Spring Cleaning Your Personal Finances

TL;DR

April’s Financial Literacy Month. These four moves — starting a college savings account, taking advantage of high yields while they’re still around and getting a piece of the stock market’s record highs — can help secure a better future for you and your family.

It’s already April and Q2 is underway. It’s also National Pet Month, Scottish-American Heritage Month and Keep America Beautiful Month.

And while we’d love to see you walking your dog while eating haggis and collecting roadside litter, offering practical recommendations during Financial Literacy Month is more our speed.

So without further ado, here are four moves you can make this month that by next April, you’ll be patting yourself on the back for.

1. Set Up a 529 College Savings Plan

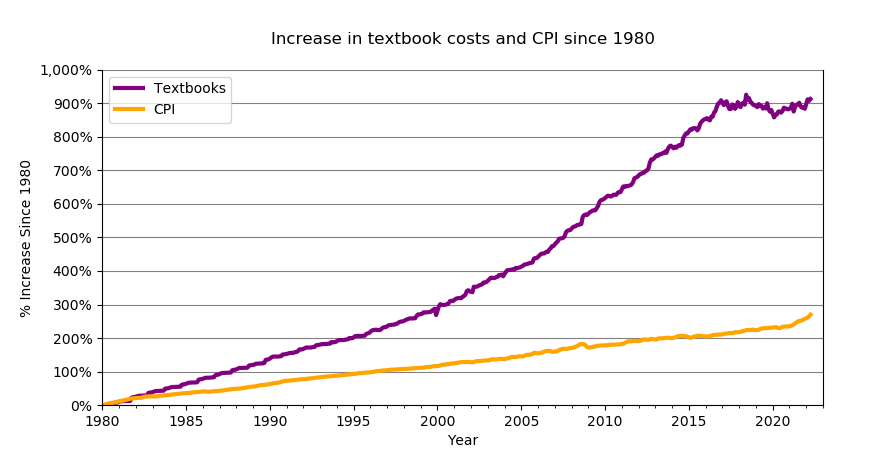

If you’re a parent, this is a no-brainer. Even if you earmark as little as $25/month, over time, a 529 plan college savings plan will help your child combat runaway tuition and textbook prices.

The racket that is college textbook publishing has been well-documented, with prices increasing 1,041% since 1977, while college tuition has increased 153% over the past 40 years.

As parents, you don’t want to burden your child with debilitating student loan repayments as soon as they enter the workforce. A 529 plan can help. (If you or your child is already struggling with repayment, read our primer on student loan debt forgiveness.)

Silver lining: If they decide to not attend college, that money can be rolled over into a Roth IRA in their name, which will help get them started on their retirement savings path.

2. Act on High APYs While They’re Still Here

The Federal Reserve spent the past two years hiking interest rates to offset 40-year high inflation. That ended last July, and to the surprise of many, it worked without being coupled with a crushing blow to the job market:

- Unemployment remains near 54-year lows.

- The Inflation Reduction Act has resulted in construction jobs nearly doubling what they were pre-pandemic in 2019.

- And inflation’s fallen considerably to its current 3.8%.

Some “news” outlets won’t report this to their indoctrinated audiences, but if you’d like to see the facts for yourself, the most recent Consumer Price Index readings are here.

Getting down to the Fed’s goal of 2% inflation is proving tricky, though. This is delaying the central bank’s decision to begin cutting interest rates, which means you still have some time to take advantage of the highest APYs in decades.

High-yield savings accounts (HYSAs) — with variable rates — probably aren’t the answer anymore. Marcus by Goldman Sachs lowered the APY of its HYSA from 4.5% to 4.4% two weeks ago, and others could begin following suit.

If you’re comfortable with your money not being immediately accessible, we recommend CDs, some of which still offer +5% rates for terms as short as 12 months with minimum deposits as low as $500.

Once rates are cut, economists expect massive outflows from savings and debt instruments that will be injected into the stock market, which received its highest forecast of the year last week.

3. Start Researching Equities

If Wall Street’s prognosticators are correct, we haven’t seen the last of the stock market setting all-time highs this year. So far in 2024, that’s been accomplished numerous times by the S&P 500, the Dow Jones and the Nasdaq.

(Again, you’re unlikely to hear this from certain “news” outlets. But facts are pesky in that they exist whether you like them or not. See here, here and here.)

If you’re a passive investor, start looking into index funds that mirror underlying benchmarks. Make sure they carry low expense ratios (they should as they’re passively managed) and be on the lookout for ETFs that fly under the radar.

For example, the SPDR Portfolio S&P 500 ETF (SPLG) as opposed to the longer-established SPDR S&P 500 ETF Trust (SPY). While they boast nearly identical holdings, SPLG has an expense ratio that’s 77% lower and has marginally outperformed the SPY.

If you want to get a piece of tech gains, the same goes for the Invesco Nasdaq 100 ETF (QQQM), which has nearly identical holdings as the more recognizable Invesco QQQ Trust (QQQ) but with an expense ratio that’s 25% lower.

If you’re more active in your portfolio management, look at stocks in sectors with inelastic demand. Companies that’ve created an impenetrable competitive moat. And learn how to identify and avoid stocks that are portfolio poison.

Just because you can get on a Spirit flight for under $100 doesn’t mean their stock — down nearly 95% from its all-time high — belongs in your holdings.

4. Share This Newsletter

We don’t know anyone who couldn’t use a little help shoring up their financial wellbeing. If there are people in your life that could benefit from reading Rise & Hedge, forward this email and ask them to sign up.

They’ll be grateful because knowledge is wasted when it’s not shared.