The Perfect Example of an Overvalued Market

TL;DR

The market remains under fire, with volatility up 86% since Trump took office. The major indices are either firmly in correction territory or rapidly approaching it. But buy-and-hold investors are in better positions than those trying to time the market.

Meanwhile, one stock’s performance serves as an example of an overvalued market that’s firmly entrenched in a late bull cycle.

The market remains a mess. We gave you a few clues why last week, among them a collapse in consumer confidence (fueled by tariffs, lingering inflation and the realization that Trump’s tax plan is going to cost everyday Americans more money), a collapse in investor sentiment and a surge in unemployment claims.

Additionally, the Atlanta Fed is now calling for a nearly 3% contraction in Q1 GDP (in early January, the forecast was expansion of 3%), credit card delinquencies are at a 13-year high, car payment delinquencies are at a 30–year high and Americans can’t sell their homes as rates remain elevated (which the Fed attributes to Trump-induced volatility) and new homes inventory reaches its highest level since 2008’s financial crisis.

The major indices continued to sell-off. As we write this:

- The Dow is down 900 points and has lost -6.83% since its six-month high.

- The S&P 500 appears to be on the same track to correction, down -8.74% since its year-to-date high on Feb. 19.

- The Nasdaq has officially entered correction territory, having lost -13.59% since its six-month high.

Meanwhile, Bitcoin has lost -26.22% since hitting its all-time high on Dec. 17, dragging down with it the entire crypto market.

Stock volatility, as measured by the VIX, is higher than it’s been at any time since Oct. 21, 2022, at the tail end of the last bear market. So once again, we’re holding off on our next stock pick — though we’re increasingly confident a good buying opportunity is approaching. Instead, today we have a hodgepodge issue that we hope will keep your finger on the pulse.

A Glimmer of Hope

We’re not saying a recession or bear market are around the corner. But as investors, we suggest you prepare accordingly. We’re already seeing a rotation out of cyclicals and growth-oriented sectors into more conservative boring-is-better defensive positions.

