Smart Investments Before the Fed Cuts Interest Rates

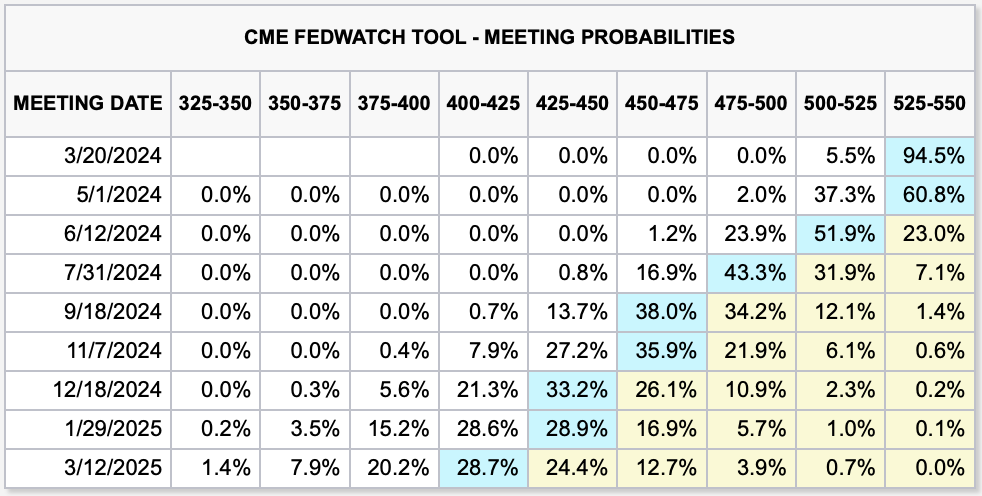

If you’ve never heard of CME FedWatch Tool, you’re not alone. It’s an obscure apparatus of the CME Group, which operates the Chicago Mercantile Exchange, New York Mercantile Exchange, the Commodity Exchange and owns 27% of the S&P Dow Jones Indices.

None of that’s important, aside to say that the company has its finger on the pulse. Its FedWatch Tool is an extension of that, gauging the market’s expectation of potential changes to the effective federal funds rate (EFFR) — the Federal Reserve’s benchmark interest rate.

