if you ask us. (We’re sure his predecessor, 13th Secretary of Energy Ernest Moniz — a nuclear physicist — would agree.)

So while Einstein’s accomplishments pale in comparison to those of the Texas wunderkind, the theoretical physicist made his fair share of contributions during his 76 years on Earth.

Beyond his seminal work in quantum mechanics and general relativity, he had some insightful observations about personal finance. Specifically, Einstein described compound interest as the eighth wonder of the world.

We’ve discussed it before. Compound interest is the secret sauce behind successful retirement accounts, high-yield savings accounts and dividend-paying stocks.

But it’s also the key to ensuring you save enough money for your child’s college education.

The Big Three

If you’re saving for your child’s college education, kudos to you. There’s no right or wrong way of doing it, and the fact that you’re trying to provide your child with a better future speaks bounds about you as a parent.

Especially since you don’t want your kid burdened by out-of-control college expenses. The days of being able to work a part-time, minimum-wage job to pay for a full-time course load are long gone.

So now matter how you’re saving, at least you are.

But in our opinion, the flexibility, tax benefits, lack of contribution limits and ability to use funds for an array of educational expenses make the 529 college savings plan the best option.

Here’s a survey of three most common plans.

No. 1: 529 prepaid plans

- Only offered in 11 states.

- Locks in lower tuition costs.

- Funds are restricted to use for tuition and administrative fees. Some states, like Florida, include provisions for room and board.

- Plans are based on in-state tuition at the state’s public colleges, so if your child wants to go to a private institution or an out-of-state college, you’ll have to pay the difference between the actual costs and the prepaid tuition plan’s amount.

- Funds are in the account custodian’s name, so there are negligible impacts on the student’s eligibility for financial aid.

- Depending on the state, the beneficiary might not be able to be changed.

No. 2: Uniform Gifts to Minors Act (UGMA) or Uniform Transfer to Minors Act (UTMA)

- Used to provide financial gifts to a child.

- Can be used by the recipient for any purpose once the child is old enough to take ownership.

- Contributing more than $15,000 to $30,000 per year (depending on tax filing status) can trigger federal gift tax.

- Earnings after the first $1,100 are taxed as income.

- Funds are in the child’s name, which can significantly impact their eligibility for financial aid.

- Beneficiary cannot be changed.

No. 3: 529 college savings plan

- No annual contribution limits (but maximum lifetime contribution limits).

- Can produce returns that exceed the cost of tuition.

- No tax on interest earned when used for qualified education expenses.

- Qualified education expenses go beyond just tuition, room and board or administrative fees, and include on- and off-campus housing, computers, books, internet access, school supplies and special needs equipment.

- Funds are in the account custodian’s name, so there are negligible impacts on the student’s eligibility for financial aid.

- Beneficiary can be changed to a family member.

- Funds can also be used for K-12 expenses ($10k annually) and student loan repayments ($10k lifetime).

- 18 states offer FDIC-insured plans.

- Up to $35k of unused funds can be rolled over into a Roth 401(k) or Roth IRA.

There are pros and cons to each. And as parents, you’re already aware of the need to choose what’s right for you and your family.

However, if you decide on a 529 savings plan, it’s important to understand …

Some Are Significantly Better Than Others

When it comes to 529 savings plans — just like U.S. Secretaries of Energy — not all are made the same.

Those who’ve had the privilege of leading the Department of Energy include Harvard alumni; Nobel Prize laurates; science faculty at MIT, Stanford and UC Berkeley; and the chair of the Atomic Energy Commission.

And then there’s Rick Perry. If you can help it, avoid getting your child the Rick Perry of 529 savings plans.

For example, due to high fees and perpetually poor fund performance, plans like the Rhode Island CollegeBound Fund, Georgia Path2College and Nevada UPromise College Fund are ranked among the worst.

Conversely, the CollegeAdvantage Ohio 529 Plan is routinely ranked in the top five due to its strong year-to-year performance and relatively low fees.

TL;DR

There are several options you can use to save for your child’s college expenses. Some benefit from compound interest. Our pick is a 529 college savings plan because of its flexibility, tax benefits and lack of annual contribution limits. If your child proves to be brighter than Rick Perry (fingers crossed) and receives a scholarship, you can roll a large portion of a 529 savings plan into a Roth 401(k) or Roth IRA for your child to give them a head start on retirement savings.