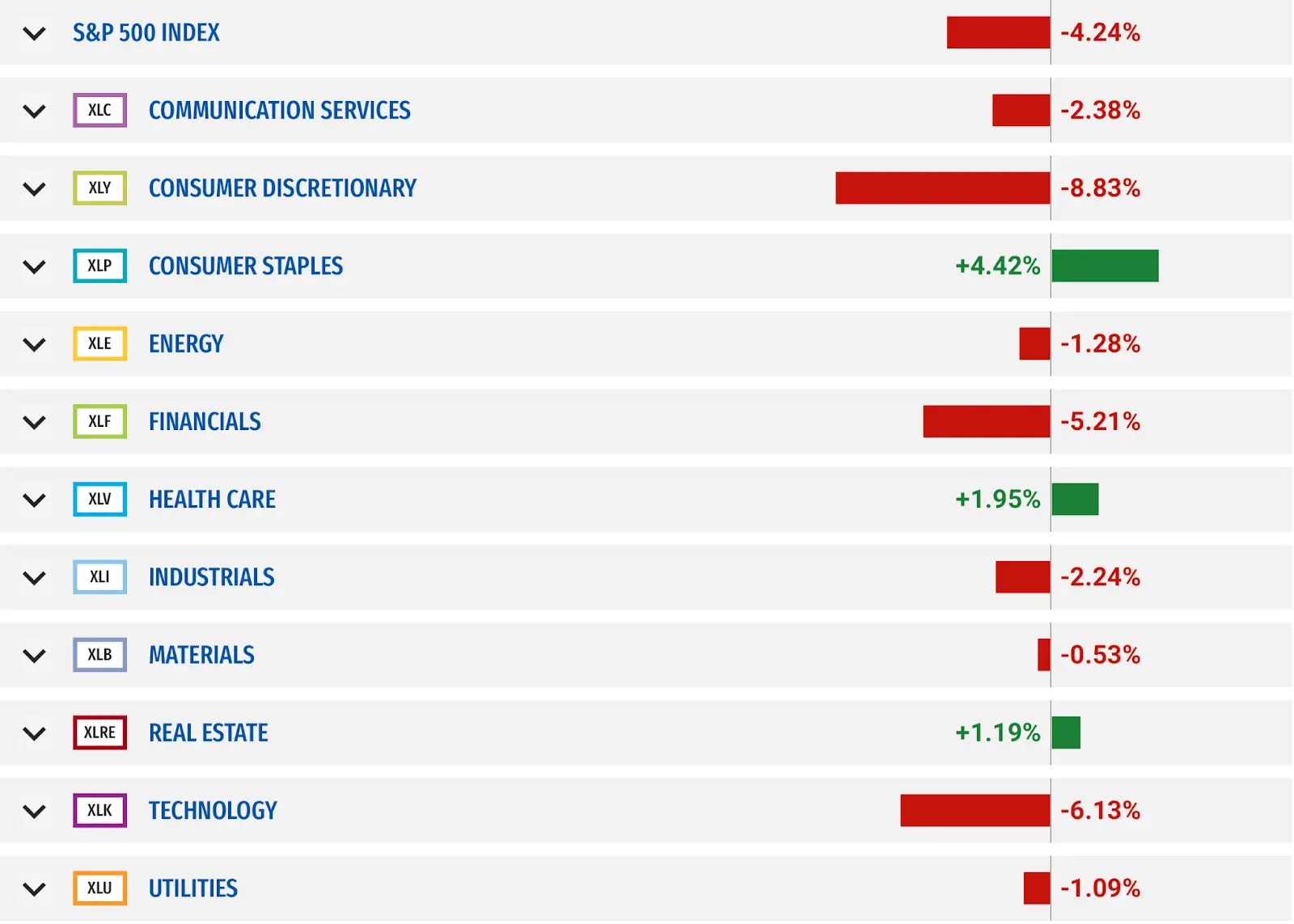

When the slow-and-steady consumer staples sector is handedly outperforming the S&P 500’s other 10 sectors, it’s not indicative of a healthy bull market:

But if we are on the verge of a broad correction or a full-blown bear market, there’s a silver lining. First, almost everything will be discounted. Before you decide to lock in gains (or worse, sell for a loss), consider this Buffettism: “The stock market is the only place where investors run out of the store during a sale.”