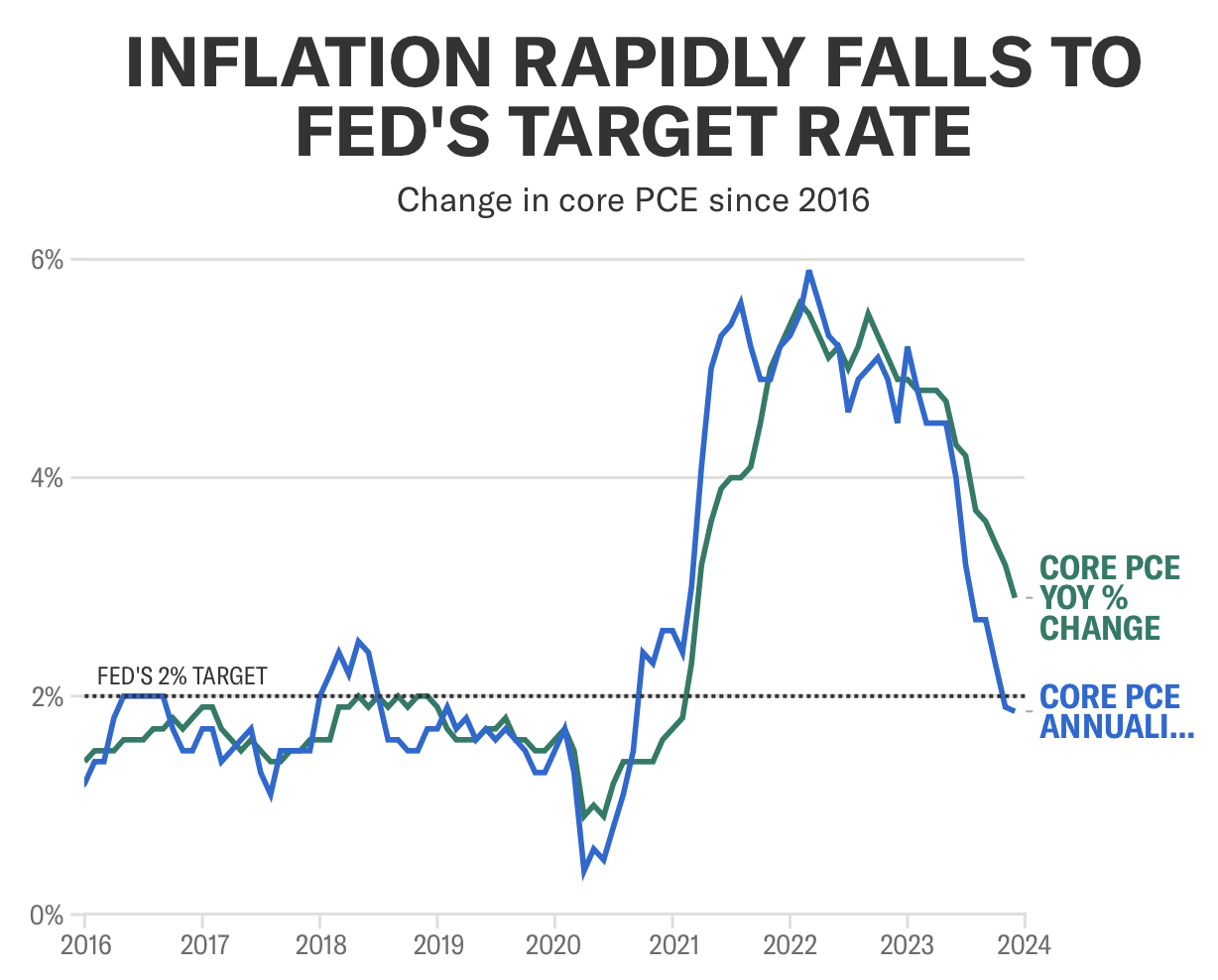

Despite last week’s Consumer Price Index (CPI) report showing inflation a bit hotter than expected for January … it remains likely the Fed will begin to cut interest rates at some point later this year.

Why? January’s CPI reading might’ve come in 0.1% higher than economists’ expectations, but the fact remains inflation has cooled significantly over the past two years.

So long as we don’t get any outlier CPI readings in the next couple of months, the Fed’s expected to begin cutting rates.

Enter the CME FedWatch Tool, which shows a 39.3% probability of that occurring in May, and a 77% chance of it happening in June, with the current EFFR at 5.3% (or 533 basis points):

What Rate Cuts Mean

When the Fed begins slashing rates, it’ll have a trickle-down effect. Not like the one the Reagan administration promised in the ‘80s that never materialized.

Spoiler alert: The London School of Economics conducted a 50-year study across 18 advanced economies that found “no evidence that tax cuts for the wealthy will generate economic growth.”

Conversely, rate cuts will have sweeping impacts that trickle down to manifold industries and — for our purposes — investments. For starters:

- Debt instruments (e.g., CDs and Treasury bills) will stop offering such appealing rates.

- Ditto for saving instruments, like money market accounts and high-yield savings accounts.

- Real estate could see a long-awaited spark. Since the start of the pandemic, skyrocketing rates resulted in mortgage refinancing falling from 80% of all loan origination to 20%.

- As bond rates fall, their inverse relationship with dividend yields sees the latter begin to grow stronger.

- Interest rate-sensitive industries that benefit from borrowing could see enormous growth opportunities with their stocks experiencing outsized performances.

While we won’t be focusing on all of those in this issue, we’ll discuss the three — (1) dividend stocks in interest rate-sensitive industries, (2) savings instruments and (3) debt instruments — that you can act on now to position yourself for looming rate cuts in 2024.

Benefit From Borrowers

Two weeks ago, we talked about real estate investment trusts (REITs) and how they’re likely bounce-back candidates this year given the interest rate environment.

The same holds true for other high-yield equities that rely heavily on interest rates, like business development companies (BDCs).

Like REITs, BDCs were significantly impacted by the Fed’s rate-hiking cycle. That’s because they’re organizations that invest in small- and medium-sized companies, helping them grow through startup stages through debt acquisition or direct investment.

And also like REITs, BDCs must distribute at least 90% of their taxable income to shareholders. That’s why REITs and BDCs tend to pay big dividends.