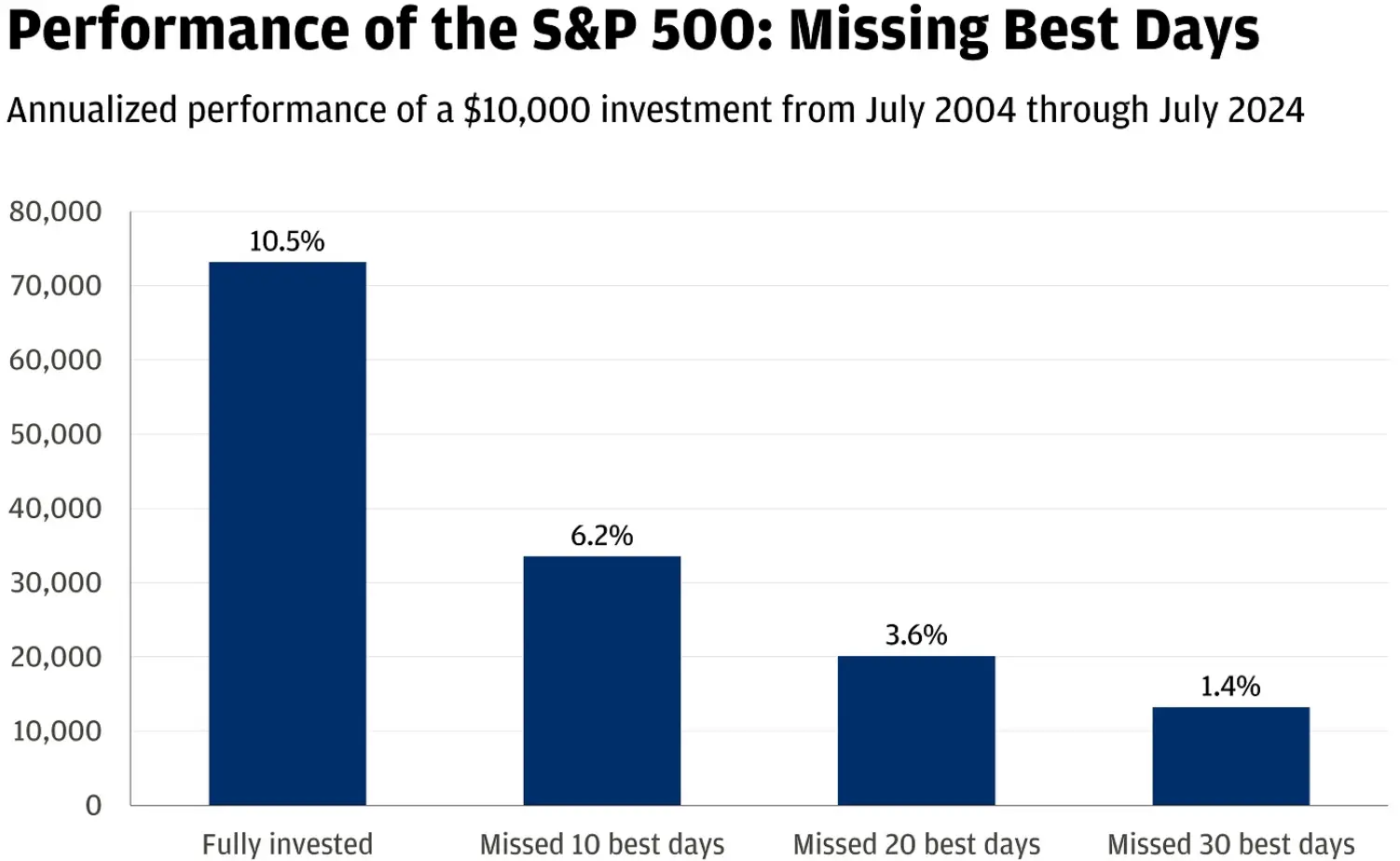

Data from JPMorgan shows that over a 10-year period, missing just the 30 best days of market performance between 2014 and 2024 would result in your average annualized return being reduced from 10.5% to 1.4%. Just 30 days of you sidelining cash because of a correction or bear market would decrease your returns by 86.66%. For the everyday investor, it’s clear that remaining invested is the best option.

Second, understanding the length of market cycles is critical. According to Hartford Funds, since 1928, the average bull market has lasted 2.7 years (the current bull market began in earnest in October 2022). Meanwhile, the average bear market has lasted less than one year.

It gets better. The average bull market has returned 115% whereas the average bear market has lost 35%. And lastly — and perhaps most germane — the first half of a bull market has outperformed the second half in 20 out of 27 bull markets since 1928.

Why’s that important? Because market timing is a fool’s errand. Those who are sitting on cash risk missing out on the outperformance of a bull market’s first half once the tides turn. To quote the report, “Since a new bull is only identifiable once it’s under way, you could miss many of the market’s strongest days if you wait for the right time to invest.”

So while zooming in currently resembles a California wildfire, zooming out reminds us that history suggests the best approach is patience and fortitude. But it’s also helpful to be able to identify a sinking ship.

Musk Enters the FAFO Stage

The market is indicating it needs to correct, and if that correction is deep enough, it could be the end of the current bull run. One stock in particular serves as a microcosm of an overinflated market undergoing extreme pressure from macro conditions and poor policy decisions.

Add in a dash of neo-Nazism, and Elon Musk’s Tesla is proof of everything that’s wrong with the current market. (Also, to preclude any far-right apologist bullsh*t, we’re referring to this.) It turns out that a lot of prospective car buyers — especially in Europe — still hate Nazis. Tesla’s sales on that continent cratered -45% in January alone. According to DriveSpark, to address this, Tesla is getting desperate and offering 0% interest loans and free lifetime parking.

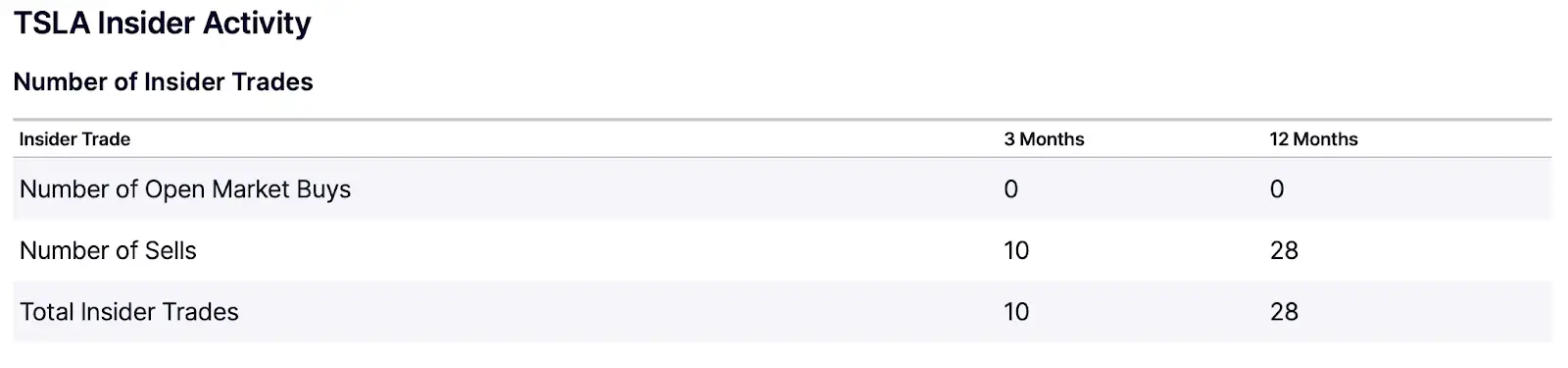

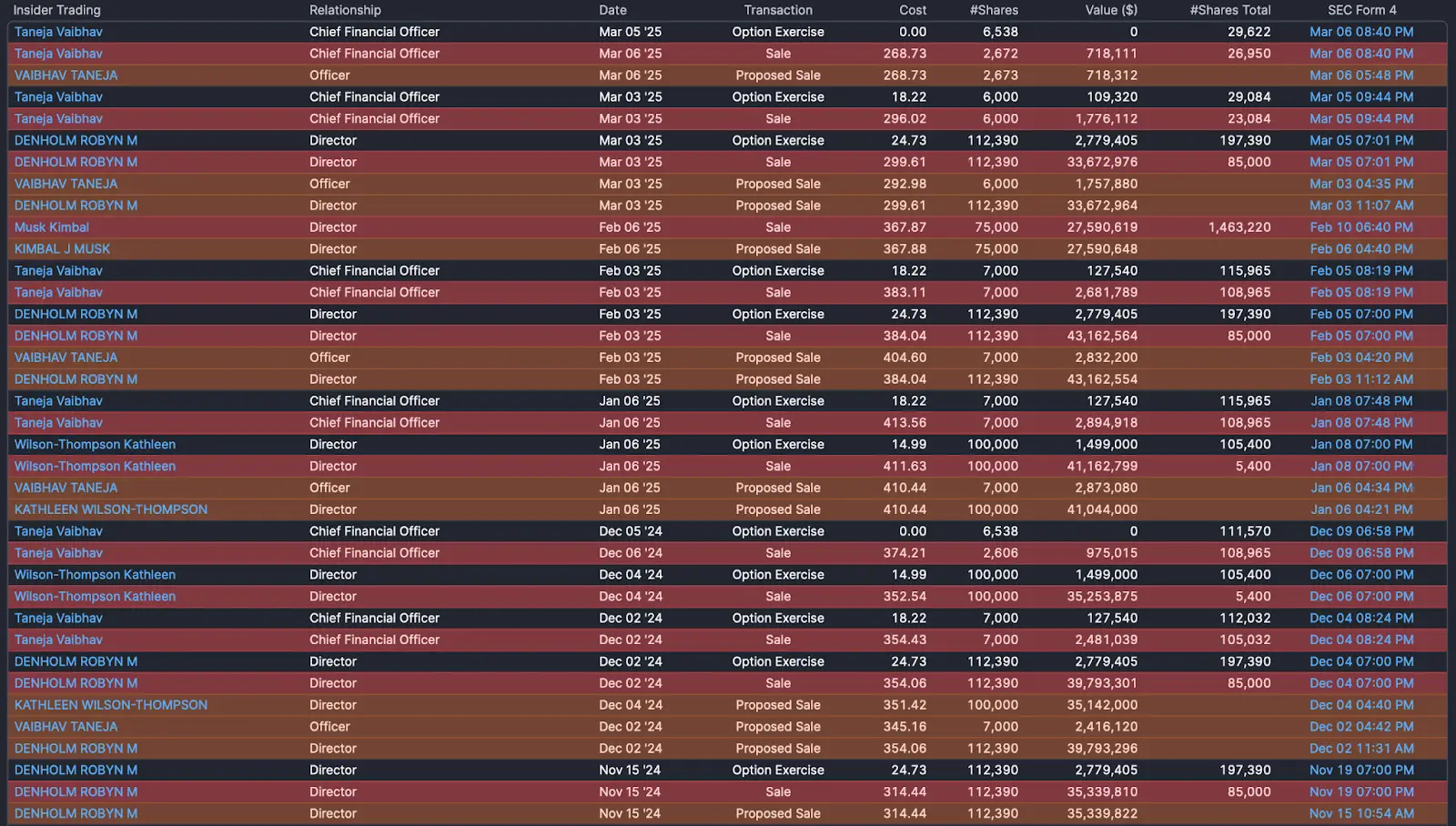

It also turns out that even before he removed any doubt about being a literal fascist, insiders were already vacating their positions because of how obscenely overvalued Tesla’s stock was. In the past year, not one single share of Tesla was purchased by insiders (i.e., Tesla executives, directors or anyone who owns more than 10% of the company’s stock).

It’s not just that insiders haven’t been buying Tesla stock — they’ve been dumping it hand over fist, including Musk, his brother, the company’s CFO and various directors:

When we say Tesla is overvalued, it’s not a matter of opinion. The company’s price-to-earnings (P/E) ratio is inordinately and unjustifiably high at 161.23. A P/E ratio tells us what investors pay for each dollar of earnings the company produces. Simply put, for every $1 Tesla earns, shareholders are dishing out $161.23.

For context, the S&P 500’s P/E ratio is currently 27.31. And even that is considered elevated given the index’s median P/E ratio of 17.7 since 1971. What’s the result? A deeply satisfying sell-off that’s seen the EV-maker’s stock plummet by nearly 54% since hitting its six-month high on Dec. 17:

If you’ve been a Rise & Hedge reader for a while, you’ll recall we warned you about this at the start of the year. But we also warned you numerous times before the sell-off began, including last summer. The good news? Musk has seen his net worth fall by $103 billion year-to-date (yet somehow remains the world’s wealthiest person, which is absurd).

In short, we find his actions — including his alignment with Germany’s far-right AfD party, his Sieg Heil from behind a lectern adorned with the presidential seal and his DOGE-driven gutting of services that have a direct and adverse impact on America’s veterans — to be reprehensible. Musk is a repugnant, indelible stain on humanity.

But from an objective standpoint, Tesla’s stock is currently a steaming pile of dung. Of 36 analysts that have rated it over the past month, 11 rate it a “Hold,” 12 rate it a “Sell” and the other 13 giving it a “Buy” rating must eternally hopeful that a bottom is in after the value of the stock halved since before Musk showed the world he’s a literal fascist.

If you’re a holder, you’re probably willing to ride out the storm. But if you do, be aware of the factors causing the company’s overvaluation, a potentially diminishing market and Musk’s atrocious public sentiment.

And, as always, follow the money. If insiders aren’t buying shares and institutional ownership is waning, wait until the opposite is evidenced before expanding your position. And if you’re looking for a buy-low opportunity in tech, consider this ETF which gives you weighted exposure to the Magnificent Seven before buying any one particular stock.