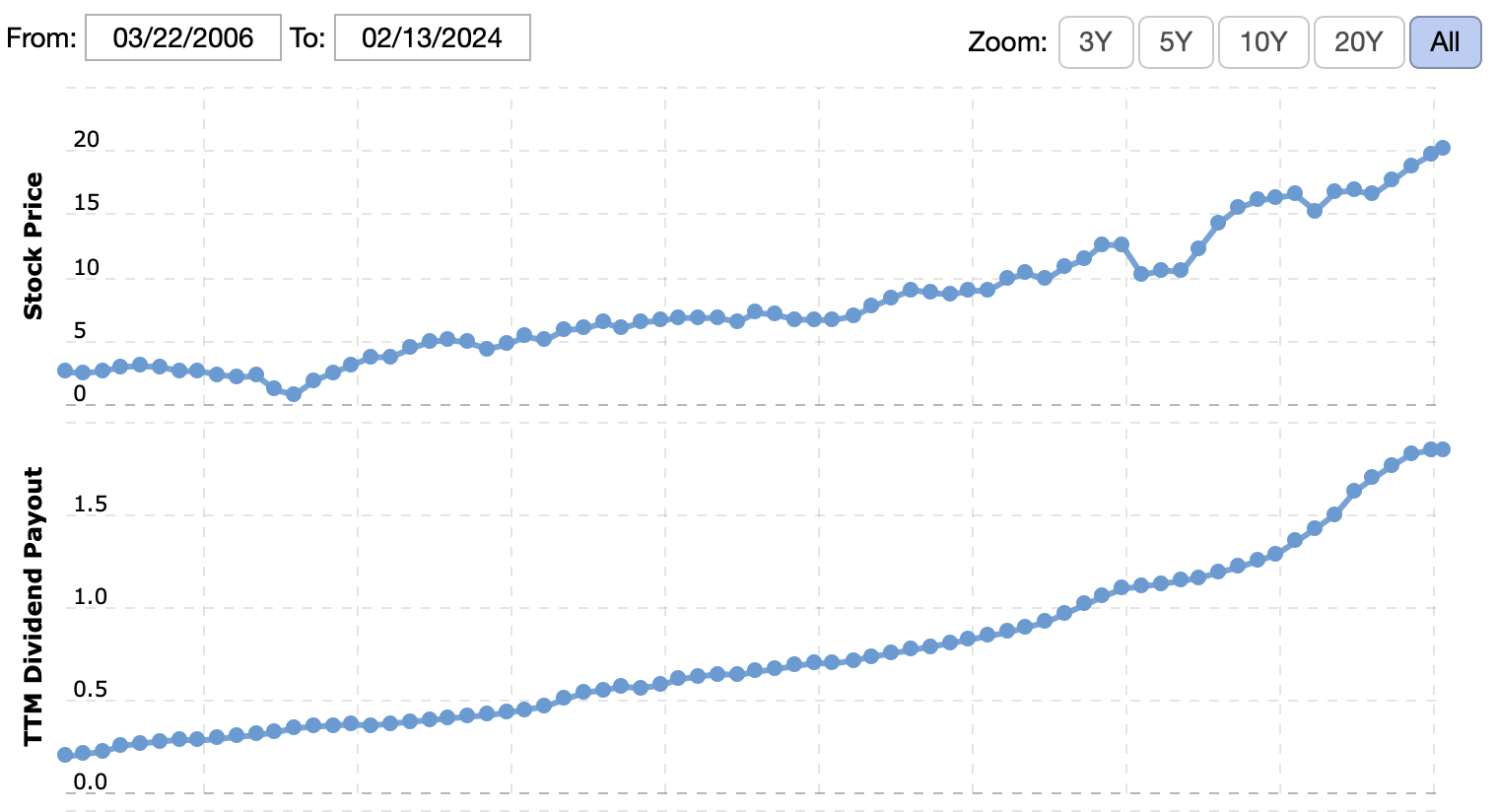

We talked about a REIT we like earlier in February. For BDCs, we’re drawn to the distributions paid by Ares Capital (ARCC), the largest publicly traded BDC by market cap, and SLR Investment (SLRC), which yield 9.51% and 10.94%, respectively.

These aren’t yield traps, either, as you can see with ARCC’s historical share appreciation and payout growth:

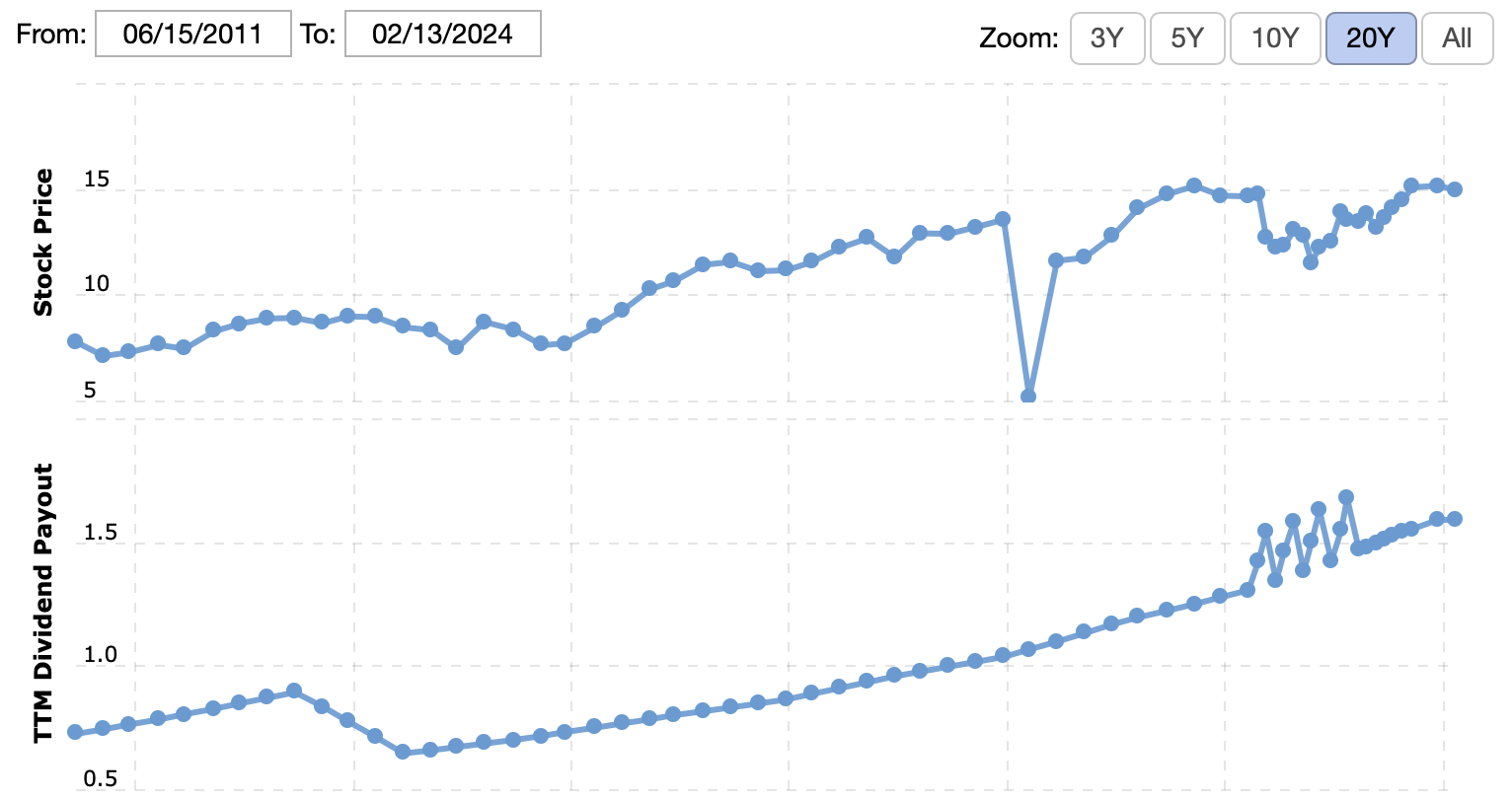

The same goes for SLRC:

As a bonus, both ARCC and SLRC are currently trading below $20/share.

Shore Up Your Savings

High-yield savings accounts (HYSAs) and money market accounts (MMAs) offer APYs that are ~11x better than those offered by traditional savings accounts.

Importantly, these rates are variable. The banks and credit unions offering these accounts can adjust the rates without notice whenever the financial institution feels it’s appropriate.

Are the APYs on HYSAs and MMAs likely to fall later this year? Yes. Is it still worth it to get as many months of ~5% APY exposure as possible before rates do fall? Again, yes.

HYSAs and MMAs compound interest daily and pay it monthly, meaning that as long as those rates remain high, you’re getting better APY with daily compounding and monthly payouts. Meanwhile, the bank on the corner provides 0.47% APY.

No amount of free lollipops for kids makes that acceptable. Don’t let your savings rot away in a brick-and-mortar bank just because it’s conveniently located.

Lock in CD & Treasury Rates

Whereas HYSAs and MMAs offer variable rates, debt instruments like CDs and bonds pay fixed interest rates, and it makes sense to lock in higher rates while you still can.

The U.S. Department of the Treasury’s I bonds are paying 5.27% for at least six months after you purchase them.

After last week’s CPI news, the interest rate for the 10-year Treasury note jumped to 4.27%, its highest since December 2023. It’s similar for CDs. With a minimum deposit of $500, Space Coast Credit Union — which is insured by the NCUA, the credit union equivalent of FDIC-insurance, which protects account balances up to $250k per depositor — is currently offering 12-month CDs paying 5.61% APY.